Fill Your Wisconsin 5S Form

Fill Your Wisconsin 5S Form

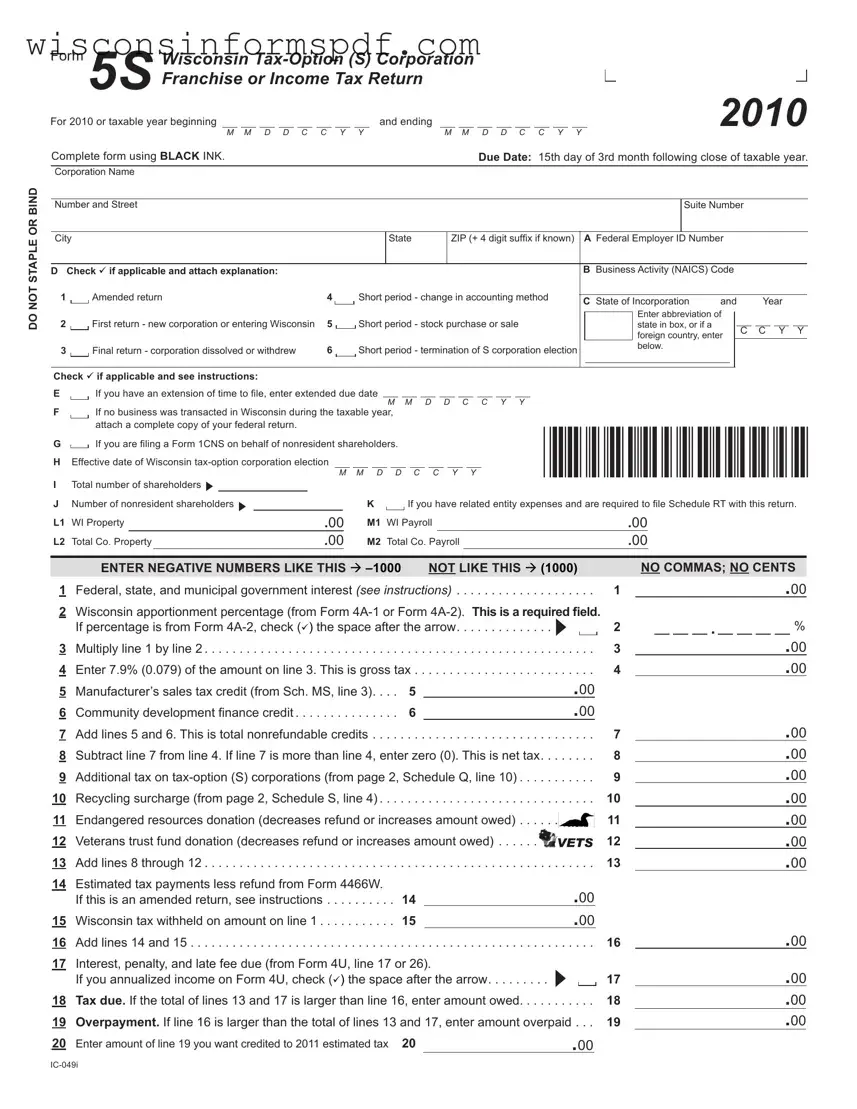

Filing the Form 5S in Wisconsin is a critical process for entities operating as S corporations within the state, encompassing a comprehensive detail on income, losses, deductions, and credits relevant to the corporation's tax responsibilities. This form, specifically designed for Tax-Option (S) Corporations, requires accurate completion with black ink and adherence to the due date, which falls on the 15th day of the 3rd month following the close of the taxable year. It begins by collecting basic but essential information about the corporation, including name, address, and Federal Employer Identification Number, moving on to more detailed sections that demand inputs on business activity codes, the state of incorporation, and specifics such as amended returns or indication of a short period due to accounting method changes. Moreover, it delves into financial specifics, requesting details on federal, state, and municipal interest, Wisconsin apportionment percentage, and calculations for net tax after credits. The form also addresses additional taxes pertinent to specific situations like recycling surcharge and shareholders’ distribution. For those corporations with operations spanning beyond state lines or engaging in international transactions, it captures the essence of such activities, ensuring that tax obligations are met both within and outside Wisconsin. Lastly, directives for attaching the federal Form 1120S and other necessary schedules highlight the interconnectedness of state and federal tax filings, underscoring the importance of thorough, accurate, and timely submission to avoid penalties and maximize compliance.

DO NOT STAPLE OR BIND

Form |

5S |

Wisconsin |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

Franchise or Income Tax Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2010 |

||||||||||||||||||

|

|

|

M M D D C |

C Y |

|

Y |

M M D D C C Y Y |

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

For 2010 or taxable year beginning |

|

|

|

|

|

and ending |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Complete form using BLACK INK. |

|

|

|

|

|

|

|

|

|

|

|

|

Due Date: 15th day of 3rd month following close of taxable year. |

|||||||||||||||||||||||||||||||

Corporation Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Number and Street |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Suite Number |

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

City |

|

|

|

|

|

|

|

|

State |

|

ZIP (+ 4 digit sufix if known) |

A Federal Employer ID Number |

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

D Check if applicable and attach explanation: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B Business Activity (NAICS) Code |

|

|

|

|

|

|

|

|

|||||||||||

1 |

|

Amended return |

4 |

|

|

Short period - change in accounting method |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

C State of Incorporation |

and |

|

|

Year |

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

2 |

|

First return - new corporation or entering Wisconsin |

5 |

|

|

Short period - stock purchase or sale |

|

|

|

|

Enter abbreviation of |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

state in box, or if a |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

C |

|

C Y Y |

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

foreign country, enter |

|

|

||||||||||

3 |

|

Final return - corporation dissolved or withdrew |

6 |

|

|

Short period - termination of S corporation election |

|

|

|

|

below. |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Check if applicable and see instructions:

E If you have an extension of time to ile, enter extended due date M M D D C C Y Y

FIf no business was transacted in Wisconsin during the taxable year, attach a complete copy of your federal return.

G If you are iling a Form 1CNS on behalf of nonresident shareholders.

HEffective date of Wisconsin

|

|

|

|

|

|

|

M |

|

M |

|

D |

|

D |

|

C |

|

C |

|

Y |

|

Y |

|

|

|

|

|

|

||||

I |

Total number of shareholders |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

J |

Number of nonresident shareholders |

|

|

|

|

|

K |

|

|

|

|

If you have related entity expenses and are required to ile Schedule RT with this return. |

|||||||||||||||||||

L1 |

WI Property |

|

.00 |

|

M1 |

WI Payroll |

|

.00 |

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

L2 |

Total Co. Property |

.00 |

|

|

M2 |

Total Co. Payroll |

|

.00 |

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ENTER NEGATIVE NUMBERS LIKE THIS |

|

|

|

NOT LIKE THIS (1000) |

|

|

NO COMMAS; NO CENTS |

|||||||||||||||||||||||

1 |

Federal, state, and municipal government interest (see instructions) |

1 |

|

.00 |

|||||||||||||||||||||||||||

2Wisconsin apportionment percentage (from Form

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

. |

% |

||||||||

|

If percentage is from Form |

|

|

|

|

|

|

|

|

|

|||||||||||||

3 |

Multiply line 1 by line 2 |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. 3. . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

00 |

|||

4 |

Enter 7.9% (0.079) of the amount on line 3. This is gross tax |

. 4. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

5 |

.Manufacturer’s sales tax credit (from Sch. MS, line 3). . . |

5 |

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

Community development inance credit |

6 |

|

.00 |

|

|

|

|

|

|

|

|

|

|

.00 |

||||||||

7 |

Add lines 5 and 6. This is total nonrefundable credits . . . . |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. 7. . |

|

|

|

|

|

|

|

|

|||||||||||

8 |

Subtract line 7 from line 4. If line 7 is more than line 4, enter zero (0). This is net tax |

. 8.. |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

9 |

Additional tax on |

. 9. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

10 |

Recycling surcharge (from page 2, Schedule S, line 4) . . . |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. 10. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||

11 |

Endangered resources donation (decreases refund or increases amount owed) |

11 |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

12 |

Veterans trust fund donation (decreases refund or increases amount owed) |

. 12. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

13 |

Add lines 8 through 12 |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. 13. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||

14 |

Estimated tax payments less refund from Form 4466W. |

14 |

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If this is an amended return, see instructions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

15 |

Wisconsin tax withheld on amount on line 1 |

15 |

|

.00 |

|

|

|

|

|

|

|

|

|

|

.00 |

||||||||

16 |

Add lines 14 and 15 |

. . . . |

. . . . . . . . . . . . . . . . . . . . . |

. 16. . |

|

|

|

|

|

|

|

|

|||||||||||

17 |

Interest, penalty, and late fee due (from Form 4U, line 17 or 26). |

|

|

17 |

|

|

|

|

|

|

|

|

.00 |

||||||||||

|

If you annualized income on Form 4U, check () the space after the arrow |

|

|

|

|

|

|

|

|

||||||||||||||

18 |

Tax due. If the total of lines 13 and 17 is larger than line 16, enter amount owed |

. 18. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

19 |

Overpayment. If line 16 is larger than the total of lines 13 and 17, enter amount overpaid |

. 19. . |

|

|

|

|

|

|

|

|

.00 |

||||||||||||

20 |

Enter amount of line 19 you want credited to 2011 estimated tax |

20 |

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2010 Form 5S |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 2 of 4 |

|

||||||||||

21 |

Subtract line 20 from line 19. This is your refund |

. . . . . . . . . . . . . . |

. . |

|

21 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

22 |

Enter total company gross receipts from all activities (see instructions) . . |

. . . . . . . . . . . . . . |

. . |

|

22 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

23 |

Enter total company assets from federal Form 1120S, item F |

. . . . . . . . . . . . . . |

. . |

|

23 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

24 |

If the |

24 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||||||

|

shareholders, enter total amount paid for all shareholders for the taxable year |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Schedule Q - Additional Tax on Certain |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||

1 |

Excess of recognized |

1 |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

2 |

Wisconsin taxable income before apportionment (attach computation schedule) |

2 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||||||

3 |

Enter the smaller of line 1 or line 2. This is the net recognized |

3 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||||||

4 |

Wisconsin apportionment percentage (from Form |

4 |

. |

% |

|

|||||||||||||||||||||||||||

|

required ield. If percentage is from Form |

|

||||||||||||||||||||||||||||||

5 |

Multiply line 3 by line 4 |

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

. . . . . . . . . . . . . . |

. . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

6 |

Wisconsin net business loss carryforward (attach schedule) |

. . . . . |

. . . |

|

6 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

7 |

Subtract line 6 from line 5 |

. . . . . . . . . . . . . . |

. . . |

|

7 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

8 |

Enter 7.9% (0.079) of the amount on line 7 |

. . . . . |

. . . |

|

8 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

9 |

Community development inance credit |

. . . . . |

. . . |

|

9 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||

10 |

Subtract line 9 from line 8. This is the additional tax to enter on Form 5S, page 1, line 9 |

10 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule S - Recycling Surcharge |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 Enter net income (loss) (see instructions) |

. . . . . . . . . . . . . . |

. . . |

|

1 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||||||||||

2 Wisconsin apportionment percentage (from Form |

|

|

. |

% |

|

|||||||||||||||||||||||||||

|

required ield. If percentage is from Form |

2 |

|

|||||||||||||||||||||||||||||

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3 Multiply line 1 by line 2 |

. . . . . . . . . . . . . . |

. . . |

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||||||||

4 Enter the greater of $25 or 0.2% (0.002) of the amount on line 3, but not more than $9,800. |

4 |

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||||||||||||||||||

|

This is the recycling surcharge to enter on Form 5S, page 1, line 10 . . . . |

. . . . . . . . . . . . . . |

. . . |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Additional Information Required |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1 |

Person to contact concerning this return: |

|

Phone #: |

|

|

|

|

|

|

Fax #: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

2City and state where books and records are located for audit purposes:

3 Are you the sole owner of any QSubs or LLCs? |

|

Yes |

|

No If yes, attach a list of the names and federal EINs of your |

||||

solely owned QSubs and LLCs. Did you include the incomes of these entities in this return? |

|

Yes |

|

No |

||||

4Did you purchase any taxable tangible personal property or taxable services for storage, use, or consumption in Wisconsin with-

out payment of a state sales or use tax? |

|

Yes |

|

No If yes, you owe Wisconsin use tax. See instructions for how to |

report use tax. |

|

|

|

|

5Did any adjustments made by the Internal Revenue Service to your income for prior years become inalized during this year?

Yes |

|

No If yes, see instructions and indicate years adjusted: |

6List the locations of your Wisconsin operations:

Under penalties of law, I declare that this return and all attachments are true, correct, and complete to the best of my knowledge and belief.

Signature of Oficer

Title

Date

Preparer’s Signature

Preparer’s Federal Employer ID Number

Date

You must ile a copy of your federal Form 1120S with Form 5S, even if no Wisconsin activity.

If you are not iling electronically, make your check payable to and mail your return to:

Wisconsin Department of Revenue

PO Box 8908

Madison WI

2010 Form 5S |

Page 3 of 4 |

Income (Loss)

Deductions

Credits

Foreign Transactions

Schedule 5K – Shareholders’ Pro Rata Share Items

|

|

(a) Pro rata share items |

|

|

(b) Federal amount |

(c) Adjustment |

|

(d) Amount under Wis. law |

|||

1 |

Ordinary business income (loss) |

. |

|

|

|

|

|

|

|||

2 |

. . . . .Net rental real estate income (loss) (attach Form 8825) |

. |

|

|

|

|

|

|

|||

3 |

. . . . . . . . . . .Other net rental income (loss) (attach schedule) |

. |

|

|

|

|

|

|

|||

4 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Interest income |

. |

|

|

|

|

|

|

|||

5 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Ordinary dividends |

. |

|

|

|

|

|

|

|||

6 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Royalties |

. |

|

|

|

|

|

|

|||

7 |

. . . . . . . . . . . . . . . . . . . . . . .Net |

. |

|

|

|

|

|

|

|||

8 |

. . . . . . . . . . . . . . . . . . . . . . . .Net |

. |

|

|

|

|

|

|

|||

9 |

. . . . . . . . . . .Net section 1231 gain (loss) (attach Form 4797) |

. |

|

|

|

|

|

|

|||

10 |

. . . . . . . . . . . . . . . . . . .Other income (loss) (attach schedule) |

. |

|

|

|

|

|

|

|||

11 |

. . . . . . . . . . . . . . .Section 179 deduction (attach Form 4562) |

. |

|

|

|

|

|

|

|||

12 |

a |

. . . . . . . . . . . . . . . .Contributions |

. |

|

|

|

|

|

|

||

|

b |

. . . . . . . . . . . . . . . .Investment interest expense |

. |

|

|

|

|

|

|

||

|

c |

Section 59(e)(2) expenditures (1) Type |

|

|

|

|

|

|

|

|

|

|

|

(2) Amount |

. |

|

|

|

|

|

|

||

|

d |

. . . . . . . . . . . . . . . .Other deductions (attach schedule) . . . |

. |

|

|

|

|

|

|

||

13 |

a |

Manufacturing investment credit - from carryover at shareholder level |

|

|

|||||||

|

b |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Manufacturing investment credit - from carryover at entity level |

|

||||||||

|

c |

. . . . . . . . . . . . . .Dairy and livestock farm investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

d |

. . .Health Insurance |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

e |

. . . . . . . . . . . . . . . .Ethanol and biodiesel fuel pump credit. |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

f |

. . . . . . . . . . . . . . . .Development zones credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

g |

. . . . . . . . .Development opportunity zone investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

h |

. . . . . . . . . . . .Development zone capital investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

i |

. . . . . . . . . . . . . . . .Economic development tax credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

j |

. . . . . . . . . . . . . . . .Technology zone credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

k |

. . . . . . . . . . . . . . . .Early stage seed investment credit. . . . |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

l |

. . . . .Supplement to federal historic rehabilitation tax credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

. . . . . . . . . . . . . . . . . . . . . . . . . . .m Internet equipment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

|||||

|

n |

. . . . . . . . . . .Dairy manufacturing facility investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

o |

. . . . . . . . . . . . . . . .Dairy cooperatives credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

p |

. . . . . . . . . . . . . .Meat processing facility investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

q |

. . . . . . . . . . . . . . . .Enterprise zone jobs credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

r |

. . . . . . . . . . . . . . . .Film production services credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

s |

. . . . . . . . . . . . .Film production company investment credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

t |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Food processing plant and food warehouse investment credit |

|

||||||||

|

u |

. . . . . . . . . . . . . . . .Jobs tax credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

v |

. . . . . . . . . . . . . . . .Postsecondary education credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

w |

. . . . . . . .Woody biomass harvesting and processing credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

x |

. . . . . . . . . . . . . . . .Water consumption credit |

. . |

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . |

|

|

||||

|

yy Tax paid to other states (enter postal abbreviation of state) |

(1) |

|

|

. . . . . . . . . . . . . . |

|

|

||||

|

|

|

|

|

|

||||||

|

|

|

|

(2) |

|

|

. . . . . . . . . . . . . . |

|

|

||

|

|

|

|

(3) |

|

|

. . . . . . . . . . . . . . |

|

|

||

|

zz Wisconsin tax withheld (do not include tax properly claimed on page 1, line 15) |

. . . . . . . . . . . . . . |

|

|

|||||||

14 |

a |

. . . . . . . . . . . . . . . .Name of country or U.S. possession . . |

. |

|

|

|

|

|

|

||

|

b |

. . . . . . . . . . . . . . . .Gross income from all sources |

. |

|

|

|

|

|

|

||

|

c |

. . . . . . . . . . . . .Gross income sourced at shareholder level |

. |

|

|

|

|

|

|

||

2010 Form 5S |

|

|

Page 4 of 4 |

(a) Pro rata share items |

(b) Federal amount |

(c) Adjustment |

(d) Amount under Wis. law |

Transactions

Foreign

Alternative |

Minimum (AMT) Items |

Tax |

Other

Foreign gross income sourced at corporate level:

dPassive category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

eGeneral category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

fOther (attach statement). . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Deductions allocated and apportioned at shareholder level:

gInterest expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

hOther. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Deductions allocated and apportioned at corporate level to foreign source income:

iPassive category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

jGeneral category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

kOther (attach statement). . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

Other information: |

|

|

|

|

|

|

l |

Total foreign taxes (check one): |

|

Paid |

|

|

Accrued . . . . |

|

m Reduction in taxes for credit (attach statement) |

. . . . . . . . . . |

|||||

|

n |

Other foreign tax information (attach statement) |

. . . . . . . . . . |

||||

15 |

a |

. . . . . . |

. . . . . . . . . . . . . . |

||||

|

b |

Adjusted gain or loss |

. . . . . . . . . . . . . . |

||||

|

c |

Depletion (other than oil and gas). . |

. . . . . . |

. . . . . . . . . . . . . . |

|||

|

d |

Oil, gas, and geothermal properties – gross income |

|||||

|

e |

Oil, gas, and geothermal properties – deductions |

|||||

|

f |

Other AMT items (attach schedule) |

. . . . . . |

. . . . . . . . . . . . . . |

|||

16 |

a |

. . . . . . . . . . . . . . |

|||||

|

b |

Other |

. . . . . . . . . . . . . . |

||||

|

c |

Nondeductible expenses |

. . . . . . . . . . . . . . |

||||

|

d |

Property distributions |

. . . . . . . . . . . . . . |

||||

|

e |

Repayment of loans from shareholders |

|||||

17 |

a |

Investment income |

. . . . . . . . . . . . . . |

||||

|

b |

Investment expenses |

. . . . . . . . . . . . . . |

||||

|

c |

Dividend distributions paid from accumulated earnings and proits |

|||||

|

d |

Other items and amounts (attach schedule) |

|

||||

18 |

a |

Related entity expense addback |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

||||

|

b |

Related entity expense allowable . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|||

19 |

Income/loss reconciliation (see instructions) |

||||||

20 |

Gross income (before deducting expenses) from all activities |

||||||

Schedule 5M – Analysis of Wisconsin Accumulated Adjustments Account and Other Adjustments Account

1 Balance at beginning of taxable year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2 Ordinary income from Schedule 5K, line 1, column d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Other additions (including separately stated items which increase income) (attach schedule) . . 4 Loss from Schedule 5K, line 1, column d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Other reductions (including separately stated items which reduce income) (attach schedule) . . .

6 Combine lines 1 through 5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Distributions other than dividend distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8 Subtract line 7 from line 6. This is balance at end of taxable year . . . . . . . . . . . . . . . . . . . . .

(a)Accumulated (b) Other Adjustments

|

Adjustments Account |

|

Account |

|

|

|

|

|

|

|

|

|

|

|

|

()

( |

) |

( |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fact | Detail |

|---|---|

| Name of Form | Form 5S Wisconsin Tax-Option (S) Corporation Franchise or Income Tax Return |

| Tax Year | 2010 |

| Ink Requirement | Complete form using BLACK INK |

| Due Date | 15th day of the 3rd month following the close of the taxable year |

| Governing Law | Wisconsin State Law |

| Submission Instructions | Do not staple or bind the documents; submit with a copy of the federal Form 1120S if not filing electronically |

Once the Wisconsin 5S form for Tax-Option (S) Corporation Franchise or Income Tax Return is completed, the corporation moves onto the next critical phase of its tax cycle. This involves awaiting any communications from the Wisconsin Department of Revenue regarding the submission, which may include requests for additional information or clarification. The corporation then needs to prepare for any payment obligations or anticipate refunds, as dictated by the finalized tax return calculations. It is also a time to ensure compliance with any changes or updates in legislation for future tax periods, and to plan accordingly for the next tax year to optimize tax positions and ensure compliance.

Completing the Wisconsin 5S form requires careful attention to detail and adherence to specified instructions. Ensure accuracy and completeness to fulfill your tax obligations and support a smooth processing of your return by the Wisconsin Department of Revenue.

What is the Form 5S used for?

The Form 5S is a tax document for Wisconsin Tax-Option (S) Corporations to file their franchise or income tax returns. It's used by corporations that have elected to be treated as an S corporation for tax purposes, allowing the corporation's income or losses to be passed through to the shareholders, who then report it on their personal tax returns.

When is Form 5S due?

This form is due on the 15th day of the third month following the close of the taxable year. For most S corporations, operating on a calendar year, the due date would be March 15 of the following year.

Which corporations need to file Form 5S?

Any corporation that has elected S corporation status for federal tax purposes and is operating in Wisconsin must file Form 5S. This requirement also includes S corporations that may not have conducted any business in Wisconsin during the taxable year but are registered or otherwise required to file in the state.

What if no business was transacted in Wisconsin during the taxable year?

In such cases, the corporation should still file Form 5S but must attach a complete copy of their federal return. This enables the Wisconsin Department of Revenue to verify that no Wisconsin-related income needs to be reported or taxed.

Are extensions available for filing Form 5S?

Yes, corporations can request an extension of time to file their Wisconsin income tax return. If granted, they should indicate the extended due date on Form 5S when filed. However, it's important to note that an extension to file is not an extension to pay any taxes due.

What attachments are required with Form 5S?

Depending on the corporation’s activities throughout the tax year, various attachments may be required. Common attachments include a completed Schedule RT for related entity expenses, documentation for any credits claimed, and a copy of the corporation's federal tax return. Specific situations, such as filing an amended return or claiming certain credits, may necessitate additional documentation.

How do nonresident shareholders affect the filing of Form 5S?

For S corporations with nonresident shareholders, Wisconsin requires the filing of Form 1CNS or equivalent, to ensure appropriate tax withholding and reporting for income attributable to Wisconsin. The total tax withheld for nonresident shareholders should be included and reported on Form 5S.

Where should Form 5S be filed and any payment sent?

If not filing electronically, the completed Form 5S and any payment due should be mailed to the Wisconsin Department of Revenue. The specific mailing address is provided on the form, ensuring it reaches the correct office for processing.

Filling out tax forms accurately is crucial to comply with state regulations and avoid potential fines. When it comes to the Wisconsin 5S Form, several common mistakes have been observed that can lead to complications or delays in processing. Here is a closer look at these errors:

Addressing these mistakes beforehand can streamline the process, ensuring compliance and avoiding possible penalties. It’s important that taxpayers pay careful attention to the detailed instructions provided for the Form 5S to mitigate any errors. Consulting with a tax professional or utilizing available resources from the Wisconsin Department of Revenue website may also be beneficial in clarifying any ambiguities and ensuring the accuracy of filed returns.

Remember, while some mistakes might seem trivial, they can lead to unnecessary delays or scrutiny. It's always better to double-check all entries and attached documentation before submission to ensure a smooth processing experience.

Filing a Wisconsin 5S Form, which is essential for Tax-Option (S) Corporations to report franchise or income tax, often requires additional documentation. Understanding these supplementary forms ensures thorough and accurate reporting, aiding both compliance and financial planning for businesses operating within the state. The following documents are commonly used alongside the primary form.

These forms together provide a comprehensive financial outline of the corporation's activities within the state of Wisconsin, ensuring that tax obligations are met accurately and in full. Accurate and timely filing, supported by the correct documentation, helps corporations avoid penalties and maintain a good standing in the state's business environment.

The U.S. Federal Form 1120S, used by S corporations for their annual tax returns, shares several similarities with the Wisconsin 5S form. Both forms require detailed financial information about the corporation's income, deductions, credits, and shareholders. They also include schedules for calculating taxes on net recognized built-in gains, reporting nonresident shareholders' income, and detailing other specific financial activities. Both forms serve a similar purpose for their respective tax authorities, asking for comprehensive financial data to accurately assess tax liability.

California's Form 100S, designed for S corporations filing within the state, mirrors the purpose and structure of Wisconsin's 5S form. Like the 5S, it includes sections on income, deductions, credits, and shareholder information. Both forms accommodate adjustments related to state-specific tax provisions and require detailed reporting of the corporation's financial activities throughout the fiscal year. These similarities stem from the need to align with federal S corporation reporting requirements while adapting to state-level tax codes.

New York's CT-3-S form for S corporation franchise tax returns shares several features with the Wisconsin 5S form. Both require detailed income reporting, calculation of applicable taxes, and allocation of income and deductions to shareholders. Additionally, they accommodate various tax credits unique to their state and require information on nonresident shareholders. Each form is tailored to capture the intricacies of the state's tax law as it applies to S corporations.

Pennsylvania's PA-20S/PA-65 form, which must be filed by S corporations operating within the state, has similarities with the Wisconsin 5S form in its structure and the information it collects. Both forms demand comprehensive financial details, including income, losses, deductions, and credits. They also have sections dedicated to nonresident shareholder income and specific state tax credits, demonstrating the blend of federal regulations with state-specific tax requirements.

Illinois' Form IL-1120-ST, designed for S corporation income and replacement tax return, closely resembles the Wisconsin 5S form in purpose and content. They both require detailed accounting of the corporation's income, deductions, and tax credits while also addressing the distribution of income to shareholders and the allocation of nonresident income. These forms reflect the adherence to both federal S corporation standards and the individual tax nuances of their respective states.

Michigan's Form 4891, the Corporate Income Tax Annual Return, though not exclusively for S corporations, contains sections that are similar to those found in Wisconsin's help taxpayers accurately report their corporate income and taxes due, taking into consideration various deductions and credits specific to their state regulations.

Ohio's IT 1140 form, intended for pass-through entities such as S corporations, shares objectives with the 5S form. Both forms manage the intricacies of allocating income to residents and nonresidents, showcasing a complex understanding of how state residency affects tax liability. Through detailed financial and shareholder information, they ensure equitable tax treatment for all shareholders.

Minnesota's M8 form for S corporations follows the same rationale as Wisconsin's 5S in capturing state-specific data on income, deductions, and tax credits alongside federal conformity issues. Both states' forms address the dual need to comply with federal S corporation rules while navigating the unique aspects of state tax codes. This duality ensures that S corporations are taxed fairly according to both federal and state guidelines.

Oregon's Form OR-20-S, for state S corporation tax returns, like the Wisconsin 5S form, demands comprehensive financial data, including income, deductions, and credits, tailored to the state's tax schemes. Both forms cater to the unique requirements of S corporations in their respective states, requiring detailed reporting to calculate tax liability accurately.

Colorado's Form 112, the S Corporation Income Tax Return, parallels the Wisconsin 5S form in structure and intent. Both forms facilitate the detailed reporting of income, deductions, and credits specific to S corporations, alongside shareholder distribution and nonresident income allocations. They exemplify the balancing act of adhering to federal guidelines while tailoring requirements to state tax laws.

When completing the Wisconsin 5S Form, it’s important to pay attention to details to ensure accuracy and compliance. Below is a list of dos and don’ts:

Following these guidelines will help ensure that your Wisconsin 5S Form is filled out accurately and processed efficiently.

Understanding the Form 5S for Wisconsin Tax-Option (S) Corporations involves navigating through some common misconceptions that often confuse taxpayers and advisors alike. Here’s a clarification of ten such misunderstandings:

Correctly understanding and addressing these misconceptions when completing the Wisconsin 5S form can help ensure compliance and potentially save tax dollars through proper application of credits, deductions, and tax reporting strategies.

Filling out the Wisconsin 5S form, designated for tax-option (S) corporations, requires attention to detail and understanding of the specificities involved to ensure accuracy and compliance with the state's tax regulations. Here are key takeaways to guide you through the process:

By following these guidelines and taking care to provide detailed and accurate information, tax-option (S) corporations can successfully navigate the completion and submission of the Wisconsin 5S form.

Apply for Food Stamps Wisconsin - By signing the application, employees disclose their health information under the assurance that it will be used solely for the purpose of obtaining group health insurance.

Wisconsin Inheritance Tax - Empowers taxation districts with a statutory method to handle uncollected personal property taxes efficiently and fairly.