Fill Your Wisconsin W706 Form

Fill Your Wisconsin W706 Form

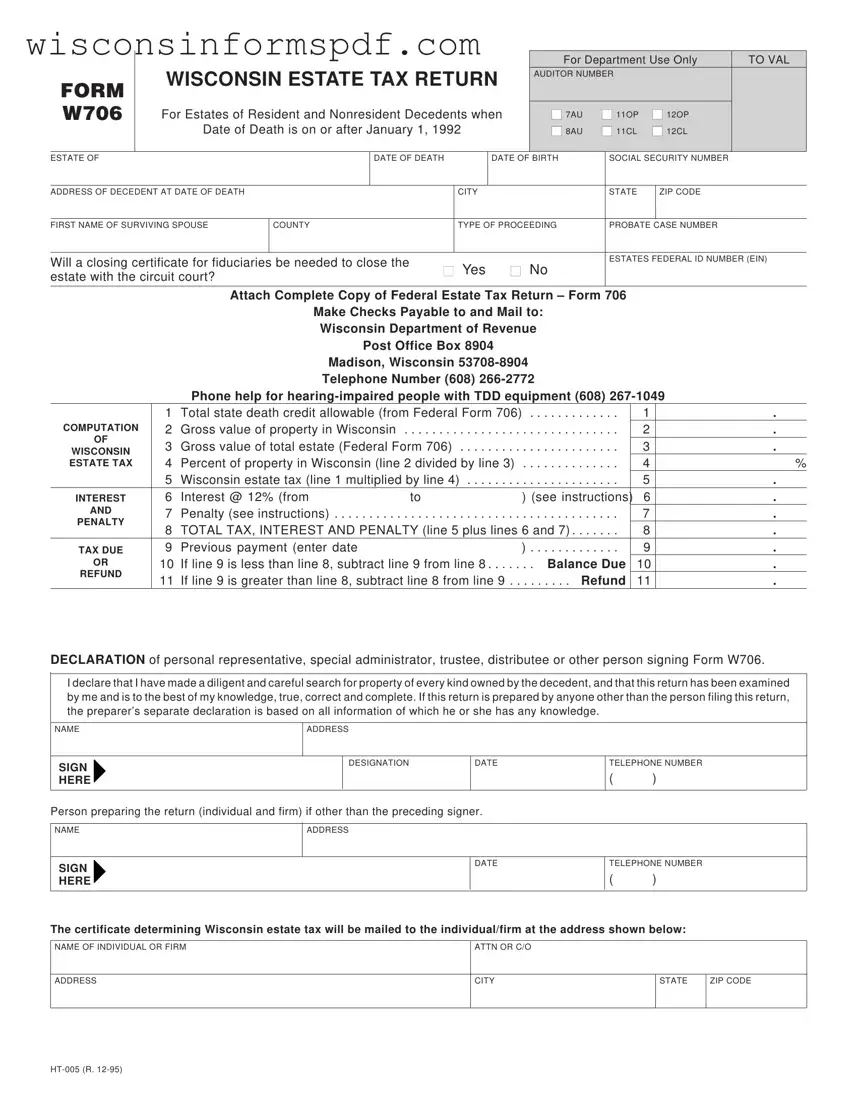

Navigating the landscape of estate planning and taxation can be complex, especially when it comes to fulfilling state-specific requirements. In Wisconsin, the W706 form serves as a crucial document for both resident and nonresident decedents, marking the final accounting of estate tax obligations. The form meticulously outlines various aspects, such as the total state death credit allowable from Federal Form 706, gross values of property both within Wisconsin and the entire estate, and the computation of taxes owed or refunds due. Furthermore, it asks for details on the decedent, including their name, date of birth, social security number, and the address at the time of death, alongside information regarding the surviving spouse, if any. Essential for the proper closing of an estate, it determines whether a closing certificate for fiduciaries is necessary. Completeness and accuracy are paramount in its submission, as it includes a declaration section where personal representatives or trustees affirm the diligent assessment of the decedent's property and truthfulness of the information provided. This comprehensive documentation aids the Wisconsin Department of Revenue in ensuring the rightful estate tax is assessed and collected, underscoring the legal and fiscal responsibilities that accompany the settlement of an estate.

|

|

|

|

|

|

|

|

|

|

|

|

|

For Department Use Only |

TO VAL |

||||||

|

|

WISCONSIN ESTATE TAX RETURN |

|

|

AUDITOR NUMBER |

|

|

|

|

|||||||||||

FORM |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

W706 |

|

For Estates of Resident and Nonresident Decedents when |

|

|

■ 7AU |

■ 11OP |

■ 12OP |

|

||||||||||||

|

|

|

Date of Death is on or after January 1, 1992 |

|

|

■ 8AU |

■ 11CL |

■ 12CL |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

ESTATE OF |

|

|

|

|

|

DATE OF DEATH |

|

DATE OF BIRTH |

|

SOCIAL SECURITY NUMBER |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

ADDRESS OF DECEDENT AT DATE OF DEATH |

|

|

|

CITY |

|

|

|

|

STATE |

|

ZIP CODE |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

FIRST NAME OF SURVIVING SPOUSE |

|

COUNTY |

|

|

|

TYPE OF PROCEEDING |

|

PROBATE CASE NUMBER |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Will a closing certificate for fiduciaries be needed to close the |

|

|

|

|

|

|

|

ESTATES FEDERAL ID NUMBER (EIN) |

||||||||||||

■ |

Yes |

■ |

|

No |

|

|

|

|

|

|

|

|||||||||

estate with the circuit court? |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

Attach Complete Copy of Federal Estate Tax Return – Form 706 |

|

|

|

|

||||||||||||

|

|

|

|

|

|

Make Checks Payable to and Mail to: |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

Wisconsin Department of Revenue |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

Post Office Box 8904 |

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

Madison, Wisconsin |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

Telephone Number (608) |

|

|

|

|

|

|

|

|||||||

|

|

|

Phone help for |

|

||||||||||||||||

|

|

1 |

Total state death credit allowable (from Federal Form 706) |

. |

. . |

|

1 |

|

|

. |

||||||||||

COMPUTATION |

2 |

Gross value of property in Wisconsin . |

. . . . . . . |

. . . . |

. . . |

. . |

. |

. . . . . . . . . . |

. |

. . |

|

2 |

|

|

. |

|||||

OF |

3 |

Gross value of total estate (Federal Form 706) |

|

|

|

|

|

|

|

|

3 |

|

|

. |

||||||

WISCONSIN |

. . . . |

. . . |

. . |

. |

. . . . . . . . . . |

. |

. . |

|

|

|

||||||||||

4 |

Percent of property in Wisconsin (line 2 divided by line 3) |

|

|

|

|

|

4 |

|

|

% |

||||||||||

ESTATE TAX |

. |

. . . . . . . . . . |

. |

. . |

|

|

|

|||||||||||||

|

|

5 |

Wisconsin estate tax (line 1 multiplied by line 4) |

. . |

. |

. . . . . . . . . . |

. |

. . |

|

5 |

|

|

. |

|||||||

INTEREST |

6 |

Interest @ 12% (from |

|

|

to |

|

|

|

) (see instructions) |

|

6 |

|

|

. |

||||||

AND |

7 |

Penalty (see instructions) |

|

|

|

|

|

|

|

|

|

7 |

|

|

. |

|||||

PENALTY |

. . . . |

. . . |

. . |

. |

. . . . . . . . . . |

. |

. . |

|

|

|

||||||||||

8 |

TOTAL TAX, INTEREST AND PENALTY (line 5 plus lines 6 and 7) |

|

|

|

8 |

|

|

. |

||||||||||||

|

|

. |

. . |

|

|

|

||||||||||||||

TAX DUE |

9 |

Previous payment (enter date |

|

|

|

|

) |

. . . . . . . . . . |

. |

. . |

|

9 |

|

|

. |

|||||

OR |

10 |

If line 9 is less than line 8, subtract line 9 from line 8 . . . |

. . |

. |

. Balance Due |

|

10 |

|

|

. |

||||||||||

REFUND |

11 |

If line 9 is greater than line 8, subtract line 8 from line 9 |

|

|

. . . . . . Refund |

|

11 |

|

|

. |

||||||||||

|

|

. . |

. |

|

|

|

||||||||||||||

DECLARATION of personal representative, special administrator, trustee, distributee or other person signing Form W706.

I declare that I have made a diligent and careful search for property of every kind owned by the decedent, and that this return has been examined by me and is to the best of my knowledge, true, correct and complete. If this return is prepared by anyone other than the person filing this return, the preparer’s separate declaration is based on all information of which he or she has any knowledge.

NAME

ADDRESS

SIGN  HERE

HERE

DESIGNATION

DATE

TELEPHONE NUMBER

( )

Person preparing the return (individual and firm) if other than the preceding signer.

NAME

ADDRESS

SIGN  HERE

HERE

DATE

TELEPHONE NUMBER

( )

The certificate determining Wisconsin estate tax will be mailed to the individual/firm at the address shown below:

NAME OF INDIVIDUAL OR FIRM

ATTN OR C/O

ADDRESS

CITY

STATE

ZIP CODE

| Fact Name | Description |

|---|---|

| Form Identifier | The form is known as the Wisconsin Estate Tax Return, designated as Form W706. |

| Applicability | This form is used for estates of both resident and nonresident decedents whose date of death is on or after January 1, 1992. |

| Submission Requirements | A complete copy of the Federal Estate Tax Return – Form 706 is required to be attached with the submission to the Wisconsin Department of Revenue. |

| Governing Law | The form is governed by Wisconsin state law relating to the taxation of estates, which outlines the computation of the state's portion of estate tax based on the total estate value and the portion of the estate located in Wisconsin. |

Filling out the Wisconsin W706 form is a crucial step for executors or administrators handling the estate of someone who has passed away. This document helps ensure that the estate is in compliance with Wisconsin's estate tax obligations. Completing it accurately is essential for a smooth process in settling the decedent's affairs. Here's how to approach it.

Upon completing and signing the Wisconsin W706 form, it should be mailed, along with any required attachments, to the address provided on the form. Accurate completion and timely submission of this form are vital steps in fulfilling the estate's tax obligations and moving forward in the estate settlement process.

What is the Form W706 and who needs to fill it out?

The Form W706, known as the Wisconsin Estate Tax Return, is a document required for the estates of both resident and nonresident decedents when the date of death is on or after January 1, 1992. It's necessary for personal representatives, special administrators, trustees, distributees or others in charge of the decedent's estate to fill out and submit this form if managing an estate that includes assets in Wisconsin. The form helps in calculating the estate tax owed to the state based on the value of the property in Wisconsin compared to the total estate value.

How do I know if I need to obtain a closing certificate for fiduciaries to close the estate with the circuit court?

Whether you need to obtain a closing certificate for fiduciaries to close the estate with the circuit court is indicated on the Form W706 under the specific question asking for this requirement. You should select "Yes" if you need the certificate. It is generally required when you are finalizing estate matters in circuit court to legally conclude the estate's distribution. It is advisable to consult with a professional if you are unsure about your specific situation.

Where should the completed Form W706 be mailed, and to whom should the checks be payable?

Once completed, the Form W706 should be mailed to the Wisconsin Department of Revenue at Post Office Box 8904, Madison, Wisconsin, 53708-8904. Any checks associated with the estate tax, including payments for taxes owed or penalty fees, should be made payable to the "Wisconsin Department of Revenue." This ensures that your payment is properly processed and credited to the estate's tax obligation. Remember to include the estate's federal ID number (EIN) on the check for precise identification.

How is the Wisconsin estate tax calculated according to the Form W706 instructions?

The Wisconsin estate tax is calculated by first determining the total state death credit allowable from Federal Form 706. Then, the gross value of the property located in Wisconsin is identified, along with the gross value of the total estate as reported on Federal Form 706. The percentage of the property in Wisconsin relative to the total estate is calculated, and this percentage is applied to the initial state death credit to determine the Wisconsin estate tax due. Interest and penalties may also apply if the tax is not paid by the due date, further increasing the total amount owed.

Filling out the Wisconsin Estate Tax Return, Form W706, is crucial for managing the estate of a resident or nonresident decedent when the date of death is on or after January 1, 1992. However, individuals often encounter obstacles during this process. Recognizing and avoiding these common mistakes can streamline the submission process, ensuring accuracy and compliance with state requirements.

One prevalent error is the failure to attach the complete copy of the Federal Estate Tax Return – Form 706. This document is essential for the Wisconsin Department of Revenue to assess the estate correctly. When it is missing, the processing of the Wisconsin Estate Tax Return can be delayed, complicating estate settlement.

Incorrect computation of the "Total state death credit allowable" and the "Gross value of property in Wisconsin" leads to the misapplication of tax rates and exemptions. These values are foundational for determining the estate's tax liability in Wisconsin and require meticulous attention to detail to ensure they are accurately reported.

Not indicating whether a closing certificate for fiduciaries is needed to close the estate with the circuit court is another oversight. This indication helps the Department of Revenue understand the specifics of the estate’s legal and financial closure requirements.

Miscalculating the amounts related to "Interest" and "Penalty" sections can also occur. The requirement to compute interest at 12% and penalties for late payments necessitates precise calculations. When these figures are inaccurately reported, it can result in either an overpayment or an underpayment of taxes, each leading to further correspondence and adjustments with the Department of Revenue.

Addressing these common mistakes demands a thoughtful and thorough review of the entire Form W706 documentation. Utilizing professional guidance or double-checking entries against estate records can help prevent these errors. Furthermore, individuals must take note of the declaration section, ensuring that all information provided is true, correct, and complete to the best of their knowledge.

Inaccuracies or omissions in the Wisconsin Estate Tax Return not only delay the processing time but can also affect the overall settlement of the estate. By acknowledging and rectifying these mistakes, individuals can contribute to a smoother estate management process.

When managing an estate in Wisconsin, particularly for those with a requirement to submit a Wisconsin Estate Tax Return (Form W706), there are several key documents and forms that often accompany or follow the initial filing. These documents serve various roles, from declaring the value of the estate, to ensuring proper distribution and closure of the estate's financial obligations. The seamless integration and timely submission of these related forms can significantly ease the process of estate settlement.

The navigation through estate management and tax obligations necessitates a comprehensive approach, incorporating various documents beyond the initial Wisconsin Estate Tax Return. Each form carries its importance in validating, transferring, and finalizing the estate's matters, ensuring adherence to both state tax laws and probate regulations. The efficient handling of these forms reflects diligent estate administration, offering peace of mind to executors and heirs alike.

The Wisconsin W706 form, a primary document for computing and filing estate taxes, shares similarities with the Federal Estate Tax Return, Form 706, in structure and purpose. Both forms are used to calculate the estate tax due following an individual's death, relying on the valuation of the decedent's estate. The crucial commonality lies in their requirement for detailed listing and valuation of the decedent's assets to determine tax responsibility. Additionally, they include deductions applicable to the estate's total value, significantly impacting the final estate tax computation.

Comparable to the Wisconsin W706 is the Form 1041, U.S. Income Tax Return for Estates and Trusts, which also deals with financial matters post-death. While the Wisconsin W706 focuses on estate tax, Form 1041 addresses income generated by the estate or trust after the decedent's passing. Both necessitate an executor or administrator to report values related to the decedent’s assets but diverge in their specific tax implications — estate tax versus income tax on assets' earnings.

Another document sharing similarities with the Wisconsin W706 form is the Form SS-4, Application for Employer Identification Number (EIN). Executors dealing with the Wisconsin W706 form often need an EIN for the estate, a prerequisite for filing taxes, opening bank accounts, and other financial transactions for the estate. While Form SS-4 is used to obtain this critical nine-digit number, used similarly to a Social Security number for individuals, it complements the estate administration process integral to the W706's context.

Similarly, the Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, parallels the Wisconsin W706 form in the realm of transfer taxes. Both are pivotal for reporting transfers of wealth, albeit at different stages — Form 709 for gifts made during the decedent’s life and the W706 form for wealth transferred after death. Each form aids in ensuring that these transfers are documented and any necessary taxes are calculated and collected to adhere to federal and state tax codes.

The Transfer on Death (TOD) Registration for Securities form evidences another point of similarity with the Wisconsin W706 in asset transition mechanisms post-death. While the TOD form facilitates the direct transfer of securities to named beneficiaries upon death, bypassing probate, the Wisconsin W706 encompasses a broader spectrum of estate assets for tax purposes. Both serve pivotal roles in managing asset distribution after death but from different angles — one avoiding probate and the other assessing tax implications.

In addition, the Petition for Probate form, often used to commence the probate process, indirectly complements the Wisconsin W706 form. The probate process involves validating the will, appointing an executor, and managing the deceased's estate, during which the estate's value is assessed — information crucial for completing the W706. Although they cater to different procedural aspects (legal authority for estate management versus tax liability), both forms are inherently connected through the estate administration process.

The Real Estate Transfer Return (RETR) form in Wisconsin shares a conceptual link with the Wisconsin W706 form by involving property assessment and tax implications connected to ownership transitions. The RETR is necessary for documenting the transfer of real estate and calculating transfer fees, while the W706 assesses estate tax based on the entire estate value, including real property. Despite differing focuses — one on a singular property transfer and the other on the estate as a whole — both underline the importance of accurately reporting property values for tax purposes.

Lastly, the Affidavit for Transfer of Personal Property Without Probate form parallels the purpose of the Wisconsin W706 in facilitating asset distribution after death. This form allows for a simpler transfer of personal property to beneficiaries without undergoing the full probate process, similar to how the TOD form operates for securities. While it simplifies asset distribution for smaller estates or specific assets, the W706 form captures the broader fiscal responsibility of estate taxation. Together, they represent different facets of managing and settling decedent estates in Wisconsin.

Filling out the Wisconsin W706 form, a critical document for reporting estate taxes, demands meticulous attention to detail and adherence to specific guidelines. The process, while complex, can be navigated successfully with a clear understanding of what should and shouldn't be done.

Do's:

Don'ts:

Each field and declaration in the Wisconsin W706 form serves pivotal roles in computing the estate's tax obligations accurately. Adhering to these guidelines not only facilitates a smoother processing experience but also ensures compliance with state tax laws, ultimately safeguarding against potential pitfalls and penalties associated with incomplete or incorrect filings.

When approaching the topic of estate planning and tax obligations in Wisconsin, there’s often a cloud of misconceptions surrounding the W706 form. Understanding the common misunderstandings can provide clarity for individuals navigating through these sometimes challenging waters.

Misconception #1: The W706 form is only for residents of Wisconsin.

While the form is primarily designed for estates of Wisconsin residents, it's equally pertinent for nonresidents who own property within the state. The requirement hinges not on residency but on whether the decedent owned property in Wisconsin, thus potentially owing estate taxes to the state.

Misconception #2: All estates must file Form W706 regardless of their size.

The necessity to file the W706 is not universal for all estates. It's contingent upon the gross value of the decedent’s estate, including property located within Wisconsin, surpassing certain thresholds that necessitate filing a federal estate tax return.

Misconception #3: Form W706 is the only document needed for estate tax purposes.

Completing Form W706 is just one step in the process. The form explicitly instructs the estate's representative to attach a complete copy of the federal estate tax return (Form 706). This implies the interdependence of state and federal estate tax filings.

Misconception #4: The Wisconsin Estate Tax can simply be estimated.

The calculation of the Wisconsin estate tax is not straightforward and cannot be merely estimated. It requires precise computations based on the allowable state death credit from the federal estate tax form and the proportional value of the estate's property located in Wisconsin.

Misconception #5: A closing certificate for fiduciaries is optional.

This document is crucial for legally closing the estate in the eyes of the court. The query regarding its necessity is not a matter of option but a step that clarifies whether this legal document, confirming tax obligations have been met, is needed to finalize the estate's closing.

Misconception #6: The declaration section is a formality without legal bearing.

The declaration made by the personal representative or other signing party is a legally binding assertion. It confirms that a diligent search for the decedent's property was conducted and that the information provided is accurate to the best of their knowledge, with significant legal implications for inaccuracies.

Misconception #7: Interest and penalties are rare.

Interest and penalties can and will be applied if taxes are overdue or filings are late. The rate and conditions under which they apply are explicitly stated, underscoring the importance of timely and accurate submissions.

Misconception #8: Previous payments are automatically deducted from the total tax obligation.

Calculating the balance due or refund involves explicitly acknowledging previous payments. This step is not automatic; it requires accurate documentation and calculation to ensure the estate’s tax obligation reflects these payments.

Misconception #9: The mailing address for the W706 is insignificant.

The address provided not only directs where the completed form and accompanying payment or correspondence should be sent, it also serves as the destination for the certificate determining Wisconsin estate tax. Accuracy in this detail is crucial for ensuring that all pertinent documents reach their intended recipients without delay.

When managing the estate of a deceased individual, the Wisconsin W706 form plays a vital role for both resident and nonresident decedents who passed away on or after January 1, 1992. Here are some key takeaways that can guide you through the process of filling out and using this form:

Making checks payable to the Wisconsin Department of Revenue and understanding where to mail the completed form is crucial for timely and proper filing. Always confirm the latest address and requirements, as these can change.

Wisconsin Permit - This form is essential for anyone looking to renew their existing Wisconsin driver license.

Wisconsin Lien Release Form - Streamlines the process of lien release upon the final payment for labor and materials.