Fill Your Wisconsin P 626 Form

Fill Your Wisconsin P 626 Form

The Wisconsin P 626 form serves as a critical tool in the fight against tax evasion and fraudulent financial activities within the state. Designed to collect detailed information on both individuals and businesses suspected of violating tax laws, it enables whistleblowers and others to report potential infractions directly to the Wisconsin Department of Revenue. The form is methodically divided into sections that solicit information about the alleged violator's identity, including personal details for individuals and key business data for companies. This not only promotes the thorough evaluation of each case but also assists in streamlining the investigation process. Furthermore, the form uniquely caters to a range of tax-related violations, from income and withholding tax to sales, use, and corporation franchise/income tax. It also seeks precise information on unreported income across multiple tax years, alleged overstated expenses, wrongly claimed dependents, and ineligibility for certain credits, among other violations. Importantly, the P 626 form includes provisions for the reporter to remain anonymous, reflecting a commitment to protecting informants while encouraging the reporting of tax evasion. With spaces dedicated to describing the nature of the violation, the availability of supporting records, and the option to be contacted for further inquiries, the form is both comprehensive and user-friendly. It serves as an instrumental resource for the Wisconsin Department of Revenue, enabling more effective tracking, investigation, and enforcement actions against tax evasion and fraud.

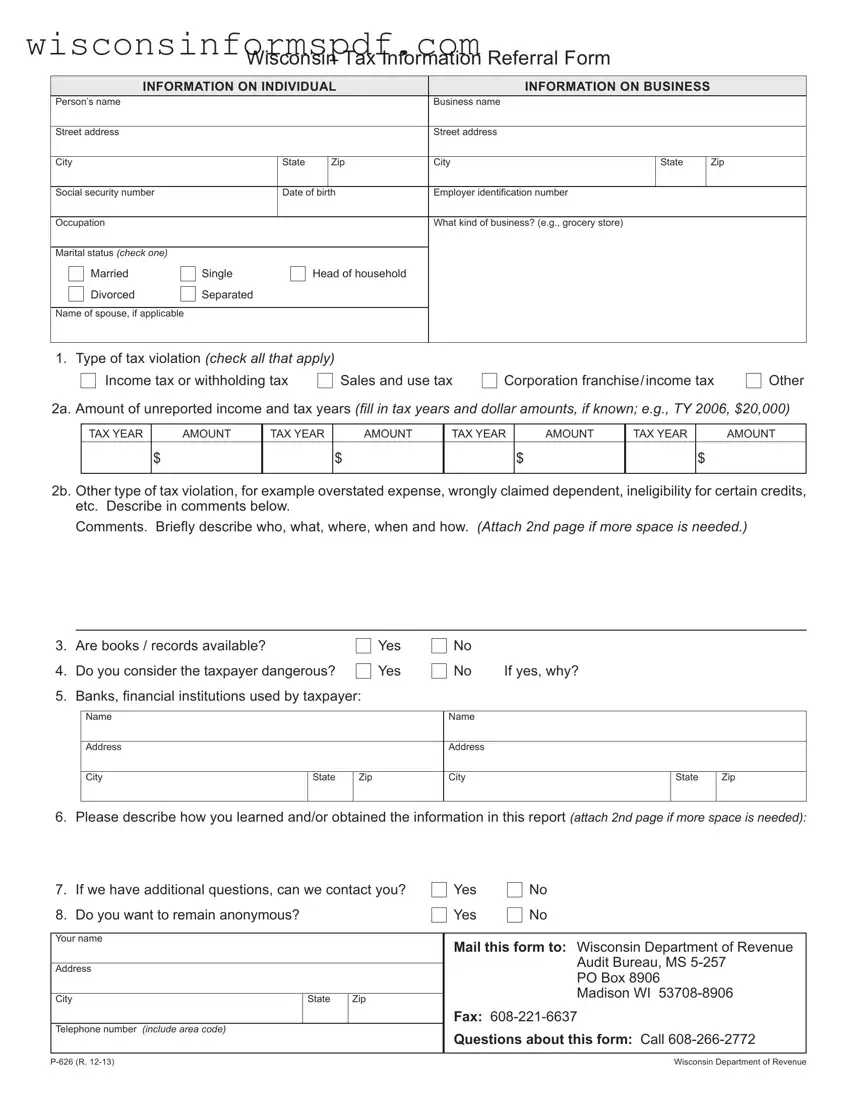

Wisconsin Tax Information Referral Form

INFORMATION ON INDIVIDUAL |

INFORMATION ON BUSINESS |

|

||||||

Person’s name |

|

|

|

|

Business name |

|

|

|

|

|

|

|

|

|

|

|

|

Street address |

|

|

|

|

Street address |

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

Zip |

City |

State |

|

Zip |

|

|

|

|

|

|

|

|

|

Social security number |

|

Date of birth |

Employer identification number |

|

|

|

||

|

|

|

|

|

|

|

|

|

Occupation |

|

|

|

|

What kind of business? (e.g., grocery store) |

|

|

|

|

|

|

|

|

|

|

|

|

Marital status (check one) |

|

|

|

|

|

|

|

|

Married |

Single |

Head of household |

|

|

|

|

||

Divorced |

Separated |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of spouse, if applicable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.Type of tax violation (check all that apply)

|

|

Income tax or withholding tax |

Sales and use tax |

Corporation franchise/income tax |

Other |

||||||

2a. |

Amount of unreported income and tax years (fill in tax years and dollar amounts, if known; e.g., TY 2006, $20,000) |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAX YEAR |

AMOUNT |

TAX YEAR |

AMOUNT |

TAX YEAR |

AMOUNT |

TAX YEAR |

|

AMOUNT |

|

|

|

|

$ |

|

$ |

|

|

$ |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

||

2b. |

Other type of tax violation, for example overstated expense, wrongly claimed dependent, ineligibility for certain credits, |

||||||||||

|

etc. Describe in comments below. |

|

|

|

|

|

|

|

|||

Comments. Briefly describe who, what, where, when and how. (Attach 2nd page if more space is needed.)

3. |

Are books / records available? |

Yes |

4. |

Do you consider the taxpayer dangerous? |

Yes |

5. |

Banks, financial institutions used by taxpayer: |

|

No |

|

No |

If yes, why? |

Name |

|

|

Name |

|

|

|

|

|

|

|

|

Address |

|

|

Address |

|

|

|

|

|

|

|

|

City |

State |

Zip |

City |

State |

Zip |

|

|

|

|

|

|

6. |

Please describe how you learned and/or obtained the information in this report (attach 2nd page if more space is needed): |

||||

7. |

If we have additional questions, can we contact you? |

Yes |

No |

||

8. |

Do you want to remain anonymous? |

Yes |

No |

||

|

|

|

|

|

|

Your name |

MAIL THIS FORM TO: Wisconsin Department of Revenue |

||||

|

|

|

|

||

|

|

|

|

|

Audit Bureau, MS |

Address |

|

||||

|

PO Box 8906 |

||||

|

|

|

|

|

|

|

|

|

|

|

Madison WI |

City |

|

State |

Zip |

|

|

|

|

|

|||

|

|

|

|

FAX: |

|

Telephone number (include area code) |

QUESTIONS ABOUT THIS FORM: Call |

||||

|

|

|

|

||

|

|

|

|

|

|

Wisconsin Department of Revenue |

2. Comments. Briefly describe who, what, where, when and how.

6. Please describe how you learned and/or obtained the information in this report:

- 2 - |

Wisconsin Department of Revenue |

| Fact | Description |

|---|---|

| Purpose | The Wisconsin P 626 form is used to report tax violations, such as unreported income, overstated expenses, or incorrect filings, to the Wisconsin Department of Revenue. |

| Components | This form includes sections for personal and business information, type of tax violation, amount of unreported income for specific tax years, details on any other types of violations, and information on the means by which the violation was discovered. |

| Governing Law | It is governed by the tax laws and regulations of the State of Wisconsin, specifically relating to the auditing and reporting of tax violations to the Wisconsin Department of Revenue. |

| Confidentiality | Filers have the option to remain anonymous when submitting information about tax violations, though they are given the option to provide contact information for follow-up questions. |

Filling out the Wisconsin P 626 form is a straightforward process, designed to help individuals report tax violations in a clear and organized manner. Whether you're reporting on an individual or a business, it's crucial to provide as much detail and accuracy as possible. The following steps are intended to guide you through completing the form, ensuring that all necessary information is accurately conveyed to the Wisconsin Department of Revenue.

Once submitted, your form will be processed by the Wisconsin Department of Revenue's Audit Bureau. If necessary, they may reach out to you for further clarification or additional information based on the contact preferences you indicated. It's important to note that the process and response time can vary based on the specifics of the report and the bureau's current workload.

What is the purpose of the Wisconsin P 626 form?

The Wisconsin P 626 form is intended for individuals to report suspected tax violations to the Wisconsin Department of Revenue. Its purpose is to gather information regarding potential income tax, withholding tax, sales and use tax, and corporation franchise/income tax violations by either an individual or a business. This form serves as a critical tool in identifying and investigating tax fraud and non-compliance within the state.

Who can fill out and submit this form?

Any individual who has information about a suspected tax violation by another individual or business in Wisconsin can fill out and submit the P 626 form. There's no restriction on who can report; concerned citizens, former employees, or even acquaintances with knowledge of tax irregularities are encouraged to report if they suspect tax evasion or fraud.

Can I remain anonymous when submitting the form?

Yes, individuals have the option to remain anonymous when submitting the Wisconsin P 626 form to report a suspected tax violation. The form includes a section where the reporter can specify if they wish to remain anonymous or if the Department of Revenue can contact them for further questions. This ensures that individuals can report issues without fear of retaliation.

What information needs to be included on the P 626 form?

The form requires detailed information about both the individual or business being reported and the nature of the suspected tax violation. This includes personal or business names, addresses, social security numbers or employer identification numbers, and specific details about the tax violation, such as the type of violation, unreported income, tax years affected, and any available documents or records. Additionally, the form asks how the reporter obtained the information and whether the taxpayer is considered dangerous.

How can the P 626 form be submitted?

The completed P 626 form can be mailed to the Wisconsin Department of Revenue's Audit Bureau at the provided PO Box address in Madison, WI. Alternatively, the form can also be faxed to the number listed on the form. This flexibility ensures that individuals can choose the submission method that is most convenient for them.

What happens after the form is submitted?

After the form is submitted, the Wisconsin Department of Revenue will review the information provided. If additional information is needed, the department may attempt to contact the reporting individual, assuming they have not chosen to remain anonymous. The department then conducts an investigation into the reported tax violation. It is important to note that due to confidentiality laws, the department may not be able to disclose any actions taken as a result of the report.

Is there a deadline for submitting the P 626 form?

There is no specific deadline for submitting the P 626 form. Reports of suspected tax violations can be made to the Wisconsin Department of Revenue at any time when an individual becomes aware of potentially fraudulent activities. Timely reporting, however, can aid in the more effective investigation and resolution of these issues.

Filling out the Wisconsin P 626 form, a Wisconsin Tax Information Referral Form, is a crucial step in reporting tax violations, but it's easy to fall into traps that might invalidate your efforts. Here are some common mistakes people make that you should avoid to ensure your report is comprehensive and accurately delivered to the Wisconsin Department of Revenue.

Avoiding these mistakes is essential for the effective reporting of tax violations in Wisconsin. Each detail you provide can significantly impact the course of an investigation, and ensuring that your form is filled out comprehensively and accurately can make a considerable difference. Remember, the objective of filling out the Wisconsin P 626 form is to help the Wisconsin Department of Revenue uphold tax laws and ensure fairness for all taxpayers.

When dealing with tax compliance, specific scenarios or investigative needs may require additional documents beyond the Wisconsin P 626 form. This referral form plays a crucial role in flagging potential tax violations. However, in the pursuit of thoroughness and legal accuracy, various supplementary forms and documents are often utilized in conjunction with the P 626 to provide a fuller picture of an individual’s or business's tax situation. Below is a list of documents that frequently accompany the Wisconsin P 626 form, each serving its unique purpose in the tax enforcement and compliance process.

These documents collectively aid regulatory bodies and investigators in creating a thorough understanding of a taxpayer’s situation. Whether reviewing income sources, verifying tax payments, or investigating potential fraud, the combined use of these forms creates a scaffold that supports the integrity of the tax system. Thus, while the Wisconsin P 626 form initiates the process, the ensuing investigation relies on a wider array of documents to ensure fairness and accuracy in tax compliance and enforcement.

The Federal Form 3949-A, "Information Referral," used by the IRS for reporting suspected tax fraud, is quite similar to the Wisconsin P 626 form. Both documents collect detailed personal and business information, including names, addresses, and social security or employer identification numbers. They also ask for specifics about the alleged tax violation, such as the type of tax issue (income, sales, etc.), and provide space for the claimant to describe the violation in detail, like unreported income or incorrect deductions. The forms are designed to streamline the process of reporting tax violations to the respective tax authority, helping in the investigation of tax evasion or fraud.

The Form 211, "Award for Original Information," also parallels the Wisconsin P 626 form in that it's used by the IRS Whistleblower Office to report tax evasion. Although its primary purpose is to apply for a financial award, it similarly requests detailed tax violation information, including types of taxes involved, and amounts of unreported income or overstated expenses. Where the P 626 form is specifically for reporting potential tax violations without the expectation of reward, both forms play crucial roles in uncovering tax malfeasance, highlighting the whistleblower's role in tax law enforcement.

Sarbanes-Oxley Act (SOX) whistleblower forms, used for reporting corporate fraud, echo aspects of the Wisconsin P 626 form through their focus on collecting detailed reports of alleged wrongdoing. While SOX forms are broader, covering various types of corporate misconduct beyond tax violations, they share the core function of documenting specific allegations. They request descriptions of the misconduct, including the "who, what, where, when, and how," similar to the detailed descriptions and comments section in the P 626 form. Both empower individuals to report misconduct, aiming to bring about corporate or fiscal accountability.

The Financial Crimes Enforcement Network (FinCEN) Suspicious Activity Reports (SARs) bear resemblance to the P 626 form in their objective to combat fraud, money laundering, and other financial crimes. Like the P 626, SARs require detailed information about the parties involved, including personal and business identifiers, and the nature of the suspicious activity. Though SARs are more focused on financial transactions and the banking sector, both forms are vital tools for federal and state agencies to investigate and penalize unlawful financial activities.

The Department of Labor's (DOL) WH-380, used for reporting violations of the Fair Labor Standards Act (FLSA), while differing in focus—employment law versus tax law—utilizes a similar reporting mechanism to the P 626. It collects detailed information about the employer and employee, and specifics about the alleged violation. Both forms serve as formal complaints that trigger investigations by the respective authority, ensuring adherence to state or federal laws and protecting individuals' rights within their employment or tax obligations.

The HUD Housing Discrimination Complaint Form, like the Wisconsin P 626 form, is designed for reporting specific allegations—this time of housing discrimination rather than tax fraud. It collects detailed information about the complainant, the party alleged to have committed the discrimination, and a description of the alleged discriminatory act. Although addressing different areas of law, both forms share the aim of enforcing legal standards through the reporting of violations, allowing authorities to investigate and address the reported misconduct.

The SEC Form TCR (Tip, Complaint or Referral), utilized by the Securities and Exchange Commission, is another document structured similarly to the Wisconsin P 626 form. It is intended for reporting violations of securities laws, with sections for detailed information about the individuals or entities involved, explanation of the suspected misconduct, and any additional documents that can substantiate the claim. Although focused on securities rather than tax law, the SEC Form TCR and the P 626 form alike encourage individuals to report wrongdoing, facilitating regulatory oversight and enforcement actions.

When filling out the Wisconsin P 626 form, attention to detail is crucial. Below are key dos and don'ts to keep in mind to ensure that the information provided is accurate and well-presented.

Understanding the Wisconsin P 626 form can sometimes be challenging, leading to a number of misconceptions. It's important to address these inaccuracies to ensure clarity and correctness when dealing with tax information referral forms. Below are eight common misconceptions and the truths behind them.

It's crucial for individuals and businesses to understand these aspects of the Wisconsin P 626 form to ensure its proper and effective use. Misunderstandings can lead to hesitancy or improper reporting, which ultimately hinders the effort to maintain tax compliance and fairness. Whether choosing to report anonymously or not, the main objective is to supply the Department of Revenue with information that could indicate tax violations, enabling appropriate actions to be taken.

Filling out the Wisconsin P 626 form is an important step in reporting tax violations. It is designed to make the process straightforward for individuals who wish to report discrepancies. Below are key takeaways to ensure you complete and submit this form correctly.

Mailing and fax information is clearly provided for the submission of the form, ensuring that individuals know how to submit their report to the Wisconsin Department of Revenue Audit Bureau. Additionally, for further questions, a telephone number is readily available, making it easier for individuals to seek clarification or assistance.

When Must a Crash Be Reported to a Law Enforcement Agency? - A user-friendly guide and form for Wisconsin drivers to help in reporting traffic accidents, underlining damages and injuries.

Wisconsin F 62019 - The F 62019 form is a proactive measure for drivers to protect themselves legally and financially in the aftermath of a vehicle accident.

Wisconsin Permit - Submission of the MV3001 form is also a declaration of residency in Wisconsin, as outlined in the document.