Fill Your Wisconsin Tax Exempt Form

Fill Your Wisconsin Tax Exempt Form

The Wisconsin Tax Exempt form serves as a crucial document for entities looking to claim exemption from state and local taxes in Wisconsin on eligible purchases, leases, or rentals. By completing this form, purchasers assert that their acquisition of tangible personal property or taxable services is not subject to Wisconsin state, county, baseball or football stadium, local exposition, and premier resort sales or use tax. These exemptions are specified for items used in certain business operations, such as farming, which includes a wide range of activities and tangible personal property like tractors, all-terrain vehicles, farm machines, and other related items. The form requires detailed information about the purchaser, such as the business name, phone number, and address, alongside a description of the property or services bought. It also mandates the seller’s details and the intended exempt use of the purchased items, necessitating accuracy in completion to ensure compliance. The certificate differentiates between single purchases and continuous engagements, allowing for specificity in how exemptions are applied. Importantly, it underscores the purchaser’s responsibility to remit use tax on the purchase price in instances where items are not used in an exempt manner, highlighting the legal obligations and potential consequences for non-compliance.

Instructions

Save

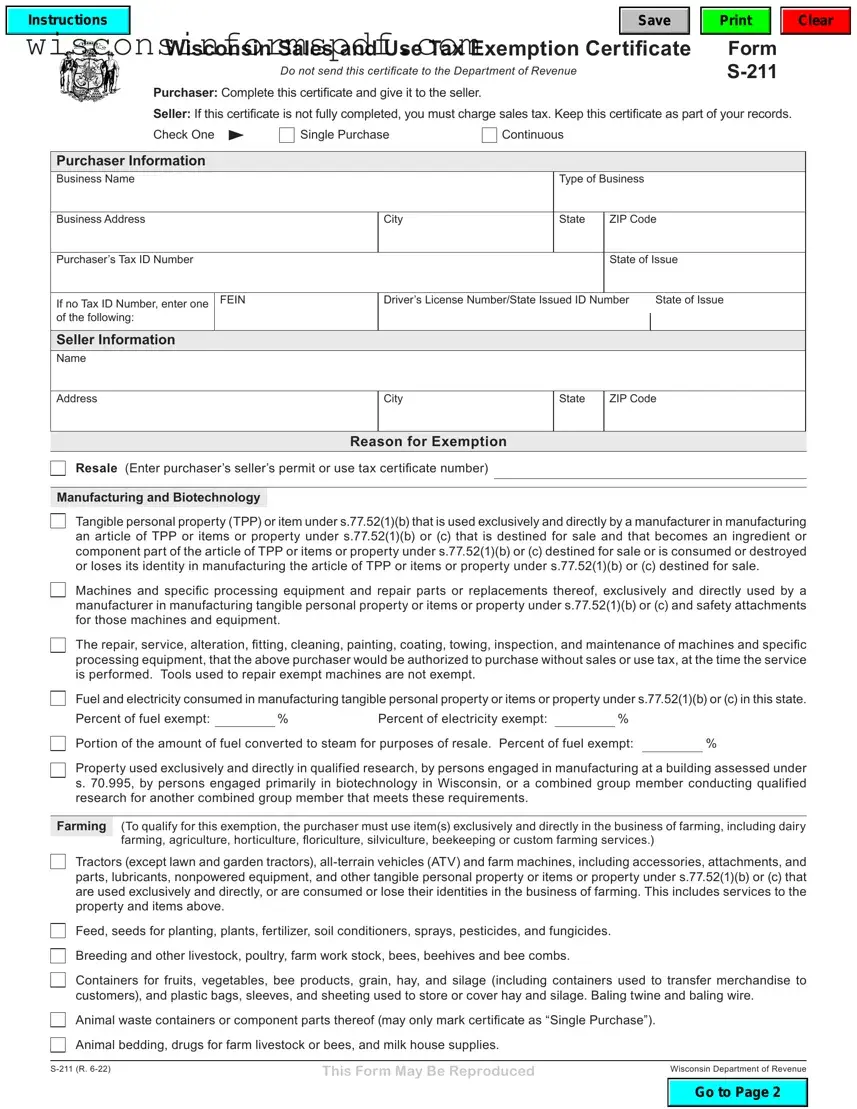

Wisconsin Sales and Use Tax Exemption Certificate

Do not send this certificate to the Department of Revenue

Purchaser: Complete this certificate and give it to the seller.

Form

Clear

Seller: If this certificate is not fully completed, you must charge sales tax. Keep this certificate as part of your records.

Check One |

Single Purchase |

Continuous |

|

|

||||

|

|

|

|

|

|

|

|

|

Purchaser Information |

|

|

|

|

|

|

|

|

Business Name |

|

|

|

|

Type of Business |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Address |

|

City |

|

|

State |

ZIP Code |

||

|

|

|

|

|

|

|

|

|

Purchaser’s Tax ID Number |

|

|

|

|

|

State of Issue |

||

|

|

|

|

|

|

|

||

If no Tax ID Number, enter one |

FEIN |

|

Driver’s License Number/State Issued ID Number |

State of Issue |

||||

of the following: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

Seller Information |

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

Address

City

State

ZIP Code

Reason for Exemption

Resale (Enter purchaser’s seller’s permit or use tax certificate number)

Manufacturing and Biotechnology

Tangible personal property (TPP) or item under s.77.52(1)(b) that is used exclusively and directly by a manufacturer in manufacturing an article of TPP or items or property under s.77.52(1)(b) or (c) that is destined for sale and that becomes an ingredient or component part of the article of TPP or items or property under s.77.52(1)(b) or (c) destined for sale or is consumed or destroyed or loses its identity in manufacturing the article of TPP or items or property under s.77.52(1)(b) or (c) destined for sale.

Machines and specific processing equipment and repair parts or replacements thereof, exclusively and directly used by a manufacturer in manufacturing tangible personal property or items or property under s.77.52(1)(b) or (c) and safety attachments for those machines and equipment.

The repair, service, alteration, fitting, cleaning, painting, coating, towing, inspection, and maintenance of machines and specific processing equipment, that the above purchaser would be authorized to purchase without sales or use tax, at the time the service is performed. Tools used to repair exempt machines are not exempt.

Fuel and electricity consumed in manufacturing tangible personal property or items or property under s.77.52(1)(b) or (c) in this state.

Percent of fuel exempt: |

|

% |

Percent of electricity exempt: |

|

% |

|

|

Portion of the amount of fuel converted to steam for purposes of resale. Percent of fuel exempt: |

|

% |

|||||

Property used exclusively and directly in qualified research, by persons engaged in manufacturing at a building assessed under s. 70.995, by persons engaged primarily in biotechnology in Wisconsin, or a combined group member conducting qualified research for another combined group member that meets these requirements.

Farming (To qualify for this exemption, the purchaser must use item(s) exclusively and directly in the business of farming, including dairy farming, agriculture, horticulture, floriculture, silviculture, beekeeping or custom farming services.)

Tractors (except lawn and garden tractors),

Feed, seeds for planting, plants, fertilizer, soil conditioners, sprays, pesticides, and fungicides. Breeding and other livestock, poultry, farm work stock, bees, beehives and bee combs.

Containers for fruits, vegetables, bee products, grain, hay, and silage (including containers used to transfer merchandise to customers), and plastic bags, sleeves, and sheeting used to store or cover hay and silage. Baling twine and baling wire.

Animal waste containers or component parts thereof (may only mark certificate as “Single Purchase”). Animal bedding, drugs for farm livestock or bees, and milk house supplies.

This Form May Be Reproduced |

Wisconsin Department of Revenue |

|

|

|

Go to Page 2 |

|

|

|

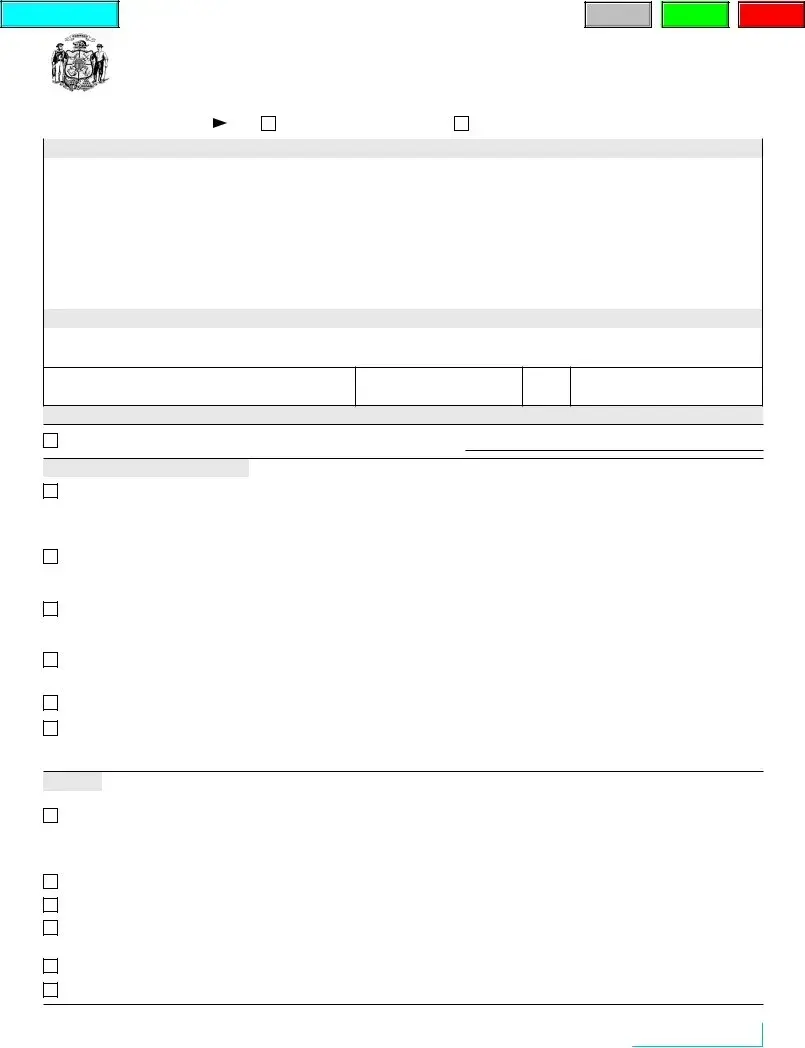

Governmental Units and Other Exempt Entities |

|

Enter CES No., if applicable |

|

|

The United States and its unincorporated agencies and instrumentalities. Any federally recognized American Indian tribe or band in this state.

Wisconsin state and local governmental units, including the State of Wisconsin or any agency thereof, Wisconsin counties, cities, villages, or towns, and Wisconsin public schools, school districts, universities, or technical college districts.

Organizations meeting the requirements of section 501(c)(3) of the Internal Revenue Code. Wisconsin organizations must enter a CES number above.

Other

Containers and other packaging, packing, and shipping materials, used to transfer merchandise to customers of the purchaser. Trailers and accessories, attachments, parts, supplies, materials, and service for motor trucks, tractors, and trailers which are

used exclusively in common or contract carriage under LC, IC, or MC No. (if applicable) |

|

. |

Machines and specific processing equipment used exclusively and directly in a fertilizer blending, feed milling, or grain drying operation, including repair parts, replacements, and safety attachments.

Building materials acquired solely for and used solely in the construction or repair of holding structures used for weighing and dropping feed or fertilizer ingredients into a mixer or for storage of such grain, if such structures are used in a fertilizer blending, feed milling, or grain drying operation.

Tangible personal property purchased by a person who is licensed to operate a commercial radio or television station in Wisconsin, if the property is used exclusively and directly in the origination or integration of various sources of program material for commercial radio or television transmissions that are generally available to the public free of charge without a subscription or service agreement.

Fuel and electricity consumed in the origination or integration of various sources of program material for commercial radio or television transmissions that are generally available to the public free of charge without a subscription or service agreement.

Percent of fuel exempt: |

|

% |

Percent of electricity exempt: |

|

% |

Tangible personal property, property, items and goods under s.77.52(1)(b), (c), and (d), or services purchased by a Native American

with enrollment #, who is enrolled with and resides on the Reservation, where buyer will take possession of such property, items, goods, or services.

Tangible personal property and items and property under s.77.52(1)(b) and (c) becoming a component of an industrial or municipal waste treatment facility, including replacement parts, chemicals, and supplies used or consumed in operating the facility. Caution: Do not check the “continuous” box at the top of page 1.

Portion of the amount of electricity or natural gas used or consumed in an industrial waste treatment facility.

(Percent of electricity or natural gas exempt %)

Electricity, natural gas, fuel oil, propane, coal, steam, corn, and wood (including wood pellets which are 100% wood) used for fuel

for residential or farm use. |

% of Electricity |

% of Natural Gas |

% of Fuel |

|||||

|

|

Exempt |

|

Exempt |

Exempt |

|||

Residential |

. |

|

% |

|

|

% |

|

% |

Farm |

|

% |

% |

% |

||||

Address Delivered: |

|

|

|

|

|

|

|

|

Percent of printed advertising material solely for

Catalogs, and the envelopes in which the catalogs are mailed, that are designed to advertise and promote the sale of merchandise or to advertise the services of individual business firms.

Computers and servers used primarily to store copies of the product that are sent to a digital printer, a

Purchases from

Other purchases exempted by law. (State items and exemption).

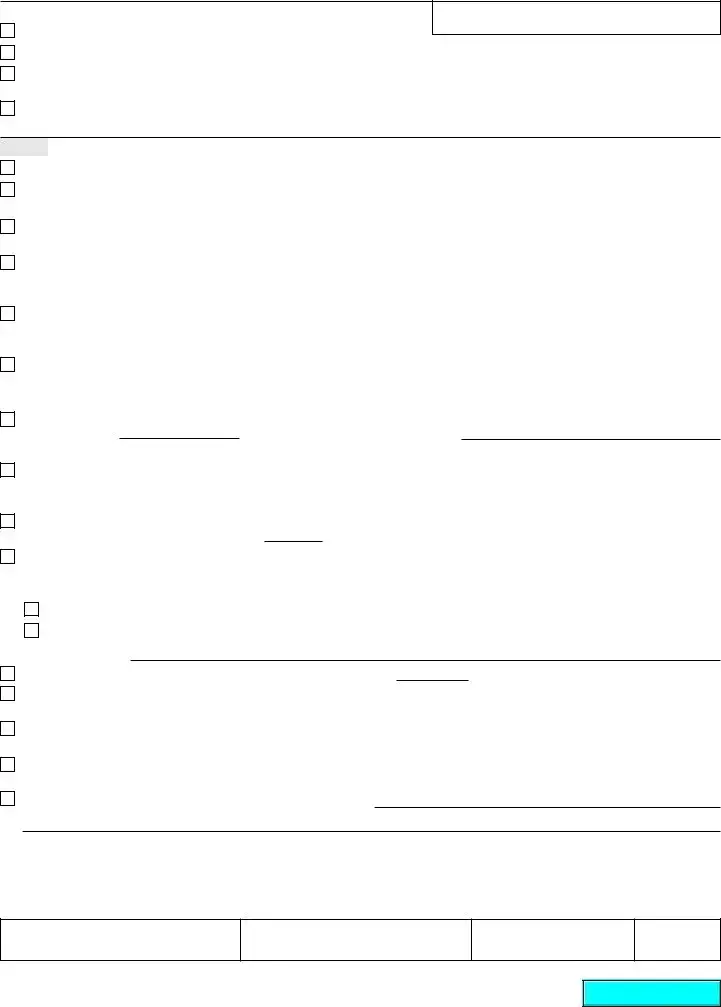

(DETACH AND PRESENT TO SELLER)

I declare that the information provided is complete and accurate to the best of my knowledge, and that the product(s) purchased will be used in the exempt manner indicated. If a product is not used in an exempt manner, I will remit use tax on the purchase price at the time of first taxable use. I understand that failure to remit the use tax may result in a future liability, including tax, interest, and penalty.

CAUTION: Using this certificate to avoid paying sales tax may result in a fine of $250 for each transaction for which the certificate is used

Signature of Purchaser

Print or Type Name

Title

Date

- 2 - |

Wisconsin Department of Revenue |

Return to Page 1

| Name | Fact | ||

|---|---|---|---|

| Form Type | Wisconsin Sales and Use Tax Exemption Certificate | ||

| Usage | Used for claiming exemption from Wisconsin state, county, baseball or football stadium, local exposition, and premier resort sales or use tax on certain purchases, leases, or rentals. | Exemption Categories | Resale, Farming equipment and supplies, Tractors and farm machines, Animal feed and livestock, Gardening supplies, and more. |

| Purchaser Information | Includes Business Name, Phone Number, and Address. | ||

| Claim Basis | Exemption claims are based on the purchaser's engagement in specific business activities and the direct use of purchased items within those activities. | ||

| Governing Law | Governed by Wisconsin Department of Revenue guidelines and regulations. | ||

| Certification Requirement | Purchasers must certify that items will be used in a qualifying manner, and acknowledge the obligation to remit use tax on items not used as exempted. | ||

| Penalties for Misuse | Failure to correctly apply exemption or remit use tax may result in tax liability including tax, interest, and penalties. |

Once you've determined the necessity for utilizing the Wisconsin Sales and Use Tax Exemption Certificate for your purchase, lease, or rental, it's essential to proceed with accuracy and attentiveness. This document is vital for transactions exempt from Wisconsin state, county, baseball or football stadium, local exposition, and premier resort sales or use tax. Proper completion of the form ensures your entitlement to exemption is clear and substantiated. Follow the steps below to fill out the form accurately.

Completing the Wisconsin Sales and Use Tax Exemption Certificate with precision is the first step toward ensuring your purchase, lease, or rental is processed without delay. This diligence ensures compliance with the Wisconsin Department of Revenue guidelines, safeguarding your business from potential misuse of the exemption. Following these instructions carefully will streamline the process, making it more efficient and less susceptible to errors that could impact your taxation obligations.

What is the Wisconsin Sales and Use Tax Exemption Certificate?

The Wisconsin Sales and Use Tax Exemption Certificate is a document that individuals or businesses in Wisconsin can use to claim exemption from state, county, baseball or football stadium, local exposition, and premier resort sales or use tax. It applies to the purchase, lease, or rental of tangible personal property or taxable services. This form allows a purchaser to certify their eligibility for tax exemption for certain types of purchases based on the business operation they are engaged in.

Who can use the Wisconsin Tax Exempt form?

Businesses or individuals who are engaged in specific types of operations that qualify for tax exemption can use this form. These operations may include, but are not limited to, the business of selling, leasing, or renting; farming and agriculture; or purchasing items for resale. The form requires detailed information regarding the nature of the exempt use and may require proof of eligibility for the claimed exemption.

What types of purchases qualify for the exemption?

Several categories of purchases may qualify for the exemption. For example, farming equipment, seeds, plants, fertilizers, livestock supplies, and other items used directly in the business of farming are eligible. Items intended for resale, goods used directly in certain businesses, and other categories as specified by Wisconsin laws can also qualify. The certificate specifies a range of exempt uses and purchasers should check the appropriate box(es) to indicate the nature of their exempt purchases.

How does one apply the exemption for a single purchase versus continuous purchases?

On the Wisconsin Tax Exempt form, there is an option to check "Single Purchase" or "Continuous" purchase at the top. If the form is used for a single exempt purchase, you must itemize the property purchased and it's only applicable to that one transaction. For continuous purchases, intended for ongoing use, no need to itemize every purchase, but the certificate should be updated as necessary to reflect current business operations and compliance with tax exemption qualifications.

What are the consequences of improper use of the tax exemption?

If items purchased under this exemption are not used in an exempt manner as certified, the purchaser is responsible for remitting the use tax on the purchase price at the time of the first taxable use. Failure to remit use tax when required can result in liability that includes taxes owed, interest, and penalties, emphasizing the importance of accurate and truthful use of this certificate.

How does one certify the exemption and what documentation is required?

To certify the exemption, the purchaser must sign the reverse side of the form, indicating their agreement to the terms and conditions of the tax exemption as stated on the certificate. This includes the promise to use the purchased items in an exempt manner. Documentation required usually involves providing a detailed description of the property or services purchased, the proposed exempt use, and possibly a seller’s permit or use tax certificate number if the purchase is for resale. It's crucial to keep records to support the exempt status of purchases, should verification by the Wisconsin Department of Revenue be necessary.

Filling out a Wisconsin Tax Exempt form can seem straightforward, but small mistakes can lead to big headaches down the line. To ensure the process is as seamless as possible, it's important to be aware of common errors people make when completing this form.

Not checking the correct exemption reason box. One of the most critical parts of the Wisconsin Tax Exempt form is identifying the reason for exemption. This decision impacts the documentation you need and the eligibility criteria you must meet. Individuals often mistakenly check the incorrect box or overlook this section altogether.

Incomplete purchaser information. Another common error involves failing to provide complete purchaser information, including the business name, phone number, and address. This omission can invalidate the exemption request, as the Department of Revenue requires these details to process the form.

Omitting the signature and title. The form is not valid unless it is signed by the purchaser or their authorized representative. In addition, the title of the person signing the form must be provided. Skipping these steps can cause unnecessary delays.

Here are additional pitfalls to avoid:

Being meticulous when filling out the Wisconsin Tax Exempt form is key to ensuring your purchase qualifies for tax exemption. Double-check your entries, make sure you have provided all required information accurately, and consult the detailed guidelines provided by the Wisconsin Department of Revenue if you're unsure about any part of the process. Avoiding these common mistakes will save you time and prevent potential issues with your tax exemption status.

When handling the Wisconsin Tax Exempt form, a comprehensive understanding of related documentation is essential for ensuring compliance and streamlining processes. Several documents often accompany the Wisconsin Tax Exempt form to reinforce the claims made or to fulfill additional legal requirements. Here's an overview of these imperative forms and documents:

Together with the Wisconsin Tax Exempt form, these documents form a comprehensive packet that supports an organization's tax exemption claim. They not only validate the legitimacy and operational integrity of the entity but also ensure adherence to both state and federal tax laws. Assembling these documents diligently is fundamental for any organization seeking to establish or maintain its tax-exempt status in Wisconsin.

The Uniform Sales & Use Tax Exemption/Resale Certificate - Multijurisdiction is a document used by businesses that purchase goods to resell, lease, or rent in several states, which exempts them from paying sales tax at the time of purchase. Much like the Wisconsin Sales and Use Tax Exemption Certificate, this document serves a similar purpose in providing a way for businesses to avoid paying sales tax on items that will be resold. It differs mainly in scope, as it applies to multiple jurisdictions rather than being specific to Wisconsin. This similarity stems from the overarching goal to prevent double taxation, first on the purchase by the reseller and again when the item is sold to the final consumer.

The Exemption Certificate for Purchases of Tangible Personal Property & Services for Resale specifically targets transactions where businesses buy goods or services to resell. This form directly parallels the Wisconsin Tax Exempt form in its function of exempting the purchaser from sales tax on such transactions. Its primary similarity lies in the focus on resale exemption, highlighting a common ground in promoting business-to-business transactions without the added burden of sales tax, thereby streamlining the resale process.

The Streamlined Sales and Use Tax Agreement Certificate of Exemption is a form utilized by businesses in states that are members of the Streamlined Sales and Use Tax Agreement to claim exemption from sales tax. It shares similarities with the Wisconsin Tax Exempt form in its purpose of providing tax exemptions for qualified purchases, including those intended for resale, use in production, and other exempt categories. The key link between these documents is their role in facilitating tax-exempt purchases under specific conditions, bound by regulations that aim to simplify the sales and use tax system across participating states.

The Nonprofit Organization Request for Sales Tax Exemption form, though it serves a more specific category of users, shares the foundational concept of tax exemption with the Wisconsin form. This document allows nonprofit organizations to claim exemption from sales tax on purchases related to their operations. Both forms illustrate the broad principle of tax exemption for eligible entities or activities, ensuring that certain purchases made in support of specific missions or business operations are not taxed, thereby supporting these entities in achieving their goals with lesser financial strain.

The Agricultural Sales and Use Tax Exemption Certificate is aimed at individuals or businesses involved in agriculture, offering tax exemptions on purchases of equipment, supplies, and services used directly in farming operations. This certificate is closely related to the Wisconsin Tax Exempt form, particularly in its provision for farming exemptions. Both documents recognize and support the agriculture sector by exempting from sales tax the purchase of items essential for farming, underlining the importance of the agricultural industry to the economy and ensuring the affordability of farming supplies and equipment.

The Direct Pay Permit allows qualified purchasers to buy goods and services without paying sales tax to the seller, opting instead to pay the tax directly to the state. It shares a common purpose with the Wisconsin Sales and Use Tax Exemption Certificate in managing how tax is accounted for on purchases. Although the process and eligibility may differ, both documents alleviate the immediate tax burden during transactions for authorized purchasers, facilitating a more direct control over tax liabilities.

The Reseller Permit issued by some states permits businesses to purchase goods tax-free if the goods are intended for resale. Similar to the Wisconsin exemption certificate, this permit underscores the principle of tax-free purchases for resale purposes. Both forms serve as proof that the purchaser is authorized to buy goods without paying sales tax at the point of sale, reinforcing the notion that tax should only be applied to the final consumer, thus preventing double taxation within the supply chain.

The Manufacturing Sales and Use Tax Exemption Certificate allows manufacturers to purchase materials and machinery tax-free when these items are to be used directly in the manufacturing process. This certificate aligns with the Wisconsin Tax Exempt form through its focus on tax exemptions for items used in production, supporting economic activities by reducing the cost of inputs for manufacturers. Both highlight a shared understanding of the importance of easing the financial burden on producers, facilitating a more efficient production process and ultimately benefitting the broader economy.

Correctly filling out the Wisconsin Tax Exempt form is essential for organizations or individuals to ensure they are not mistakenly paying taxes on items or services that are legally exempt. The following lists provide guidance on what you should and shouldn't do when completing this important document.

What You Should Do

Thoroughly review the form to understand all the required fields and information needed, including the specific exemptions available.

Ensure that the purchaser’s business name, phone number, and address are filled out completely and accurately.

Itemize the property purchased if making a single purchase to clearly identify what is being claimed as exempt from the sales tax.

If applicable, enter the purchaser’s seller’s permit or use tax certificate number when claiming exemption for resale purposes.

Check the appropriate box(es) indicating the proposed exempt use with accurate details, especially if the purchase is for farming, to ensure compliance with requirements for such exemptions.

Sign and date the form on the reverse side to certify the information provided is true and correct.

Keep a copy of the completed form for your records to have proof of the exemption claim and for future reference.

What You Shouldn't Do

Don’t rush through filling out the form without understanding each part; mistakes can lead to the rejection of the tax-exempt status.

Avoid providing incomplete or inaccurate information, as this can also lead to a denial of exemption.

Don’t forget to itemize purchases if selecting the single purchase option; a general description may not suffice.

Avoid making assumptions about whether a purchase is exempt; verify each item’s eligibility for exemption.

Don’t neglect to check the specific requirements for each exemption category, as failing to meet these can invalidate your claim.

Avoid using the form without properly certifying it with a signature and date; an unsigned form is not valid.

Don’t fail to update the Department of Revenue if there are changes in how the purchased items are used that might affect their tax-exempt status.

By carefully following these guidelines, you can effectively navigate the process of claiming your rightful tax exemptions on the Wisconsin Tax Exempt form, ensuring compliance while maximizing your savings.

When it comes to navigating state tax laws, misconceptions can lead to costly errors, especially with forms such as the Wisconsin Sales and Use Tax Exemption Certificate. It's essential to understand the common myths and the realities of tax-exempt purchases in Wisconsin.

Only Nonprofits Qualify: A common misconception is that tax exemption is exclusively for nonprofit organizations. In reality, this form can be used by various types of businesses, such as those in farming, reselling, or manufacturing, provided the goods or services purchased are for resale or used directly in the manufacturing or farming process.

Any Purchase Qualifies: Not all purchases by an exempt business qualify for exemption. The items must be used in a manner that directly relates to the business's exempt purpose. For example, a farmer cannot use this certificate to buy office supplies tax-free under the farming exemption.

Permanent Exemption: Some believe once they fill out a Wisconsin Tax Exempt form, their exemption is permanent. However, purchasers must specify whether their exemption is for a single purchase or continuous. Continuous exemptions require regular verification and compliance with Wisconsin tax laws.

No Need to Itemize for Single Purchases: Even if claiming an exemption for a single purchase, the specific items or services must be itemized and described on the form to ensure they qualify for exemption.

All Farm-related Purchases are Exempt: While many farm-related purchases qualify for exemption, they must be used directly and exclusively in the business of farming. Items not directly related to farming activities, even if used on a farm, may not qualify.

Immediate Use is Required: There's a belief that items must be put to use immediately after purchase to qualify for exemption. The crucial requirement is that the items are used in a manner consistent with the claimed exemption, regardless of the timing of their use.

Submission Guarantees Approval: Submitting a Wisconsin Tax Exempt form does not automatically guarantee approval. The Wisconsin Department of Revenue may require additional information or documentation to verify the exempt status of the purchase.

Understanding these misconceptions and their realities helps ensure that businesses can effectively manage their exemptions without facing unexpected tax liabilities. It's always advisable to consult with tax professionals or the Wisconsin Department of Revenue for guidance specific to your business situation.

Filling out and using the Wisconsin Tax Exempt form is an essential process for businesses looking to navigate state tax laws effectively. Here are five key takeaways to keep in mind:

It's also important to note that keeping records of your tax-exempt purchases is crucial in case of an audit. Documentation should clearly support the exempt purpose of each purchase, aligning with the details provided on the Wisconsin Tax Exempt form.

Wisconsin Doc 1163 - Including the subject's identifying information directly on the form streamlines the process of matching authorizations with the correct records.

Wisconsin Gab 131 - The requirement underscores Wisconsin's commitment to maintaining a transparent electoral environment.