Fill Your Wisconsin Pc 200 Form

Fill Your Wisconsin Pc 200 Form

In Wisconsin, managing uncollected personal property taxes presents a unique challenge, especially when entities that owe these taxes cease operations, declare bankruptcy, or when the taxable personal property is removed from the tax roll. The Wisconsin PC 200 form, an essential tool in this process, facilitates the chargeback of uncollected net personal property taxes to various taxing jurisdictions within a taxation district, excluding the state itself. This procedure, detailed in Section 74.42(1), Wis. Stats., allows taxation district treasurers to redistribute the burden of uncollected taxes proportionately among local taxing bodies, such as counties, school districts, and technical colleges. The form specifies a timeframe—no earlier than February 2 and no later than April 1—for taxation district treasurers to act. It requires detailed information including the personal property account number, property owner's name, and the net amount of uncollected taxes. Moreover, it outlines a precise methodology for calculating each jurisdiction’s share of the tax shortfall and subsequently how to charge it back. This ensures that even when taxes go unpaid, the financial responsibility is equitably shared, preventing undue strain on any one part of the local government. With explicit instructions and an example provided, the PC 200 form is designed to streamline what could otherwise be a complex and contentious endeavor, safeguarding local finances against the unpredictable fiscal impacts of uncollected taxes.

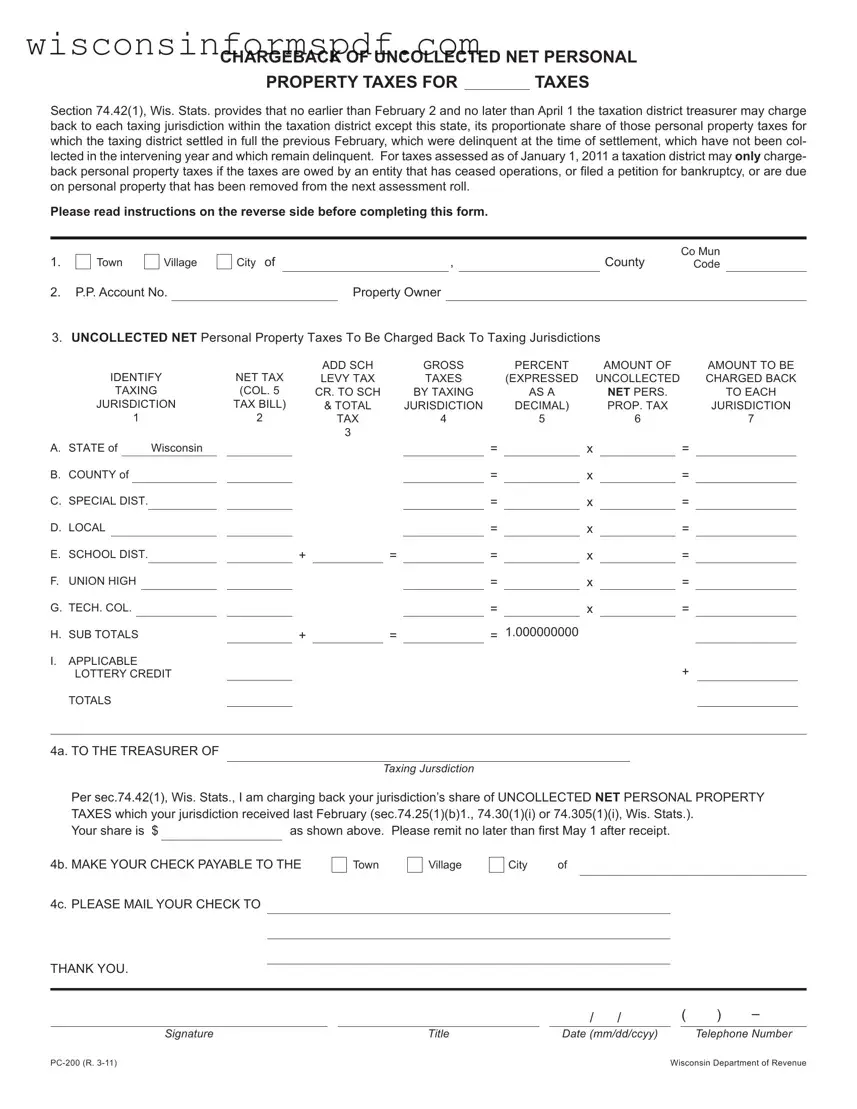

CHARGEBACK OF UNCOLLECTED NET PERSONAL

PROPERTY TAXES FOR |

|

TAXES |

Section 74.42(1), Wis. Stats. provides that no earlier than February 2 and no later than April 1 the taxation district treasurer may charge back to each taxing jurisdiction within the taxation district except this state, its proportionate share of those personal property taxes for which the taxing district settled in full the previous February, which were delinquent at the time of settlement, which have not been col- lected in the intervening year and which remain delinquent. For taxes assessed as of January 1, 2011 a taxation district may only charge- back personal property taxes if the taxes are owed by an entity that has ceased operations, or iled a petition for bankruptcy, or are due on personal property that has been removed from the next assessment roll.

Please read instructions on the reverse side before completing this form.

1. |

Town |

Village |

2.P.P. Account No.

City of |

|

, |

|

County |

Co Mun |

||

|

Code |

|

|||||

|

Property Owner |

|

|

|

|

|

|

3. UNCOLLECTED NET Personal Property Taxes To Be Charged Back To Taxing Jurisdictions

IDENTIFY |

NET TAX |

|

ADD SCH |

|

GROSS |

|

PERCENT |

|

AMOUNT OF |

|

|

AMOUNT TO BE |

||||||||||

|

LEVY TAX |

|

TAXES |

|

(EXPRESSED |

UNCOLLECTED |

|

|

CHARGED BACK |

|||||||||||||

|

TAXING |

(COL. 5 |

|

CR. TO SCH |

|

BY TAXING |

|

AS A |

|

NET PERS. |

|

|

TO EACH |

|||||||||

JURISDICTION |

TAX BILL) |

|

& TOTAL |

|

JURISDICTION |

|

DECIMAL) |

|

PROP. TAX |

|

|

JURISDICTION |

||||||||||

1 |

|

|

|

|

2 |

|

TAX |

4 |

5 |

6 |

|

7 |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

A. STATE of |

|

Wisconsin |

|

|

|

|

|

|

= |

|

x |

|

|

= |

|

|

|

|||||

B. COUNTY of |

|

|

|

|

|

|

|

|

= |

|

x |

|

|

= |

|

|

|

|||||

C. SPECIAL DIST. |

|

|

|

|

|

|

|

= |

|

x |

= |

|

|

|

||||||||

D. LOCAL |

|

|

|

|

|

|

|

|

|

= |

|

x |

|

|

= |

|

|

|

||||

E. SCHOOL DIST. |

|

|

|

+ |

|

= |

|

= |

|

x |

= |

|

|

|

||||||||

F. UNION HIGH |

|

|

|

|

|

|

|

|

|

= |

|

x |

|

|

= |

|

|

|

||||

G. TECH. COL. |

|

|

|

|

|

|

|

|

= |

|

x |

|

|

= |

|

|

|

|||||

H. SUB TOTALS |

|

|

|

+ |

|

= |

|

= 1.000000000 |

|

|

|

|

|

|

|

|||||||

I. APPLICABLE |

|

|

|

|

|

|

|

|

|

|

|

|

+ |

|

|

|

||||||

LOTTERY CREDIT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

TOTALS

4a. TO THE TREASURER OF

Taxing Jursdiction

Per sec.74.42(1), Wis. Stats., I am charging back your jurisdiction’s share of UNCOLLECTED NET PERSONAL PROPERTY TAXES which your jurisdiction received last February (sec.74.25(1)(b)1., 74.30(1)(i) or 74.305(1)(i), Wis. Stats.).

Your share is $ |

|

as shown above. Please remit no later than irst May 1 after receipt. |

4b. MAKE YOUR CHECK PAYABLE TO THE

Town

Village

City of

4c. PLEASE MAIL YOUR CHECK TO

THANK YOU.

|

|

|

/ |

/ |

( |

) |

– |

||

Signature |

|

Title |

|

Date (mm/dd/ccyy) |

|

|

Telephone Number |

||

Wisconsin Department of Revenue |

INSTRUCTIONS

COMPLETE ONE FORM FOR EACH UNCOLLECTED PERSONAL PROPERTY TAX BILL WHICH QUALIFIES UNDER SEC. 74.42(1), WIS. STATS. AS A CHARGEBACK.

Heading: Enter applicable year in the space provided in the form title.

Line 1: Check the applicable box, enter the name of your taxation district, county and your

Line 2: Enter the personal property account number and the name of the property owner.

Lines

EXAMPLE

In this example the taxation district has been unable to collect $4,858.12 of NET tax from a taxpayer that has ceased operations.

IDENTIFY

TAXING

JURISDICTION

1

A. |

STATE |

|

Wisconsin |

||||

B. |

COUNTY |

|

|

Dane |

|||

C. |

SPECIAL DIST. Rd. Lake |

||||||

D. |

LOCAL |

|

|

T. Badger |

|||

E. |

SCHOOL DIST. Lincoln |

||||||

F. |

UNION HIGH |

|

|

||||

G. |

TECH. COL. |

|

|

MATC |

|||

H.SUB TOTALS

I.APPLICABLE LOTTERY CREDIT

TOTALS

NET TAX |

|

ADD SCH |

|

GROSS TAXES |

|

|

|

|

||||||||

|

LEVY TAX |

|

|

|

PERCENT |

|||||||||||

|

|

|

(COL. 5 |

CR. TO SCH |

|

|

|

BY TAXING |

|

(EXPRESSED AS |

||||||

TAX BILL) |

& TOTAL TAX |

|

JURISDICTION1,2 |

|

|

A DECIMAL) |

||||||||||

2 |

|

3 |

|

|

4 |

|

|

5 |

|

|||||||

|

43.65 |

|

|

|

|

|

|

43.65 |

|

= |

0.008222879 |

|

||||

1,025.14 |

|

|

|

|

|

|

1,025.14 |

|

= |

|

0.193118025 |

|

||||

|

98.58 |

|

|

|

|

|

|

98.58 |

|

= |

|

0.018570707 |

|

|||

|

515.95 |

|

|

|

|

|

|

515.95 |

|

= |

|

0.097195744 |

|

|||

2,874.73 |

+ |

450.24 |

|

= |

3,324.97 |

|

= |

0.626364828 |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

= |

|

|

|

|

300.07 |

|

|

|

|

|

|

300.07 |

|

= |

|

0.056527817 |

|

|||

4,858.12 |

+ |

450.24 |

|

= |

|

5,308.36 |

|

= |

1.000000000 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

4,774.14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

CALCULATION PROCEDURES

AMOUNT OF QUALIFYING |

|

AMOUNT TO BE |

|||||||

|

CHARGED BACK |

||||||||

|

UNCOLLECTED NET |

|

|

|

TO EACH |

||||

|

PERS. PROP. TAX |

|

|

|

JURISDICTION2,4 |

||||

|

6 |

|

|

|

7 |

||||

x |

|

|

4,774.14 |

|

= |

|

39.26 |

||

4,774.14 |

|

||||||||

|

|

921.97 |

|||||||

x |

|

|

= |

|

|||||

x |

4,774.14 |

|

= |

|

88.66 |

||||

x |

|

4,774.14 |

|

= |

|

|

464.03 |

||

x |

|

4,774.14 |

|

= |

|

|

2990.35 |

||

x |

|

|

|

|

|

= |

|

0.00 |

|

x |

|

4,774.14 |

|

= |

|

|

269.87 |

||

|

|

4,774.14 |

|||||||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

+ |

|

83.98 |

|

|

|

|

|

|

|

|

|

4,858.12 |

|

1.Enter Net Taxes from Column 5 of tax bill in Column 2 of this form.

2.Add school levy tax credit to school tax and total tax (Col. 3) to get actual gross tax (Col. 4).

3.Calculate the percentage (to 9 decimal points) that each taxing jurisdiction’s share of tax is to the total tax. (Divide the gross

tax for each taxing jurisdiction by the total gross tax. For example, 43.65 |

÷ 5,308.36 = .008222879). Enter your results in Column 5. |

4.Enter the amount of qualifying UNCOLLECTED NET personal property tax in Column 6.

5.Multiply the total amount of qualifying UNCOLLECTED NET personal property tax by the percentage you calculated. (Multiply Column 6 by Column 5.) If personal property such as a mobile home, qualiies for the lottery credit and it was claimed, net tax means after lottery credit. Enter the lottery credit amount on line I and subtract from line H column 2.

6.Enter the amounts you have calculated on the appropriate lines in Column 7.

Note: 1. Gross taxes are before school levy tax, and lottery and gaming credits have been subtracted.

2.Your tax district’s share. May be budgeted for in your next budget.

3.If the municipality has a TIF district(s), use the APPORTIONED levies from your Statement of Taxes to calculate the amount to be charged back. The entire tax increment must be included with the local tax. Contact us for special instructions if the municipality has a TIF district and multiple school districts.

4.The state’s proportionate share shall be charged back to the county.

Line 4a. A copy of this form must be sent to the treasurer of each taxing jurisdiction having an entry greater than zero in column 7, except for local and state (see example notes). Enter the name of the applicable taxing jurisdiction in the space provided and enter the amount you are charging back to that taxing jurisdiction.

Line 4b. Enter the name the taxing jurisdiction should make its check payable to.

Line 4c. Enter the complete address of where the taxing jurisdiction should mail the check.

Enter your title, the date, and telephone number in the spaces provided and sign the form before mailing. Retain original worksheet and send a copy to the tax district clerk; and mail a copy to each affected taxing jurisdictions.

Contact the Department of Revenue, Local Government Services Section at lgs@revenue.wi.gov, or (608)

| Fact Name | Description |

|---|---|

| Governing Law | Section 74.42(1), Wis. Stats., authorizes the process for the chargeback of uncollected net personal property taxes within certain timelines. |

| Timeframe for Action | The taxation district treasurer may execute the chargeback process no earlier than February 2 and no later than April 1 following the year of delinquency. |

| Eligibility Criteria for Chargeback | Chargeback applies only to personal property taxes remaining delinquent from the previous February settlement, specifically if the entity has ceased operations, filed for bankruptcy, or the property has been removed from the assessment roll. |

| Completion and Submission | The PC-200 form requires detailed information about the uncollected taxes and the proportionate share owed by each taxing jurisdiction. It must be completed and sent to the relevant jurisdictions along with a request for payment by May 1. |

Filling out the Wisconsin Pc 200 form, a process that entails providing accurate information about uncollected net personal property taxes, must be carried out meticulously to ensure each taxing jurisdiction within the taxation district is properly charged back. This form plays a critical role in the annual financial adjustments of taxation districts, particularly when previous attempts to collect owed taxes have been unsuccessful. The steps below guide you through the completion of this form, ensuring clarity and compliance with state regulations. To fill this form out correctly, one needs to closely follow the specified instructions and understand the allocation of uncollected taxes across different jurisdictions.

Upon completion, this meticulous process ensures fair allocation of charges for uncollected taxes, improving financial outcomes for all involved jurisdictions. Should questions arise, or if the complexities of your district's situation require it, the provided contact details for the Department of Revenue are invaluable resources for additional support.

What is the Wisconsin PC 200 form?

The Wisconsin PC 200 form, also known as the "Chargeback of Uncollected Net Personal Property Taxes" form, is a financial document used by taxation district treasurers in Wisconsin. It allows them to charge back to each taxing jurisdiction within the district (except the state) their proportionate share of personal property taxes that were delinquent at the time of settlement, have not been collected in the past year, and remain delinquent. This process is detailed under Section 74.42(1) of the Wisconsin Statutes.

When should the PC 200 form be completed and submitted?

The form must be completed and sent no earlier than February 2 and no later than April 1 following the year in which the personal property taxes remain uncollected. This deadline allows taxation districts to reconcile uncollected taxes in a timely manner, ensuring that affected taxing jurisdictions are informed and can adjust their financial planning accordingly.

Who needs to be notified with the completion of the PC 200 form?

Upon completion, a copy of the PC 200 form needs to be sent to the treasurer of each taxing jurisdiction that has an entry greater than zero in the calculated chargeback amounts, with the exception of local and state jurisdictions. Additionally, the tax district clerk and each affected taxing jurisdiction should receive a copy of this form. This ensures that all parties involved are aware of the uncollected amounts and the impact on their financial planning.

How is the amount to be charged back to each jurisdiction calculated?

The calculation involves determining each jurisdiction's proportionate share of the uncollected net personal property taxes by applying the percentage of the jurisdiction's share of the total taxes (to nine decimal points) to the amount of qualifying uncollected net personal property tax. This complex calculation considers the net taxes from the tax bill, adding any applicable school levy tax credit to the school tax and the total tax to get the actual gross tax. From this, each jurisdiction's percentage share is applied to find the amount to be charged back.

Are there any special circumstances where the PC 200 form cannot be used?

Yes, for taxes assessed as of January 1, 2011, a taxation district may only chargeback personal property taxes if those taxes are owed by an entity that has ceased operations, filed a petition for bankruptcy, or are due on personal property that has been removed from the next assessment roll. This limitation aims to ensure that chargebacks are pursued only in situations where collection efforts are unlikely to be successful due to the debtor's circumstances.

What should be done after completing the form?

After completing the form, the taxation district treasurer should mail it to the treasurer of each affected taxing jurisdiction, along with making the necessary financial adjustments in their records. Retaining the original worksheet and ensuring that a copy is sent to both the tax district clerk and each affected taxing jurisdiction is crucial for maintaining transparency and proper documentation of the chargeback process.

Where can I get assistance or more information on completing the PC 200 form?

For assistance or further information on completing the PC 200 form, taxation district treasurers and other officials can contact the Wisconsin Department of Revenue's Local Government Services Section via email at lgs@revenue.wi.gov, or by calling (608) 261-5341. They provide guidance and support to ensure the form is completed accurately and in compliance with Wisconsin's statutory requirements.

Filling out the Wisconsin PC-200 form, which is specifically designed for the chargeback of uncollected net personal property taxes, can be a complex task. This complexity often leads to mistakes that can have significant ramifications for the taxation district and the entities involved. By being aware of common pitfalls, individuals can ensure a smoother process and avoid potential issues.

One key area where mistakes commonly occur is in the calculation and allocation of amounts to be charged back to each taxing jurisdiction. This involves a series of detailed steps that must be followed with precision:

To ensure accuracy, it's pivotal to meticulously follow the instructions provided on the form, including those related to special tax considerations like TIF districts or lottery and gaming credits. Careful attention to detail in calculating the share of taxes using the provided example as a guide can help avoid common errors. Moreover, double-checking entries against tax bills and ensuring that all necessary jurisdictional information is correctly filled out will assist in mitigating potential issues.

Furthermore, communication with the Department of Revenue, Local Government Services Section for assistance, as suggested at the form’s conclusion, is a critical step for clarifying any uncertainties and ensuring compliance with the statutory requirements. By avoiding these common mistakes and seeking guidance when necessary, individuals can contribute to the efficient and accurate processing of the form.

When dealing with the Wisconsin Pc 200 form, which focuses on the chargeback of uncollected net personal property taxes, understanding additional forms and documents that might be used alongside it is crucial for thorough processing and compliance. These documents each have a specific role in ensuring the accurate and legal handling of taxes and their associated adjustments within the state of Wisconsin.

Collectively, these forms contribute to a comprehensive understanding and management of taxes within Wisconsin, providing the necessary details to ensure compliance and accuracy in financial and tax reporting. Entities dealing with personal property taxes must be aware of these documents to manage their tax obligations effectively. Coordination between these various forms ensures that the financial health and legal standing of businesses and individuals relative to personal property taxes are maintained appropriately.

The Wisconsin PC-200 form bears similarity to the "Declaration of Personal Property" form used in various states. This form also deals with the valuation and reporting of personal property for tax purposes. Both forms require property owners to provide detailed information about the personal property subject to tax within a jurisdiction. The key similarity lies in their focus on ensuring accurate tax assessment of personal property, thus requiring detailed breakdowns of the property values. However, the Wisconsin PC-200 form specifically addresses the chargeback process for uncollected taxes, whereas the "Declaration of Personal Property" form primarily serves as a means to declare property value initially.

Another comparable document is the "Request for Taxpayer Identification Number and Certification" (Form W-9) in the context of providing essential taxpayer information. Like the PC-200 form, the W-9 is a critical tax document used within the United States to correctly identify and tax entities. Both forms are integral to the tax collection and compliance process, ensuring that taxing authorities have accurate information. While the W-9 form collects taxpayer identification information to prevent tax evasion, the PC-200 form is used to manage the specifics of tax owed on personal property and its subsequent chargeback, demonstrating their roles in broader tax administration efforts.

The "Real Estate Tax Statement" form, issued by county treasurers, also shares parallels with the Wisconsin PC-200 form. This form outlines the amount of real estate taxes due on a property, similar to how the PC-200 lists uncollected personal property taxes. Though one document focuses on real estate and the other on personal property, both serve the crucial function of informing taxpayers and jurisdictions about tax liabilities. Additionally, both forms contribute to the process of tax reconciliation and collection within their respective scopes, highlighting their importance in local government finance.

Lastly, the "Bankruptcy Proof of Claim" form is similar to the Wisconsin PC-200 in the context of addressing unpaid liabilities. This form is used in bankruptcy proceedings to identify creditors and the amount owed by the bankrupt party. The resemblance lies in their function of dealing with unpaid debts - for the "Bankruptcy Proof of Claim," it pertains to all manners of debt in the context of bankruptcy, while the PC-200 form specifically targets uncollected personal property taxes. Each document plays a crucial role in the respective legal and tax collection frameworks, ensuring that liabilities are accounted for and properly managed.

When completing the Wisconsin PC 200 Form, which is designed for the chargeback of uncollected net personal property taxes, it's important to follow explicit guidelines to ensure the process is executed accurately and efficiently. Here’s a comprehensive list of dos and don'ts:

Do:

Don’t:

Following these guidelines will help ensure that the process of charging back uncollected net personal property taxes is handled properly, maintaining accuracy and compliance with Wisconsin state statutes.

There are several misunderstandings about the Wisconsin Pc 200 form which need to be clarified:

One common misconception is that the Pc 200 form applies to all types of property taxes. However, it specifically pertains to the chargeback of uncollected net personal property taxes. This means it is only relevant for personal property taxes that remain unpaid, not real estate taxes or other types of taxes.

Another misunderstanding is that taxes can be charged back at any time. The form clearly states that the chargeback can only occur no earlier than February 2 and no later than April 1, following the year the taxes were settled but remained delinquent.

Some may wrongly believe that any delinquent personal property tax can be charged back using this form. In reality, chargebacks can only apply to taxes owed by entities that have ceased operations, filed for bankruptcy, or taxes on personal property removed from the next assessment roll as highlighted for taxes assessed from January 1, 2011, onwards.

There is also a misconception regarding the recipients of the chargeback notice. It must be sent to each taxing jurisdiction within the district excluding the state, for their proportionate share of the uncollected personal property taxes. This requirement ensures that the correct jurisdictions are informed and responsible for their share of the uncollected taxes.

Understanding these key aspects of the Wisconsin Pc 200 form helps in accurate completion and compliance with the specified requirements, ensuring proper handling of uncollected personal property taxes.

Understanding the Wisconsin Pc 200 form is crucial for efficiently managing uncollected personal property taxes in a timely and legally compliant manner. Here are seven key takeaways to ensure the process is handled effectively:

These guidelines ensure that the process of reclaiming uncollected personal property taxes is handled effectively, providing clarity and structure to what can be a complex process. For further assistance, individuals are encouraged to contact the Department of Revenue's Local Government Services Section.

What Is a Rent Certificate - By requiring specific details about the rental period and expenses, the form minimizes ambiguity and maximizes accuracy in homestead credit applications.

Motion to Modify Placement Wisconsin Form - This official form aids Wisconsin parents and guardians in the process of reevaluating court orders related to family maintenance, aligning them with current needs.

When Must a Crash Be Reported to a Law Enforcement Agency? - Comprehensive accident report form for Wisconsin drivers, detailing criteria for when self-reporting is required after a traffic incident.