Fill Your Wisconsin Wt 6 Withholding Form

Fill Your Wisconsin Wt 6 Withholding Form

Handling payroll and tax obligations is a crucial part of running a business with employees. In Wisconsin, one key document that employers must become familiar with is the Wisconsin Wt 6 Withholding form. This form plays a significant role in the process of reporting and remitting state income taxes withheld from employees' wages. It's not just about fulfilling a legal requirement; it's about ensuring that employers are contributing to the state’s economy in a direct and impactful way. The form requires detailed information regarding the amount of income tax withheld from employees during the reporting period, which can be monthly, quarterly, or annually based on the employer's total tax liability. By accurately completing and submitting this form, businesses not only comply with state laws but also help to streamline their own financial operations and support the maintenance of public services in Wisconsin.

| Fact | Description |

|---|---|

| Purpose | The Wisconsin WT-6 Withholding Tax Form is used by employers to report withholding taxes on a quarterly basis to the Wisconsin Department of Revenue. |

| Governing Law | This form is governed by Wisconsin Statutes, specifically by the provisions related to the collection and remittance of income taxes withheld by employers. |

| Due Dates | Due dates for the WT-6 form are tied to the quarter during which taxes were withheld: April 30 for Q1, July 31 for Q2, October 31 for Q3, and January 31 for Q4. |

| Filing Method | Employers have the option to file this form electronically through the Wisconsin Department of Revenue's website or by submitting a paper copy via mail. |

| Penalties for Late Filing | Late filing of the WT-6 form can result in penalties, which include a percentage of the tax owed plus interest on the overdue amount. |

Preparing and submitting the Wisconsin WT-6 Withholding Tax Form is a straightforward process, necessary for businesses operating within the state to comply with local tax regulations. This document plays a pivotal role in ensuring the accurate and timely payment of withheld taxes from employees' wages. By following a sequence of well-defined steps, entities can fulfill this obligation accurately, thus avoiding potential penalties and ensuring their operations run smoothly. Below is a clear, step-by-step guide intended to assist in this crucial task.

Completing the Wisconsin WT-6 Withholding Tax Form is essential for compliance with state tax obligations. By methodically preparing this document, businesses can maintain good standing with the Wisconsin Department of Revenue. Timely and accurate submissions not only fulfill legal requirements but also contribute to the integrity and financial health of any business operating within the state.

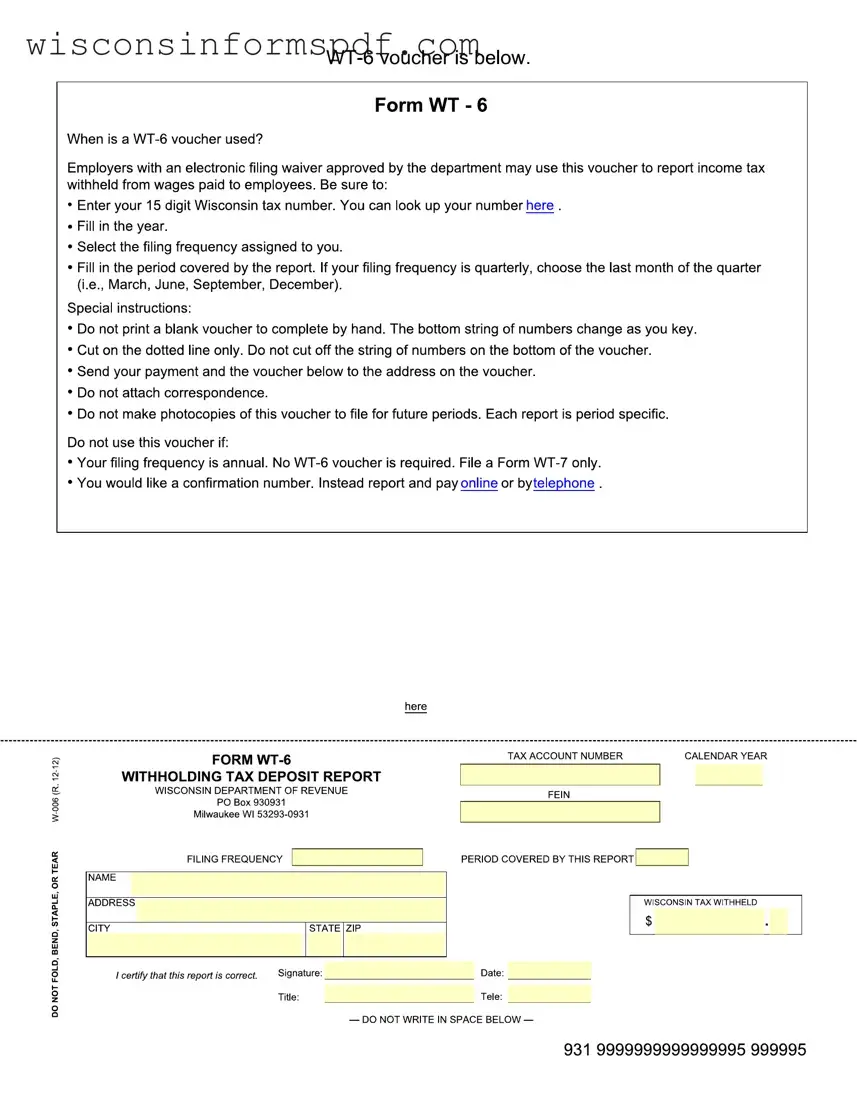

What is the Wisconsin WT-6 Withholding Form?

The Wisconsin WT-6 Withholding Form is a document that employers in Wisconsin must submit to report the amount of state income tax withheld from their employees' wages. This form helps in ensuring that employees have the correct amount of state income tax withheld from their pay, which is critical for compliance with state tax laws.

Who needs to file the Wisconsin WT-6 Withholding Form?

Any employer who withholds Wisconsin state income tax from employee wages is required to file the Wisconsin WT-6 Withholding Form. This requirement applies to all sizes of employers, from small businesses to large corporations, as long as they have employees from whom they withhold state income tax.

When is the Wisconsin WT-6 Withholding Form due?

The due date for submitting the Wisconsin WT-6 Withholding Form depends on the employer's withholding volume. Employers may be required to file this form on a quarterly, monthly, or even more frequent basis. Typically, quarterly filers must submit the form by the last day of the month following the end of the quarter, while monthly filers have a due date of the 15th day of the month following the reporting month. It is important for employers to verify their specific filing deadline based on their withholding amounts.

How can I submit the Wisconsin WT-6 Withholding Form?

Employers have the option to submit the Wisconsin WT-6 Withholding Form electronically through the Wisconsin Department of Revenue website or by mailing a paper form. Electronic filing is encouraged for its convenience and efficiency, but some employers may prefer or be required to submit a paper form, depending on their situation.

What information is required on the Wisconsin WT-6 Withholding Form?

The Wisconsin WT-6 Withholding Form requires detailed information about the employer's withheld state income tax. This includes the total amount of Wisconsin income tax withheld from employees' wages during the reporting period, the number of employees, the period covered, and the employer’s identification information. Accurate and complete information is crucial for the form's submission.

Can I correct a mistake on a previously submitted Wisconsin WT-6 Withholding Form?

Yes, employers can correct errors on a previously submitted Wisconsin WT-6 Withholding Form. To make a correction, an employer needs to submit an amended form for the period in which the mistake occurred. Detailed instructions for how to amend the form can be found on the Wisconsin Department of Revenue website or by contacting their support services. It is important to address and correct any errors promptly to avoid potential penalties.

Filling out the Wisconsin WT-6 Withholding Tax Form is an important task for businesses, ensuring compliance with state tax laws. However, individuals often encounter mistakes during this process. Identifying and avoiding these errors is crucial for timely and accurate submissions.

Not Updating Company Information: One of the common errors is neglecting to update company information. This includes changes in address, business name, or ownership. Accurate and current information is essential for the Wisconsin Department of Revenue to process forms and communicate effectively.

Incorrect EIN Usage: Employers must provide their Employer Identification Number (EIN) on the WT-6 form. Mistyping or using an incorrect EIN can lead to processing delays and potential penalties. It's crucial to double-check this number for accuracy.

Failing to Specify the Reporting Period: The WT-6 form requires businesses to specify the reporting period clearly. This period informs the state of the time frame for the reported withholdings. A common mistake is providing vague or incorrect reporting period dates, which can result in the form being returned for correction.

Omitting Required Signatures: A formal signature from an authorized individual is mandatory on the WT-6 form. This oversight can be easily overlooked but is critical for validating the document. Without a signature, the form is incomplete and will not be processed.

Inaccurate Withholding Amounts: Reporting incorrect amounts of tax withheld from employees or making calculation errors is a significant issue. These inaccuracies can lead to discrepancies with employee records and potential conflicts with state tax obligations. It's important to carefully review and ensure that all withholding amounts are reported accurately.

By paying close attention to these common pitfalls, businesses can improve their compliance with Wisconsin's tax requirements. Diligence in reviewing and submitting the WT-6 Withholding Tax Form can save time and prevent unnecessary complications with the Wisconsin Department of Revenue.

When businesses in Wisconsin manage their tax responsibilities, the Wisconsin WT-6 Withholding Tax Form is a key component of the process. This form serves as a withholding tax deposit report that employers must file to report income taxes withheld from employees' wages. However, this form is often accompanied by several other important documents and forms that facilitate comprehensive tax compliance and payroll management. Here is an overview of other significant documents often used alongside the Wisconsin WT-6 form.

These documents play a crucial role in ensuring that both employees' rights are protected and employers fulfill their legal obligations. Managing taxes and employment documentation can be complex, but these forms provide a structured way to navigate these responsibilities effectively. Employers should pay close attention to the requirements for each form to maintain compliance with state and federal laws.

The Wisconsin WT-6 Withholding Tax Deposit Report shares similarities with the Federal Form 941, Employer's Quarterly Federal Tax Return. Both forms are used for reporting taxes withheld from employees' wages. While the WT-6 focuses on state income tax withholding specific to Wisconsin, the Federal Form 941 covers withholding of federal income tax, Social Security, and Medicare taxes. Both forms require employers to calculate the total taxes withheld from employees during the reporting period and report any deposits of these taxes.

Similar to the Wisconsin WT-6 is the Form W-2, Wage and Tax Statement, in the sense that both involve wage reporting and tax withholding information. The WT-6 is used by employers to report the total amount of taxes withheld from all employees to the state, whereas the Form W-2 is issued to employees detailing their annual wages and the amount of taxes withheld from their paychecks for that year. Both documents are integral to ensuring correct income tax reporting and compliance.

Another document resembling the Wisconsin WT-6 is the Form W-3, Transmittal of Wage and Tax Statements. The Form W-3 is used to transmit Form W-2s to the Social Security Administration and summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the year. Though the Form W-3 deals with federal reporting, its function as a summary document mirrors the state-level summary reporting of the WT-6.

The Wisconsin WT-7, Employers Annual Reconciliation of Wisconsin Income Tax Withheld from Wages, is closely related to the WT-6. While the WT-6 is utilized for periodic withholding tax deposits, the WT-7 serves as an annual reconciliation form where employers report the total amounts of Wisconsin income taxes withheld from employees' wages throughout the entire year. Both forms are crucial for state tax compliance and ensuring accurate withholding and reporting.

The Quarterly Contribution Report to Unemployment Insurance (UI) is another document with a similar purpose to the WT-6. Although the focus is on unemployment insurance contributions rather than income tax withholdings, both forms require employers to report amounts that have been deducted from employees' wages and paid to the government. These reports ensure employers contribute to state-run programs accurately.

Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return, is somewhat akin to the WT-6 in that it deals with employer contributions based on employee wages. However, Form 940 is specific to reporting and paying unemployment taxes to the federal government. Both forms are part of the payroll tax reporting requirements, ensuring employers support federal and state programs designed to assist with unemployment.

The State Unemployment Tax Act (SUTA) report, similar to the Federal Unemployment Tax Act (FUTA) filings, is akin to the WT-6 in the realm of state requirements. This report concerns state unemployment insurance taxes and requires employers to report wages paid to employees, similar to how the WT-6 reports state income tax withholdings. Both are mandatory for employers and are used to fund respective state and federal unemployment insurance benefits.

Form 1099-MISC, Miscellaneous Income, though not used by employers for reporting employee wages, is similar to the WT-6 in its purpose of reporting specific types of payments. The 1099-MISC is used to report payments made in the course of a business to individuals not employed by the business, such as independent contractors. Like the WT-6, it's essential for tax reporting and compliance, ensuring all income is reported to tax authorities.

The Employer's Quarterly State Tax Return is an analogous document to the Wisconsin WT-6, but it may be specific to other states. This form is used by employers to report wages paid, taxes withheld, and taxes due to the state. Each state has its own version of this form for state income tax withholding, similar to how the WT-6 is used in Wisconsin, underscoring the uniform need across the U.S. for employers to report and remit taxes withheld from employees' wages.

Finally, the Adjusted Employer's Quarterly Federal or State Tax Return is related to the Wisconsin WT-6 as both may be used to make adjustments to previously reported tax information. Adjustments may be needed if errors were made in reporting the amount of tax withheld or wages paid. Both forms allow employers to correct these errors and ensure accurate tax reporting and compliance.

Filling out the Wisconsin WT-6 Withholding form is a crucial task for businesses operating within the state. Here's a helpful guide to navigate this process, highlighting key dos and don'ts to ensure accuracy and compliance.

Do:

Read the instructions carefully before you begin. The guidelines provided are designed to help you fill out the form correctly.

Gather all necessary information, including your federal employer identification number (EIN), the reporting period, and the total amount of Wisconsin income tax withheld during the period.

Use precise figures. Estimate values can lead to discrepancies and potentially, penalties.

Verify all information before submission, particularly the EIN and the reporting period, to avoid processing delays.

Submit the form before the due date to avoid late fees and interest charges. The due dates vary depending on your withholding frequency.

Keep a copy of the submitted form and any related documents for your records. This will be helpful in case of any inquiries from the tax department.

Use the electronic filing option if available. E-filing is faster, more secure, and often more convenient.

Don't:

Leave any fields blank. If a section does not apply to your situation, enter 'N/A' (Not Applicable) or '0,' depending on what is more appropriate.

Misstate your withholding amount. Reporting incorrect amounts can result in interest and penalties.

Forget to sign the form if submitting by paper. An unsigned form is not valid and will not be processed.

Ignore the rounding instructions. If the form specifies to round figures to the nearest dollar, do so to ensure your form is correctly processed.

Use correction fluid or tape. If you make a mistake, start over on a new form. Alterations can void the form.

Submit the form without a payment, if you owe withholding taxes. Payments and forms often go hand-in-hand, and overlooking this can lead to penalties.

Assume the mailing address is the same every year. Always check the current form for the correct mailing address or electronic filing options.

Understanding the Wisconsin WT-6 Withholding form is crucial for businesses operating within the state. However, several misconceptions can lead to confusion and potential non-compliance. Here is a list of ten common misconceptions and clarifications to help guide you through the correct processing of this form.

It's only for large businesses: Many people believe that the WT-6 Withholding form is only a requirement for large businesses. However, any business that has employees and withholds income tax from wages in Wisconsin must file this form, regardless of its size.

It's filed annually: A common mistake is thinking that the form is submitted on an annual basis. In reality, the WT-6 Withholding form is a quarterly tax form. Businesses need to file it by the last day of the month following the end of the quarter.

Electronic filing is optional: While Wisconsin does allow paper filings, it strongly encourages businesses to file the WT-6 form electronically. In some cases, depending on the amount of Wisconsin tax withheld, electronic filing is mandatory.

No penalty for late filing: Filing the WT-6 form late can result in penalties and interest charges. Timely filing is important to avoid unnecessary costs.

You can estimate amounts: Accuracy is crucial when completing the WT-6 form. Estimated amounts can lead to discrepancies and may trigger audits or reviews by the state department.

Only taxable wages are reported: The WT-6 form requires reporting of all wages paid to employees, including those that may be exempt from federal taxes but are subject to Wisconsin withholding.

Amendments are discouraged: Should you realize an error after submission, amendments are not only allowed but are necessary to ensure accurate reporting and compliance. Wisconsin provides a process for correcting previously filed WT-6 forms.

It's the same as the federal withholding form: While similar in purpose to federal withholding forms, the WT-6 is specific to Wisconsin and must be filed in addition to any federal withholding tax forms. Compliance with state regulations requires attention to both federal and state forms.

Payment is due with the annual return: Although the final payment of withheld taxes may be aligned with the filing of the annual return, quarterly payments must be made with each WT-6 filing throughout the year.

Non-profit organizations are exempt: While some non-profits may have exemptions from income tax, if they have employees earning wages in Wisconsin, they are generally required to file the WT-6 form and withhold state income tax accordingly.

Misunderstandings about the WT-6 Withholding form can lead to errors in compliance. It's important for all Wisconsin employers to be properly informed about their filing obligations to maintain good standing with state tax regulations.

Filling out and properly using the Wisconsin WT-6 Withholding Form is a crucial process for employers in the state. This form plays a significant role in the management of state income tax withholdings for employees. To ensure compliance and avoid potential issues with the Wisconsin Department of Revenue, here are key takeaways to consider:

Proper attention to detail and adherence to the stated guidelines will ensure that the process of filing and using the Wisconsin WT-6 Withholding Form is as smooth and error-free as possible. Employers who take these steps not only comply with state tax laws but also protect their business and employees.

Wisconsin Cfs 2114 - By focusing on the improvement to facility operations and child care delivery, the form connects learning outcomes directly to practical application.

Wisconsin Department of Revenue Payment Plan - There is a clause that allows the department to void the agreement if false information was provided.

Motion to Modify Placement Wisconsin Form - The FA-604 form is indispensable for Wisconsin residents seeking court approval to modify existing legal judgments concerning family matters.