Fillable Promissory Note Document for Wisconsin

Fillable Promissory Note Document for Wisconsin

In the state of Wisconsin, individuals who intend to loan money or receive loans have a legal tool at their disposal to ensure the terms of their agreement are clearly defined and enforceable: the Promissory Note form. This document serves as a binding agreement between a borrower and a lender, detailing the loan amount, interest rate, repayment schedule, and the responsibilities of all parties involved. Its use is common in both personal and business finance contexts, providing a level of security and predictability to financial transactions. The importance of this form cannot be overstated, as it not only outlines the financial obligations but also sets forth the consequences should the borrower fail to meet the terms agreed upon. With provisions for both secured and unsecured loans, the Wisconsin Promissory Note form accommodates a wide range of lending scenarios, making it a versatile tool for managing loans within the state. It’s crucial for parties entering into such agreements to familiarize themselves with the specifics of the Promissory Note to ensure it accurately reflects their intentions and complies with Wisconsin law, ultimately safeguarding the interests of both lender and borrower.

Wisconsin Promissory Note Template

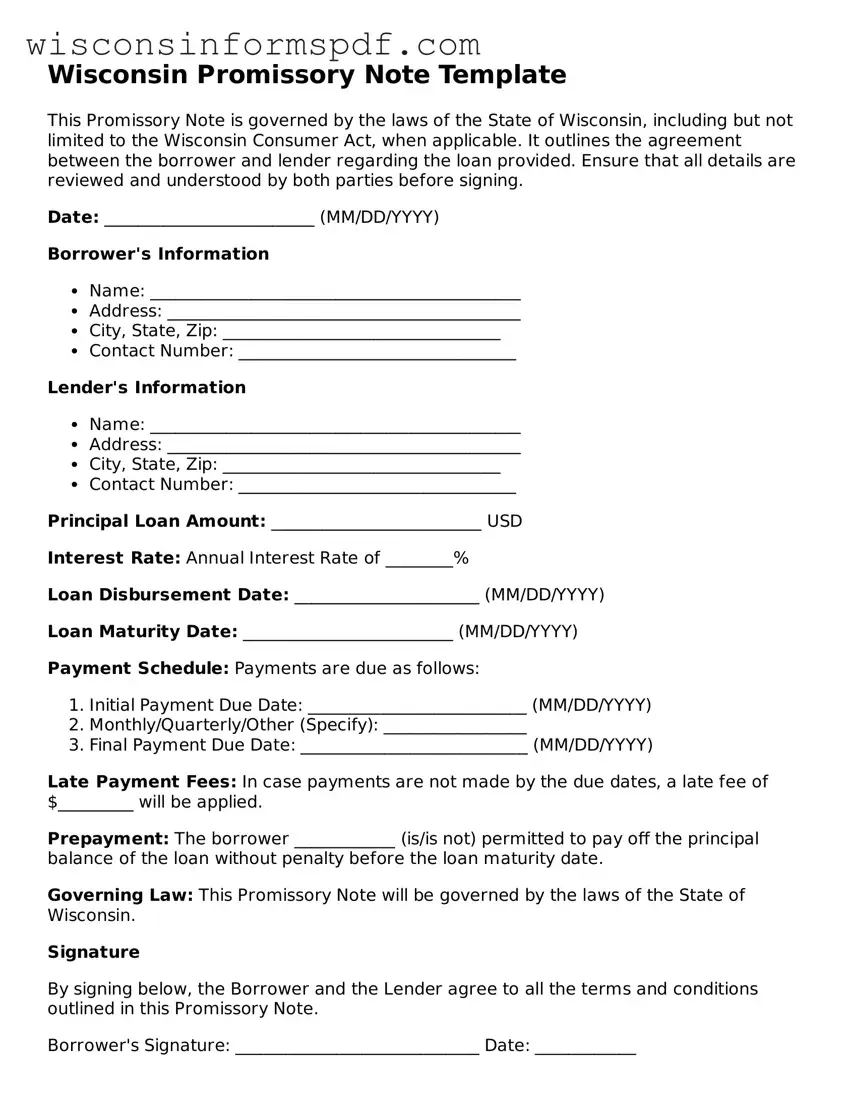

This Promissory Note is governed by the laws of the State of Wisconsin, including but not limited to the Wisconsin Consumer Act, when applicable. It outlines the agreement between the borrower and lender regarding the loan provided. Ensure that all details are reviewed and understood by both parties before signing.

Date: _________________________ (MM/DD/YYYY)

Borrower's Information

Lender's Information

Principal Loan Amount: _________________________ USD

Interest Rate: Annual Interest Rate of ________%

Loan Disbursement Date: ______________________ (MM/DD/YYYY)

Loan Maturity Date: _________________________ (MM/DD/YYYY)

Payment Schedule: Payments are due as follows:

Late Payment Fees: In case payments are not made by the due dates, a late fee of $_________ will be applied.

Prepayment: The borrower ____________ (is/is not) permitted to pay off the principal balance of the loan without penalty before the loan maturity date.

Governing Law: This Promissory Note will be governed by the laws of the State of Wisconsin.

Signature

By signing below, the Borrower and the Lender agree to all the terms and conditions outlined in this Promissory Note.

Borrower's Signature: _____________________________ Date: ____________

Lender's Signature: _______________________________ Date: ____________

| Fact Name | Description |

|---|---|

| Governing Law | The Wisconsin Promissory Note form is governed by the laws of the State of Wisconsin, including but not limited to the Wisconsin Statutes Chapter 403, which pertains to negotiable instruments. |

| Types Available | There are two primary types of promissory notes in Wisconsin: secured and unsecured. A secured promissory note is backed by collateral, whereas an unsecured promissory note is not. |

| Usury Rate | In Wisconsin, the maximum interest rate that can be charged on a personal loan unless otherwise legally agreed upon is 5% per annum as per the Wisconsin Statutes Section 138.04. |

| Prepayment Penalties | Under Wisconsin law, prepayment penalties on promissory notes are allowed, but the conditions must be clearly stated within the note itself and agreed upon by both parties. |

| Late Fees | Wisconsin laws permit the inclusion of late fees for delayed payments on a promissory note. However, the amount and conditions related to these fees must be reasonable and clearly specified in the note. |

Filling out the Wisconsin Promissory Note form is essential for documenting a loan agreement between two parties. This document specifies the terms under which the loan is given and repaid, including the repayment schedule, interest rate, and what happens if the loan is not repaid as agreed. Creating a promissory note is a straightforward process but requires attention to detail to ensure all the information is accurate and legally binding.

After completing these steps, keep a copy of the promissory note for your records. This document is now a legally binding agreement that outlines the terms of the loan. Both the lender and the borrower should adhere to its terms to avoid any legal complications.

What is a Wisconsin Promissory Note?

A Wisconsin Promissory Note is a legal document that outlines a loan agreement between two parties in Wisconsin. It records the amount borrowed, the interest rate, repayment schedule, and other terms of the agreement, making the borrower legally obliged to repay the specified sum under those conditions.

Is a Wisconsin Promissory Note legally binding?

Yes, a Wisconsin Promissory Note is legally binding when it is properly filled out and signed by both the lender and the borrower. It can serve as evidence in court if there is a dispute over the repayment of the loan.

Do I need a witness or notary for a Promissory Note in Wisconsin?

In Wisconsin, having a witness or notarizing a Promissory Note is not usually required for it to be considered valid. However, involving a notary can add a layer of verification and could protect both parties in case of disagreements.

What information should be included in a Wisconsin Promissory Note?

The form should specify the amount of money lent, the interest rate, payment schedule, parties' information (lender and borrower), and any collateral if the note is secured. It may also include what happens if the borrower fails to make payments on time.

Can the interest rate on a Wisconsin Promissory Note be any amount?

No, the interest rate must comply with Wisconsin's usury laws, which cap the maximum interest rate to prevent unfair lending practices. Before setting the interest rate, it's important to check the current limits under state law.

What is the difference between a secured and an unsecured Promissory Note?

A secured Promissory Note requires the borrower to pledge an asset as collateral for the loan, offering the lender protection if the borrower fails to repay. An unsecured note does not involve collateral, posing a higher risk to the lender.

How can a lender enforce a Wisconsin Promissory Note if the borrower fails to pay?

If a borrower fails to make payments as agreed, the lender has the right to file a lawsuit to collect the debt. In the case of a secured note, the lender may also obtain the collateral. It's encouraged to seek legal advice to navigate the collection process properly.

Can the terms of a Wisconsin Promissory Note be modified after it's signed?

Yes, the terms can be modified, but any changes should be made in writing, and both the lender and the borrower must agree to the modifications. The amended agreement should then be signed by both parties.

What happens if I lose my original Wisconsin Promissory Note?

If the original note is lost, parties should create a signed statement detailing the note’s loss and the agreement's terms. This can serve as a substitute for the original note. It's also a good idea to include the steps taken to search for the lost document and any details of its presumed loss.

When it comes to filling out the Wisconsin Promissory Note form, there are a few common missteps that people tend to make. Although the form is designed to facilitate the process of promising to pay a debt, overlooking some key details can lead to significant issues down the road. By understanding these errors, individuals can ensure a smoother, more accurate process.

The first mistake is not specifying the interest rate. In Wisconsin, if an interest rate is not clearly stated, the note might be subjected to the state's default rate, which could be less favorable for the lender. Then, there’s the error of not clearly defining the payment schedule. Without specifying the dates and amounts, confusion and disagreements can arise regarding the payment expectations.

In addition to these common mistakes, it's also vital not to rush the process of completing the Wisconsin Promissory Note form. Taking the time to review and double-check all the information can prevent these errors. Moreover, it might be beneficial to seek advice or have the document reviewed by a professional if there's any uncertainty. After all, this document is a binding legal agreement, and its accuracy is paramount for both parties' protection.

In summary, the Wisconsin Promissory Note form is a powerful tool for documenting a loan agreement. However, to fully harness its benefits and protect all parties involved, it's crucial to avoid these common pitfalls. By paying close attention to detail and possibly seeking professional guidance, borrowers and lenders can navigate this process more successfully.

When dealing with a Wisconsin Promissory Note, which is a commitment by one party to pay another, it's important to understand that there are other forms and documents often used alongside it. These documents are crucial for various reasons, including legal protection, clarity, and ensuring that all parties fully understand the terms of the financial transaction. Here's a look at four such documents that are commonly used.

Understanding these documents can be vital for both the borrower and the lender. They ensure that all aspects of the loan are well-documented and clear to all parties involved. This can prevent misunderstandings and provide legal protections if disputes arise. When embarking on a loan, always consider which of these supporting documents might be necessary for your particular situation.

The Wisconsin Promissory Note form is closely related to a Loan Agreement. Both documents outline the terms under which money is lent and the repayment expected. The primary difference lies in the detail and formality; loan agreements usually provide more comprehensive details about the obligations of each party and often include security clauses that promissory notes may lack.

A Mortgage Agreement is another document similar to the Wisconsin Promissory Note, as both involve the lending of money with an agreement to repay. However, a Mortgage Agreement specifically involves real estate as collateral to secure the loan, ensuring the lender can claim the property if the borrower fails to meet the repayment terms.

An IOU (I Owe You) document bears resemblance to a promissory note, as it also represents a commitment to repay a debt. However, an IOU is typically less formal and may not include specific details about repayment terms or interest rates, making promissory notes a more legally binding and detailed option.

The Installment Agreement shares similarities with the promissory note by detailing a schedule for repaying a debt in parts over a set period. Both documents include information on the total amount owed and repayment terms, but the installment agreement focuses more on the timeframe and structure of the payments.

The Deed of Trust is in the same category as a promissory note in that it is used in financing arrangements, particularly involving real estate. Unlike a promissory note, which primarily documents the loan and its repayment, a Deed of Trust transfers legal title of real property to a trustee as collateral for the loan until the borrower pays off the debt.

A Line of Credit Agreement is similar to a promissary note because it involves a financial arrangement where a borrower is allowed to use funds up to a designated limit and is obligated to repay. The key distinction is that a line of credit agreement offers ongoing access to funds, unlike a fixed loan amount detailed in a promissory note.

The Credit Agreement has parallels with a promissory note, as both are used to document a loan. Credit agreements, however, are typically more complex, covering broader terms of credit between a lender and a borrower, including covenants, representations, warranties, and conditions precedent to borrowing.

A Student Loan Agreement can be compared to a promissory note, particularly since both involve borrowing money that must be repaid with interest. A student loan agreement, though, often includes specific conditions related to the borrower's education and may offer different terms for repayment, such as deferment options while the borrower is still enrolled in school.

An Equipment Loan Agreement shares similarities with a promissary note by detailing the borrowing of funds to purchase specific equipment. While the promissory note focuses on the promise to repay the amount borrowed, an equipment loan agreement typically includes additional terms regarding the use, maintenance, and insurance of the equipment.

Lastly, a Business Loan Agreement is akin to a promissory note in that both are used by businesses to borrow funds. However, business loan agreements often encompass a wider array of terms and conditions about the business operation, collateral, and detailed repayment schedules, reflecting the more complex nature of business financing.

Do ensure accuracy when entering the names of both the borrower and the lender to avoid any confusion or legal complications.

Don't skip including the loan amount in words and numbers to ensure clarity on the exact amount being agreed upon.

Do specify the interest rate clearly. Remember that Wisconsin has usury laws limiting the maximum interest that can be charged, so make sure the rate complies with these regulations.

Don't forget to outline the repayment schedule in detail, including the frequency of payments (monthly, quarterly, etc.), the amount of each payment, and when the first payment is due.

Do include any applicable late fees or penalties for missed payments to ensure the borrower is aware of the consequences of failing to make timely payments.

Don't leave out the consequences of default. It's crucial to explain what will happen if the borrower fails to comply with the terms of the promissory note, including any recourse available to the lender.

Do have a clear section detailing any collateral securing the loan, if applicable. This should include a description of the collateral and any conditions related to its seizure in the event of default.

Don't neglect to include the governing law clause. Specify that the promissory note is subject to the laws of the State of Wisconsin, which will govern any disputes that may arise.

Do ensure that both the borrower and the lender sign and date the promissory note. These signatures legally bind both parties to the terms of the note, so it's essential they are included.

When discussing the Wisconsin Promissory Note form, various misconceptions can lead to confusion among individuals. Here’s a list aimed at clarifying some of the common misunderstandings:

Legality is tied solely to professional preparation. Many believe that for a promissory note to be legal in Wisconsin, it must be prepared by a lawyer. While having a lawyer can ensure that all state-specific requirements are met, individuals can legally prepare their own forms, provided they include all necessary legal elements and comply with Wisconsin law.

All promissory notes are the same. There is a misconception that one generic form applies universally across all scenarios. In reality, promissory notes can vary significantly based on their purpose, such as personal loans, business loans, or real estate transactions. It's crucial that the form used is tailored to fit the specific situation and meet the requirements of Wisconsin law.

Interest rates can be freely chosen. Some people mistakenly believe that the interest rate on a loan can be set at any level by the parties involved. Wisconsin law, however, stipulates maximum interest rates to prevent usury. Before setting an interest rate, it’s important to consult state regulations to ensure compliance.

Oral agreements are as enforceable as written ones. Although oral agreements can be legally binding, proving the terms or existence of such agreements can be exceedingly difficult. In Wisconsin, a written promissory note serves as a tangible record of the loan’s terms, which is crucial for enforcement and protection under the law.

A signature is all that’s needed for validity. While the borrower's signature is critical, several other elements must be present for a promissory note to be considered valid and enforceable in Wisconsin. These elements include the loan amount, interest rate, repayment schedule, and any collateral involved. Missing any key details can compromise the effectiveness of the document.

Clearing up these misconceptions is vital for anyone engaging in lending or borrowing through a promissory note in Wisconsin. It ensures that both parties understand their rights and obligations, minimizing potential legal issues in the future.

When considering the creation and use of a Wisconsin Promissory Note form, it's important to understand the key elements and implications involved in its preparation and execution. This document, which is a written promise to pay a specified sum of money to a person or entity, must be handled with care to ensure legal enforceability and clarity regarding the terms of repayment. Here are nine crucial takeaways for individuals navigating this legal instrument:

Creating and using a Wisconsin Promissory Note requires a comprehensive understanding of these key takeaways to ensure the agreement is clear, fair, and legally compliant. Proper attention to detail can safeguard the interests of both the lender and the borrower, facilitating a smooth financial transaction.

Free Printable Bill of Sale for Car Wisconsin - For businesses, it can be an essential part of inventory sales records, tracking the sale of goods from the business to buyers.

Wisconsin Residential Lease Agreement Pdf - Offers peace of mind by specifying the condition the property must be in at the start and end of the tenancy, protecting both parties' interests.

Sample Power of Attorney for Vehicle Transactions - A necessary document for those wanting to ensure their vehicle's affairs are in good hands.