Fill Your Wisconsin 2 Form

Fill Your Wisconsin 2 Form

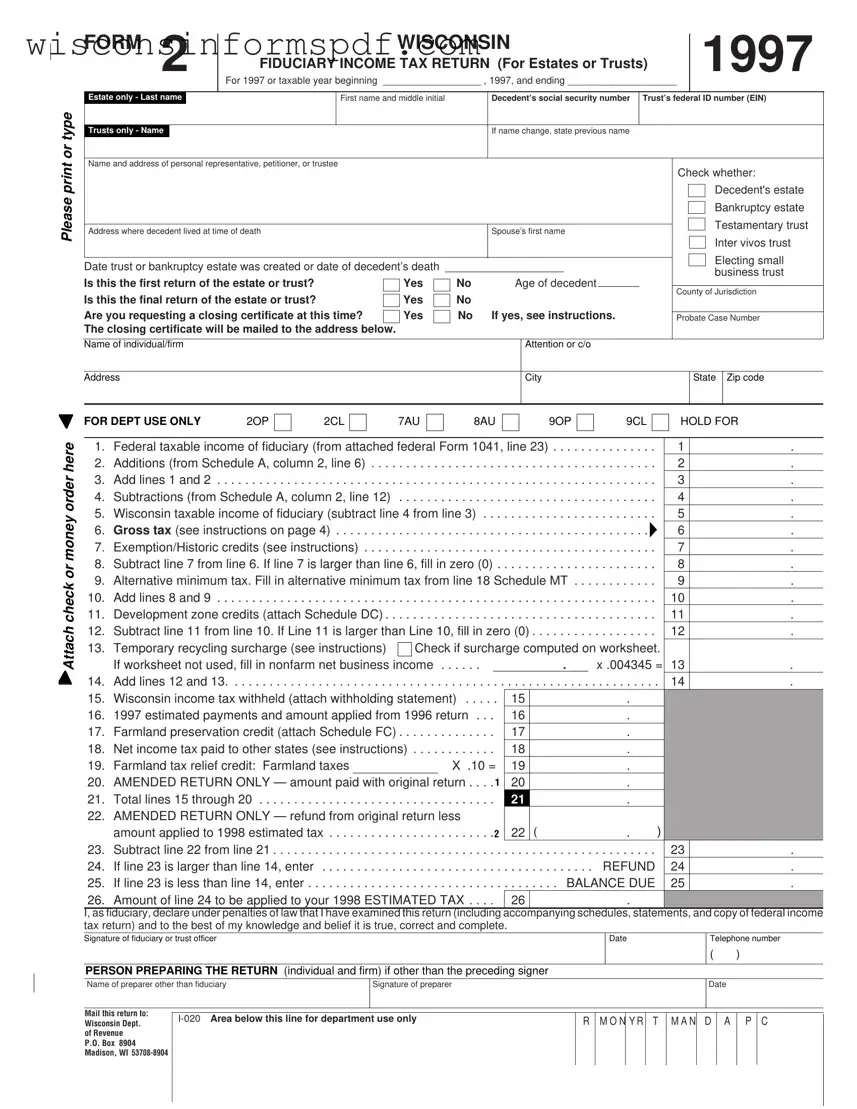

In navigating the complexity of fiduciary responsibilities, understanding and completing the Wisconsin Form 2 for Fiduciary Income Tax Return is crucial for estates and trusts. This detailed document, specifically designed for the 1997 tax year or for taxable years beginning in 1997, serves as a comprehensive guide for personal representatives, trustees, or petitioners in accurately reporting income for either estates or trusts. Aiming to streamline the tax filing process, this form covers various essential aspects, including the decedent's social security number or the trust's federal ID number, alongside details about the estate or trust's creation and the decedent's last known address. Crucially, it explores whether it's the first or final return for the entity, and it even delves into requests for closing certificates. The form further breaks down into specifics, requesting detailed income calculations and tax obligations, encompassing federal taxable income adjustments, addition and subtraction adjustments required according to Wisconsin's unique tax laws, and potential tax credits. The form also outlines requirements for attaching accompanying documents, such as the federal Form 1041 and schedules, Wisconsin Schedules 2K-1 and WD if applicable, and additional documentation that may be necessary for closing certificate requests for estates or trusts. Filing Form 2 is a testament to the intricate balance of adhering to legal requirements while ensuring the financial activities of estates or trusts are accurately represented to the Wisconsin Department of Revenue.

or type

FORM |

2 |

|

WISCONSIN |

1997 |

||||

|

|

|

|

|

||||

|

|

|

|

FIDUCIARY INCOME TAX RETURN (For Estates or Trusts) |

|

|||

|

|

|

|

For 1997 or taxable year beginning __________________ , 1997, and ending ____________________ |

|

|||

|

|

|

|

|

|

|

|

|

Estate only - Last name |

|

|

First name and middle initial |

Decedent’s social security number |

Trust’s federal ID number (EIN) |

|||

|

|

|

|

|

|

|

|

|

Trusts only - Name |

|

|

|

|

If name change, state previous name |

|

||

|

|

|

|

|

|

|

|

|

Please print

Name and address of personal representative, petitioner, or trustee

Address where decedent lived at time of death |

Spouse’s first name |

|

|

Date trust or bankruptcy estate was created or date of decedent’s death ___________________

Is this the first return of the estate or trust? |

|

Yes |

|

No |

Age of decedent |

|

|

|

|

||||

|

|

|

|

|

|

|

Is this the final return of the estate or trust? |

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

Are you requesting a closing certificate at this time? |

|

Yes |

|

No |

If yes, see instructions. |

|

The closing certificate will be mailed to the address below. |

|

|

|

|

|

|

Check whether: Decedent's estate

Bankruptcy estate

Testamentary trust

Inter vivos trust

Electing small business trust

County of Jurisdiction

Probate Case Number

Name of individual/firm |

Attention or c/o |

|

|

|

|

|

|

Address |

City |

State |

Zip code |

|

|

|

|

Attach check or money order here

FOR DEPT USE ONLY |

2OP |

2CL |

7AU |

8AU |

|

|

9OP |

9CL |

|

HOLD FOR |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

1. |

Federal taxable income of fiduciary (from attached federal Form 1041, line 23) |

. . . . . |

. . . . . . . . . |

. |

|

1 |

|

. |

|||||||||

2. |

Additions (from Schedule A, column 2, line 6) . . . . |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

2 |

|

. |

|||||

3. |

Add lines 1 and 2 . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

3 |

|

. |

||||

4. |

Subtractions (from Schedule A, column 2, line 12) |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

4 |

|

. |

|||||

5. |

Wisconsin taxable income of fiduciary (subtract line 4 from line 3) |

. . . . . . . . |

. . . . . . . . . |

. |

|

5 |

|

. |

|||||||||

6. |

. . . . . . . . . . . . . . .Gross tax (see instructions on page 4) |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

6 |

|

. |

||||||

7. |

Exemption/Historic credits (see instructions) |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

7 |

|

. |

|||||

8. |

Subtract line 7 from line 6. If line 7 is larger than line 6, fill in zero (0) . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

8 |

|

. |

||||||||

9. |

Alternative minimum tax. Fill in alternative minimum tax from line 18 Schedule MT . . |

. . . . . . . . . |

. |

|

9 |

|

. |

||||||||||

10. |

Add lines 8 and 9 . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

10 |

|

. |

||||

11. |

Development zone credits (attach Schedule DC) . . |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

11 |

|

. |

|||||

12. |

Subtract line 11 from line 10. If Line 11 is larger than Line 10, fill in zero (0) |

. . . . . . . . |

. . . . . . . . . |

. |

|

12 |

|

. |

|||||||||

13. |

Temporary recycling surcharge (see instructions) |

Check if surcharge computed on worksheet. |

|

|

|

||||||||||||

|

If worksheet not used, fill in nonfarm net business income . . . . |

. . |

|

|

|

. |

x .004345 = |

13 |

|

. |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

Add lines 12 and 13. . . |

. . . . . . . . . . . |

. . . . |

. . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

. . |

. . . . . . . . . . . . . . . |

. |

14 |

|

. |

|||||

15. |

Wisconsin income tax withheld (attach withholding statement) |

15 |

|

|

. |

|

|

|

|

|

|||||||

16. |

1997 estimated payments and amount applied from 1996 return . . . |

16 |

|

|

. |

|

|

|

|

|

|||||||

17. |

Farmland preservation credit (attach Schedule FC) |

. . . . . . |

. . . . |

. . . . |

17 |

|

|

. |

|

|

|

|

|

||||

18. |

Net income tax paid to other states (see instructions) |

. . . . |

18 |

|

|

. |

|

|

|

|

|

||||||

19. |

Farmland tax relief credit: Farmland taxes |

|

|

X |

.10 = |

19 |

|

|

. |

|

|

|

|

|

|||

20. |

AMENDED RETURN ONLY — amount paid with original return |

. . . . 1 |

20 |

|

|

. |

|

|

|

|

|

||||||

21. |

. . . . . . . . . . . . . . . . . . . .Total lines 15 through 20 |

. . . . . . |

. . . . |

. . . . |

21 |

|

|

. |

|

|

|

|

|

||||

22. |

AMENDED RETURN ONLY — refund from original return less |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

amount applied to 1998 estimated tax |

. . . . . . . . . . |

. . . . . . |

. . . . |

. . . .2 |

22 |

( |

|

. |

|

) |

|

|

|

|||

23. |

Subtract line 22 from line 21 |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. . . . . . . . . |

. |

|

23 |

|

. |

|||||

24. |

If line 23 is larger than line 14, enter |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . . . . . . |

. REFUND |

|

24 |

|

. |

||||||

25. |

If line 23 is less than line 14, enter |

. . . . . . |

. . . . |

. . . . . |

. . . . |

. . . |

. BALANCE DUE |

|

25 |

|

. |

||||||

26. |

Amount of line 24 to be applied to your 1998 ESTIMATED TAX |

. . . . |

26 |

|

|

. |

|

|

|

|

|

||||||

I, as fiduciary, declare under penalties of law that I have examined this return (including accompanying schedules, statements, and copy of federal income tax return) and to the best of my knowledge and belief it is true, correct and complete.

Signature of fiduciary or trust officer |

Date |

Telephone number |

|

|

|

( |

|

) |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PERSON PREPARING THE RETURN (individual and firm) if other than the preceding signer |

|

|

|

|

|

|

|

|

|

|

|

||

Name of preparer other than fiduciary |

Signature of preparer |

|

|

|

|

|

|

Date |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mail this return to: |

|

|

|

|

|

|

|

|

|

|

|

|

|

R |

M O N |

Y R |

T |

M A N |

D |

A |

|

P |

C |

||||

Wisconsin Dept. |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

|

P.O. Box 8904 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Madison, WI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 2 (1997)Page 2

SCHEDULE A — MODIFICATIONS AND ADJUSTMENTS |

COL. 1 |

COL. 2 |

|

ADDITIONS: |

Distributable Income |

||

1. |

Adjustment to convert 1997 federal taxable income to the level allowable under |

|

|

|

the Internal Revenue Code in effect on August 5, 1997 (Schedule B) |

|

. |

2. |

Interest (less related expenses) on state and municipal obligations |

. |

. |

3. |

State and local taxes (see instructions) |

. |

. |

4. |

Capital gain/loss adjustment (see instructions) |

. |

. |

5. |

Other (specify) |

. |

. |

6. |

Total additions (add lines 1 through 5) |

. |

. |

SUBTRACTIONS: |

|

|

|

7. |

Adjustment to convert 1997 federal taxable income to the level allowable under |

|

|

|

|

||

|

the Internal Revenue Code in effect on August 5, 1997 (Schedule B) |

|

. |

8. |

Interest (less related expenses) on obligations of the United States |

. |

. |

9. |

Capital gain/loss adjustment (see instructions) |

|

. |

. . . . . . . . . . . . . . . . . . .10. State and local income tax refunds (see instructions) |

. |

. |

|

11. |

Other (specify) |

. |

. |

12. Total subtractions (add lines 7 through 11) |

. |

. |

|

SCHEDULE B — ADJUSTMENTS TO CONVERT 1997 FEDERAL TAXABLE INCOME TO THE LEVEL ALLOWABLE UNDER THE INTERNAL REVENUE CODE IN EFFECT ON AUGUST 5, 1997 (see instructions on page 11)

|

|

|

|

|

|

|

Adjustments for 1997 |

|||||

1 NATURE OF |

|

|

|

|

|

|

|

|

||||

|

Distributable |

|

|

|||||||||

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

TOTAL |

(If total increases federal taxable income, enter on Schedule A, line 1) |

|

|

|

|

|

|

|

|

||

(If total decreases federal taxable income, enter on Schedule A, line 7) |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

TOTAL (enter, as appropriate, on Wisconsin Schedule |

|

|

|

|

|

|

|

|

|||

SCHEDULE C — ADJUSTMENTS TO CAPITAL GAINS/LOSSES BECAUSE CAPITAL ASSETS DISPOSED OF |

|

|

|

|||||||||

|

|

|

|

HAD DIFFERENT BASIS FOR WISCONSIN AND FEDERAL INCOME TAX PURPOSES |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

1a |

|

DESCRIPTION OF CAPITAL ASSETS HELD ONE YEAR OR LESS |

A. FEDERAL |

B. WISCONSIN |

|

|

C. DIFFERENCE |

|||||

|

|

|

|

AND REASON FOR DIFFERENCE IN BASIS |

ADJUSTED BASIS |

ADJUSTED BASIS |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

1b TOTAL – Combine amounts in column C. Fill in here and on line 4 of Wisconsin Schedule WD (Form 2) |

......................... |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2a |

|

DESCRIPTION OF CAPITAL ASSETS HELD MORE THAN ONE YEAR |

A. FEDERAL |

B. WISCONSIN |

|

|

C. DIFFERENCE |

|||||

|

|

|

|

AND REASON FOR DIFFERENCE IN BASIS |

ADJUSTED BASIS |

ADJUSTED BASIS |

|

|||||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

2b TOTAL – Combine amounts in column C. Fill in here and on line 12 of Wisconsin Schedule WD (Form 2) |

....................... |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INFORMATION REQUIRED WHEN REQUESTING A CLOSING CERTIFICATE FOR AN ESTATE |

|

|

|

|||||

1 |

Did the decedent have a will? |

yes |

no |

|

2 |

Type of Probate |

formal |

informal |

other |

3 |

Is there a requirement to file a federal estate tax return (Form 706)? Yes |

|||

No If Yes, date filed

4 If the decedent did not file tax returns prior to death, state the decedent’s approximate income for: 1997 - $ |

, |

||||

1996 - $ |

, 1995 - $ |

, 1994- $ |

. |

|

|

|

|

||||

5Attach a copy of the inventory and will. Attach a copy of the final account to the final fiduciary return.

6If an estate does not have enough income to require filing and needs a Closing Certificate for Fiduciaries, or if the estate will be filing only one fiduciary return when the estate is closed and needs the closing certificate before filing that return, see page 2 of the instructions for procedures to be followed.

INFORMATION REQUIRED WHEN REQUESTING A CLOSING CERTIFICATE FOR A TRUST

1Attach a copy of the trust instrument with amendments and copies of annual court accountings for past three years.

2a. Name(s) of grantor(s) ______________________________________________________________________________________________

Social Security Number(s) _____________________________________ __________________________________________

b. Name(s) of grantee(s) _____________________________________________________________________________________________

Social Security Number(s) _____________________________________ |

__________________________________________ |

3State reason for closing the trust ________________________________________________________________________________________

__________________________________________________________________________________________________________________

4 Is a certificate required by the court? |

Yes |

No See page 2 of instructions (requests for closing certificates). |

|

|

|

ATTACH A COPY OF FEDERAL FORM 1041 AND SCHEDULES TO THIS RETURN.

ALSO ATTACH COPIES OF WISCONSIN SCHEDULES

| Fact Number | Fact Detail |

|---|---|

| 1 | Form Name: Wisconsin Form 2 - 1997 Fiduciary Income Tax Return (For Estates or Trusts) |

| 2 | Applicable Year: 1997 or taxable year beginning in 1997 |

| 3 | Applicability: Used for filing income tax returns for estates or trusts in Wisconsin |

| 4 | Required Identifiers: Decedent’s social security number for estates; Trust’s federal ID number (EIN) for trusts |

| 5 | Governing Law: Internal Revenue Code as effective on August 5, 1997, along with Wisconsin state specific modifications |

| 6 | Sections Include: Information on the estate or trust, income calculations, tax calculations, and signatures |

| 7 | Key Components: Federal taxable income of fiduciary adjustments, Wisconsin taxable income, tax credits, and surcharges |

| 8 | Attachment Requirements: Copy of federal Form 1041, Wisconsin Schedules 2K-1 and WD (Form 2), if applicable |

Filling out the Wisconsin 2 form, officially known as the 1997 Fiduciary Income Tax Return for Estates or Trusts, is a straightforward process, but attention to detail is crucial. This form is used to report income, deductions, and credits of estates or trusts. It covers the specifics from the beginning of the 1997 taxable year or another starting point in 1997, through to the ending of that same year. Before jumping into the steps, make sure to have all necessary financial records at hand, including the federal Form 1041 and any schedules relevant to the estate or trust's financial activities throughout the year.

After submitting the form, keep a copy for record-keeping purposes. The processing of the return and any applicable refunds may take several weeks. Pay special attention to deadlines to avoid penalties for late filing.

What is the Wisconsin Form 2 used for?

Wisconsin Form 2 is used by estates or trusts to file their fiduciary income tax return. It's for reporting income, deductions, and credits of the estate or trust for the tax year. This form is necessary for managing the tax obligations related to income the estate or trust generates.

Who needs to file the Wisconsin Form 2?

Any estate or trust with income generated in Wisconsin is required to file Form 2. This includes estates of deceased individuals, trusts established by a will (testamentary trusts), living trusts (inter vivos trusts), and certain bankruptcy estates. If you're a personal representative, trustee, or petitioner managing such entities, you'll likely need to complete this form.

Is there a deadline for filing Form 2 in Wisconsin?

Yes, the Wisconsin Form 2 typically must be filed by April 15 of the year following the tax year being reported. If the estate or trust operates on a fiscal year rather than a calendar year, the filing deadline is the 15th day of the fourth month after the close of the fiscal year.

Can I request a closing certificate using Form 2?

Yes, you can request a closing certificate for fiduciaries by indicating "Yes" on the form where asked if you are requesting a closing certificate at this time. This certificate is important as it officially closes the estate or trust with the Wisconsin Department of Revenue.

What information do I need to complete Form 2?

You'll need the estate's or trust's federal ID number (EIN), the decedent's Social Security number for estates, details about income and deductions reported to the IRS, and any specific state adjustments. Additionally, information about the personal representative, petitioner, or trustee is required alongside any schedules or additional forms that support your tax return.

What are the key parts of Form 2?

Key sections include reporting federal taxable income, making Wisconsin-specific adjustments, calculating Wisconsin taxable income, applying tax rates, and claiming any available credits. You'll also report any Wisconsin income tax withheld and make payments or refunds.

How do I calculate Wisconsin taxable income on Form 2?

Start with the federal taxable income reported on the federal Form 1041 and make adjustments as outlined in the Wisconsin Form 2 instructions. This includes additions and subtractions specific to Wisconsin law. The resulting figure is the Wisconsin taxable income for the estate or trust.

What happens if I file Form 2 late?

Filing late can result in penalties and interest charges on any unpaid tax due to the state. To avoid these, it's crucial to file on time or request an extension if you need more time to prepare an accurate return.

Can I file Form 2 electronically?

As of the latest updates, Wisconsin allows for electronic filing of Form 2 for estates and trusts. Filing electronically is faster, more secure, and can expedite the processing of your return and any refunds due.

Where do I mail my completed Wisconsin Form 2?

If you're submitting your Form 2 on paper, mail it to the Wisconsin Department of Revenue at the following address: P.O. Box 8904, Madison, WI 53708-8904. Make sure all supporting documents are attached and that the form is signed and dated correctly.

Filling out the Wisconsin Form 2 for Estates or Trusts can seem straightforward at first glance. However, common mistakes often occur that can delay processing or impact the accuracy of tax responsibilities. Here are eight common pitfalls to avoid:

To ensure a smooth filing process, pay careful attention to the details. Double-check each section for accuracy and completeness before submission. Taking the time to thoroughly review the return and attached documentation can save time, frustration, and potentially money in the long term.

When in doubt, consult the instructions provided with the Form 2 or seek professional advice. The complexity of fiduciary taxes cannot be understated, and ensuring compliance with state and federal tax laws protects the interests of the estate or trust and its beneficiaries.

When filling out the Form 2 for Wisconsin Fiduciary Income Tax Return (for Estates or Trusts), there are several critical documents and forms that you often need to complete or have at hand to make sure your submission is thorough and accurate. These documents complement Form 2 by providing detailed financial information, evidence of compliance with federal tax obligations, and specifics about the assets and income of the estate or trust. It's essential to familiarize yourself with these documents whether you're preparing for an initial filing or finalizing the tax matters of an estate or trust.

Understanding and accurately completing these documents in conjunction with Form 2 is essential for the correct filing of Wisconsin Fiduciary Income Tax Returns for estates and trusts. These documents ensure compliance with both state and federal tax laws, allow for accurate tax calculations, and provide clarity on the distribution of the estate or trust's income. They collectively form a comprehensive account of the estate or trust's financial activities over the tax year, making thorough preparation and attention to detail paramount in their completion.

The Wisconsin Form 2, serving estates or trusts for fiduciary income tax purposes, shares similarities with the Federal Form 1041, U.S. Income Tax Return for Estates and Trusts. Specifically, both forms require information about the income, deductions, and credits of the estate or trust, aiming to calculate the tax liability based on these details. They also include sections for reporting adjustments to income that may not align with the standard federal income tax code.

Another document akin to the Wisconsin Form 2 is the Schedule A (Modifications and Adjustments), which is integral to the Form 2 itself. This schedule details additions and subtractions to the fiduciary's federal taxable income to arrive at the Wisconsin taxable income, mirroring how adjustments are made on Federal Schedule 1 (Additional Income and Adjustments), albeit for personal income tax.

The Schedule B (Adjustments), also part of the Wisconsin Form 2 package, mirrors the purpose of federal adjustments documents, though specifically geared towards adjusting 1997 federal taxable income to comply with previous Internal Revenue Codes. This is an example of a state-specific adaptation of broader federal income adjustment processes, which are more generally seen in documents such as the Federal Form 1040 adjustments sections.

Similar to the Schedule C (Adjustments to Capital Gains/Losses) associated with Wisconsin's Form 2, the Federal Schedule D (Capital Gains and Losses) serves to report the sale or exchange of capital assets. Both schedules require detailed reporting on the basis and adjustments to the gains or losses of capital assets, though Schedule C focuses on reconciling differences between Wisconsin and federal tax bases.

The Information Required When Requesting a Closing Certificate section of the Wisconsin Form 2 resembles other estate closure documents used across various states, such as the Executor's/ Administrator's Deed or the Estate Tax Closing Letter. These documents help formalize the process of closing an estate, ensuring all tax liabilities have been addressed, which is fundamental for the distribution phase to proceed without legal implications.

The Wisconsin form shares similarities with the United States Estate (and Generation-Skipping Transfer) Tax Return, Form 706, in that both deal with the financial aspects of an estate after a death. While the Wisconsin Form 2 addresses income tax responsibilities for estates or trusts, Form 706 focuses on calculating federal estate tax liabilities, demonstrating the intersection of income and estate taxes during estate settlement.

Documents related to generating a Closing Certificate for Fiduciaries, like those instructions found with the Wisconsin Form 2, are also echoed in different jurisdictions through forms or letters such as the Trust Closing Letter. These are pivotal in showing that a trust has fulfilled its tax obligations and can be formally closed, a universal requirement across state and federal levels.

Lastly, the requirement to attach a copy of Federal Form 1041 and its schedules when submitting Wisconsin's Form 2 draws a parallel to the interdependence seen between state and federal tax filings for individuals, such as linking Federal Form 1040 with state income tax returns. This relationship ensures consistency and compliance across tax jurisdictions, highlighting how state documents often complement federal filings to provide a complete tax picture.

Filling out the Wisconsin Form 2, the Fiduciary Income Tax Return for Estates or Trusts, requires careful attention to ensure accuracy and compliance. Here are some key dos and don'ts to guide you through the process:

Following these guidelines can streamline the process of completing the Wisconsin Form 2 and help ensure that the fiduciary income tax return for your estate or trust is filled out accurately and in compliance with state requirements.

When it comes to navigating tax forms, especially those as specific as the Wisconsin Form 2 for fiduciary income tax returns, it's easy to run into misunderstandings. Here are nine common misconceptions about the Wisconsin Form 2 and the facts behind them:

Understanding these nuances ensures that fiduciaries can accurately complete the Form 2 and comply with Wisconsin's tax laws. It's always advised to review the instructions carefully or consult a tax professional when preparing tax returns for estates or trusts.

Filing the Wisconsin 2 form, which serves as the 1997 Fiduciary Income Tax Return for Estates or Trusts, requires attention to detail and careful adherence to specific instructions. Here are key takeaways to ensure the process is handled correctly:

It’s essential to follow the specific guidelines and provide comprehensive and accurate information throughout the return to avoid errors or delays in processing. Ensuring all documentation is attached and properly filled out will facilitate a smoother handling of the estate or trust’s tax obligations to the State of Wisconsin.

Dept of Financial Institutions - Includes a direct way for nonprofits to provide their contact information for official records.

Wisconsin Permit - An option to exclude personal information from public records lists is available through the MV3001 form.

Real Estate Executive Summary Example - Identifies the conditions under which a unit owner may rent out their condominium, including any limitations or rules set by the association.