Fill Your Wisconsin Pr 230 Form

Fill Your Wisconsin Pr 230 Form

In navigating the complexities of property tax exemptions within the State of Wisconsin, the PR-230 form emerges as an instrumental document for property owners seeking relief for the current assessment year. Mandated by state law, this detailed form lays down the procedural blueprint that property owners must follow to potentially secure an exemption. Failure to file the form in its entirety, accompanied by the necessary attachments, could lead to a denial of the exemption request. It sets a clear deadline of March 1st for submission to the taxation district's assessor where the relevant property is located, underscoring the importance of timeliness in the application process. The PR-230 form demands thorough information about the applicant, including their name, the organizational structure of the ownership (ranging from sole proprietorships to non-profit associations), and contact details for key individuals. Additionally, the form explores the property's use in great detail, listing numerous potential purposes from rehabilitation to religious, and it requires applicants to justify the exemption request based on specific statutory references. The comprehensive nature of this document ensures that applicants provide a full picture of the property's use, income derived from it, the benefit it provides to the community, and detailed ownership information—factors all critical to the assessor's evaluation of exemption eligibility under sec. 70.11, Wis. Stats. Furthermore, the requirement for attachments adds another layer of verification to the process, including evidence of non-profit status, organizational documents, and financial information. With all its details, the PR-230 form embodies the state's meticulous approach to property tax exemption, aiming to balance the interest of tax fairness with the provision of public benefits through exempt properties.

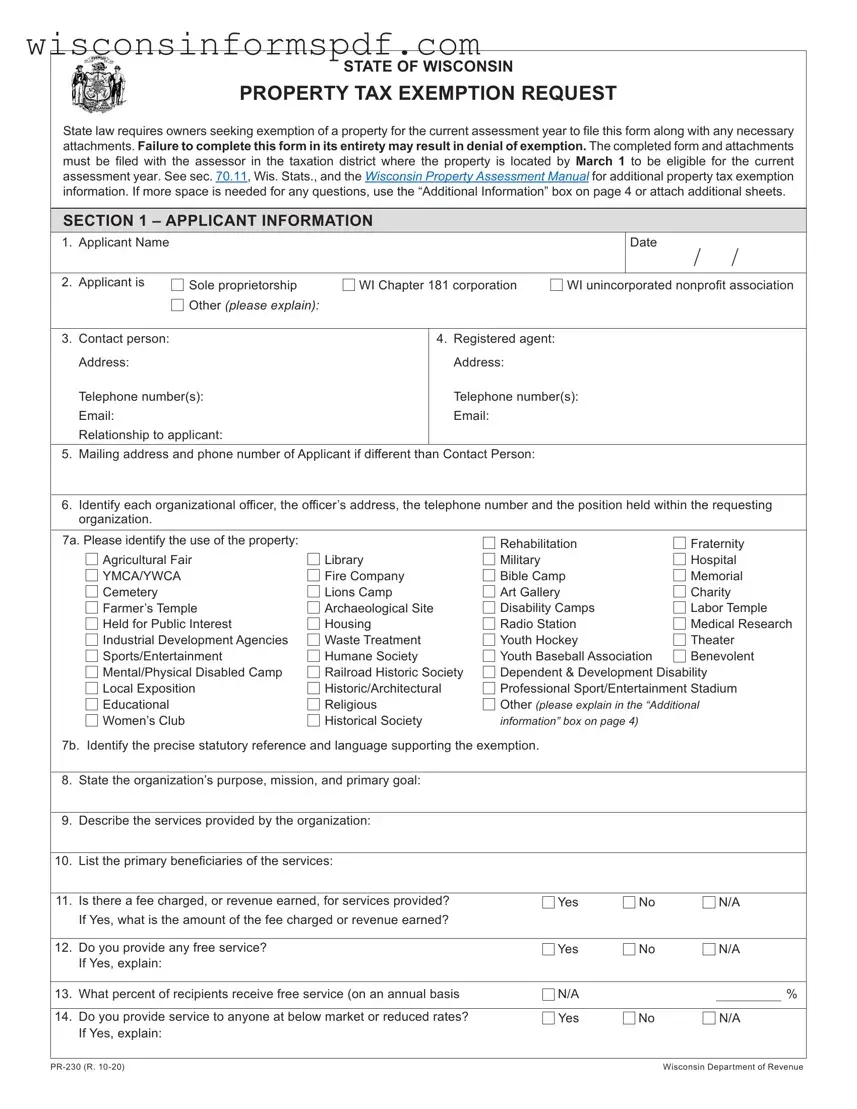

STATE OF WISCONSIN

PROPERTY TAX EXEMPTION REQUEST

State law requires owners seeking exemption of a property for the current assessment year to file this form along with any necessary

attachments. Failure to complete this form in its entirety may result in denial of exemption. The completed form and attachments must be filed with the assessor in the taxation district where the property is located by March 1 to be eligible for the current assessment year. See sec. 70.11, Wis. Stats., and the Wisconsin Property Assessment Manual for additional property tax exemption information. If more space is needed for any questions, use the “Additional Information” box on page 4 or attach additional sheets.

SECTION 1 – APPLICANT INFORMATION

1. Applicant Name

Date

/ /

2. Applicant is |

Sole proprietorship |

WI Chapter 181 corporation |

WI unincorporated nonprofit association |

|

Other (please explain): |

|

|

3.Contact person: Address:

Telephone number(s): Email:

Relationship to applicant:

4.Registered agent: Address:

Telephone number(s): Email:

5.Mailing address and phone number of Applicant if different than Contact Person:

6.Identify each organizational officer, the officer’s address, the telephone number and the position held within the requesting organization.

7a. Please identify the use of the property: |

|

Rehabilitation |

Fraternity |

Agricultural Fair |

Library |

Military |

Hospital |

YMCA/YWCA |

Fire Company |

Bible Camp |

Memorial |

Cemetery |

Lions Camp |

Art Gallery |

Charity |

Farmer’s Temple |

Archaeological Site |

Disability Camps |

Labor Temple |

Held for Public Interest |

Housing |

Radio Station |

Medical Research |

Industrial Development Agencies |

Waste Treatment |

Youth Hockey |

Theater |

Sports/Entertainment |

Humane Society |

Youth Baseball Association |

Benevolent |

Mental/Physical Disabled Camp |

Railroad Historic Society |

Dependent & Development Disability |

|

Local Exposition |

Historic/Architectural |

Professional Sport/Entertainment Stadium |

|

Educational |

Religious |

Other (please explain in the “Additional |

|

Women’s Club |

Historical Society |

information” box on page 4) |

|

7b. Identify the precise statutory reference and language supporting the exemption.

8. |

State the organization’s purpose, mission, and primary goal: |

|

|

|

|

|

|

|

|

9. |

Describe the services provided by the organization: |

|

|

|

|

|

|

|

|

10. |

List the primary beneficiaries of the services: |

|

|

|

|

|

|

|

|

11. |

Is there a fee charged, or revenue earned, for services provided? |

Yes |

No |

N/A |

|

If Yes, what is the amount of the fee charged or revenue earned? |

|

|

|

12.Do you provide any free service? If Yes, explain:

Yes

No

N/A

13. What percent of recipients receive free service (on an annual basis

N/A |

|

% |

14.Do you provide service to anyone at below market or reduced rates? Yes No N/A

If Yes, explain:

Wisconsin Department of Revenue |

15. |

What percentage of annual recipients receive services at below or reduced rates? |

|

N/A |

|

|

|

|

% |

||

|

|

|

|

|

|

|

|

|

|

|

16. |

Are you under any obligation to provide services to those who cannot pay? |

|

|

Yes |

|

No |

N/A |

|||

|

If Yes, explain: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

17. |

Does Applicant receive any subsidies, grants, or low or no interest loans to operate or otherwise |

Yes |

|

No |

N/A |

|||||

|

provide its services? If Yes, identify sources and amounts and how monies are applied or used. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

18. |

How much of Applicant’s annual gross income or revenue is derived from donations? |

$ |

|

|

|

|

|

|

||

|

What percentage is that of Applicant’s total annual income or revenue? |

|

N/A |

|

|

|

|

% |

||

|

|

|

|

|

|

|

|

|

|

|

SECTION 2 – SUBJECT PROPERTY INFORMATION |

* |

|

N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

* If N/A, explain in the “Additional information” box on page 4 of this form. |

|

|

|

|

|

|

|

|

||

19. |

Property for which exemption is being applied (“Subject Property”): |

|

|

|

|

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

Tax parcel number: |

Number of acres: |

|

|

|

|

|

|

|

|

|

Legal description: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20. |

Estimated fair market value of Subject Property: |

|

$ |

|

|

|

|

|

|

|

|

If based on an independent appraisal, identify the appraiser and the purpose of the appraisal below. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

||||

|

Appraiser: |

|

|

as of |

/ |

/ |

|

|

||

|

Purpose of Appraisal: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

21. |

Owner of Subject Property: |

|

|

|

|

|

|

|

|

|

|

If Owner is different from Applicant, explain and identify the relationship between Applicant and Owner. |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

22. |

Date Owner acquired Subject Property: |

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

23. |

Person or entity from whom Owner acquired Subject Property: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24. |

Date Owner first began using and occupying Subject Property: |

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

25. |

Date Applicant first began using and occupying the Subject Property: |

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26. |

Explain precisely how Applicant actually uses the Subject Property: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

27. |

Explain in detail why Applicant feels the Subject Property qualifies for property tax exemption. Finally, describe precisely how |

|||||||||

|

applicant and the Subject Property fit within that statutory language. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION 3 – TENANT INFORMATION |

|

|

N/A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

28. |

Identify all persons and entities other than Owner who have the right to use and occupy any part of the Subject Property. |

|||||||||

|

Include all tenants, licensees, and concessionaires of the Subject Property. Use the space provided on page 4 or attach |

|||||||||

|

additional pages as necessary. For each, include: |

|

|

|

|

|

|

|

|

|

|

a. Name of tenant or occupant. |

|

|

|

|

|

|

|

|

|

|

b. Their mailing address and phone number. |

|

|

|

|

|

|

|

|

|

|

c. Their interest in the Subject Property. |

|

|

|

|

|

|

|

|

|

|

d. A precise and detailed explanation of how they actually use the Subject Property. |

|

|

|

|

|

|

|

|

|

|

e. The date from which they began occupancy of the Subject Property. |

|

|

|

|

|

|

|

|

|

|

f. The monthly rate or fee they pay to use or occupy the Subject Property. |

|

|

|

|

|

|

|

|

|

|

g. An explanation of how rent or other fees they pay to use and occupy the Subject Property are used and applied. |

|

|

|||||||

|

h. The portion of the Subject Property they use or occupy. |

|

|

|

|

|

|

|

|

|

|

Indicate number of users other than owner, if there are no other users, enter “None”. Number of other users: |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

29. |

Identify the percentage of the Subject Property that is used or occupied by persons other than owner. |

|

|

|

|

% |

||||

|

|

|

|

|

|

|

|

|

|

|

30. |

Was the subject Property used in an unrelated trade or business for which the Owner was |

Yes |

|

No |

|

|

||||

|

subject to taxation under section 511 to 515 of the Internal Revenue Code? If Yes, explain: |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

2 |

Wisconsin Department of Revenue |

SECTION 4 – ATTACHMENTS

31.ATTACH COPIES OF THE FOLLOWING DOCUMENTS:

A.Documents regarding applicant, owner, tenant(s), or occupant(s) of the Subject Property (where applicable):

1.Proof of

2.Partnership Agreement, Association Documents, Articles of Incorporation, Charter and

3.Latest annual report filed with State Department of Financial Institutions.

4.Curriculum of educational courses offered.

5.Part II of Form 1023 (Application for Recognition of Exemption) filed with the Internal Revenue Service.

6.Form 990 (Return of Organization Exempt from Income Tax).

7.Form 990T (Exempt Organization Business Income Tax Return).

8.Ordination papers for the occupants if the Subject Property is to be considered eligible as housing for pastors and their ordained assistants, members of religious order and communities, or ordained teachers.

9.Leases and subleases affecting the Subject Property or any part thereof, including all amendments thereto.

10.Concessionaire agreements, license agreements, and other documents regarding the use of occupancy of the Subject Property or any part thereof, including all amendments thereto.

11.Covenants, restrictions, rules and regulations (recorded or unrecorded), and all amendments thereto, affecting use or occupancy of the Subject Property or title thereto and all amendments thereto.

12.Mortgages (recorded or unrecorded) affecting the Subject Property.

13.Copy of the documents listed in 1 through 12 above as the same relate to any tenant or occupant of the property.

14.Any other information that would aid in determining exempt status.

B.Documents regarding the Subject Property:

1.Survey of the Subject Property. This includes certified survey maps and subdivision maps and plats.

2.An Appraisal of the Subject Property.

3.Deeds or instruments of conveyance by which organization acquired interest in the Subject Property.

4.Any other information that would aid in determining exempt status.

SECTION 5 – AFFIDAVIT

Under penalties of perjury, I, on behalf of the

Title

Signature

Telephone |

Date |

( ) –

Name (printed)

STATE OF WISCONSIN

COUNTY OF:

Subscribed and sworn to before me this |

|

day of |

, |

|

||

|

|

|

|

|

|

|

Notary Public |

|

|

|

|

(Seal) |

|

My Commission expires on |

|

|

|

|

|

|

|

|

|

|

|

||

3 |

Wisconsin Department of Revenue |

Note: The following text is an excerpt from Stat., Sec. 70.11. Refer to current Wisconsin Statutes for the complete language or sections applicable to the exemption of property from taxation.

70.11Property exempted from taxation. The property described in this section is exempted from general property taxes if the property is exempt under sub. (1), (2), (18), (21), (27) or (30); if it was exempt for the previous year and its use, occupancy or ownership did not change in a way that makes it taxable; if the property was taxable for the previous year, the use, occupancy or ownership of the property changed in a way that makes it exempt and its owner, on or before March 1, files with the assessor of the taxation district where the property is located a form that the department of revenue prescribes or if the property did not exist in the previous year and its owner, on or before March 1, files with the assessor of the taxation district where the property is located a form that the department of revenue prescribes. Except as provided in subs. (3m)(c), (4)(b), (4a) (f), and (4d), leasing a part of the property described in this section does not render it taxable if the lessor uses all of the leasehold income for maintenance of the leased property, construction debt retirement of the leased property or both and if the lessee would be exempt from taxation under this chapter if it owned the property. Any lessor who claims that leased property is exempt from taxation under this chapter shall, upon request by the tax assessor, provide records relating to the lessor’s use of the income from the leased property.

Additional information:

4 |

Wisconsin Department of Revenue |

| Fact | Details |

|---|---|

| Form Name | Wisconsin Property Tax Exemption Request (PR-230) |

| Purpose | Used by property owners to request exemption from property taxes for the current assessment year. |

| Filing Requirement | Must be filed with the assessor in the taxation district where the property is located by March 1. |

| Applicant Types | Inclusive of sole proprietorships, WI Chapter 181 corporations, WI unincorporated nonprofit associations, among others. |

| Property Uses for Exemption | Covers a wide range of property uses including libraries, hospitals, agricultural fairs, and more. |

| Governing Law | Sec. 70.11, Wisconsin Statutes (Wis. Stats.) |

| Supporting Documents | Includes proof of nonprofit status, financial statements, articles of incorporation, and other related documents. |

| Additional Information | Space available on page 4 of the form or through attachment for expanded responses. |

| Affidavit Section | Includes perjury statement, requiring authorized signature, title, and contact information. |

| Instructions for Use | Clearly stated requirements for filing, including deadlines and necessary documentation. |

After completing the State of Wisconsin Property Tax Exemption Request (PR-230 form), the next step involves submitting the form and any necessary attachments to the local assessor's office by the March 1 deadline. This submission is critical for eligibility consideration for the current assessment year’s property tax exemption. Proper and timely submission of the form, along with all required documents, ensures that the request for exemption is processed without delay. Once submitted, the assessor will review the application to determine if the property meets the criteria for exemption under Wisconsin state law. Remember, thoroughness and accuracy in filling out the form can greatly influence the outcome.

By following these steps carefully, you will complete the State of Wisconsin Property Tax Exemption Request (PR-230 form) accurately, increasing the likelihood of a successful exemption request.

What is the Wisconsin PR-230 form used for?

The Wisconsin PR-230 form is a document utilized by property owners seeking to obtain an exemption from property taxes for the current assessment year in the State of Wisconsin. This request for exemption is required by state law and involves filing the form, along with any necessary attachments, with the assessor of the taxation district where the property is located. Failure to complete this form in its entirety and by the deadline could result in the denial of the property tax exemption. The form serves as an application that substantiates the property's eligibility for exemption based on its ownership, use, occupancy, and other criteria as outlined by the Wisconsin Statutes and the Wisconsin Property Assessment Manual.

Who needs to file the PR-230 form, and what is the deadline?

This form must be filed by property owners seeking tax exemption for a property located within Wisconsin. It is applicable to a range of entities, including sole proprietors, corporations, unincorporated nonprofit associations, and others who believe their property qualifies for exemption under specific sections of Wisconsin Statutes (sec. 70.11, Wis. Stats.). The necessary paperwork, including the completed PR-230 form and any relevant attachments, must be submitted to the local assessor by March 1st to be considered for exemption for the current assessment year. This deadline ensures that the application is reviewed within the appropriate fiscal period for tax assessments.

What documentation is required alongside the PR-230 form?

Applicants must provide a variety of documents alongside the PR-230 form to substantiate their request for a property tax exemption. These include proof of non-profit status, such as a Determination Letter under I.R.C. 501(c)(3), Articles of Incorporation, by-laws, latest annual report filed with the State Department of Financial Institutions, and other relevant organizational documents. Additionally, documents specific to the property in question, such as surveys, appraisals, deeds or instruments of conveyance, and documents related to any tenants or occupants of the property, are required. These documents help in establishing the nonprofit status of the applicant, the ownership and use of the property, and compliance with statutory requirements for a tax exemption.

How does one determine if their property is eligible for exemption?

Eligibility for property tax exemption under the Wisconsin PR-230 form depends on the property's use, ownership, and occupancy aligning with criteria specified in section 70.11 of the Wisconsin Statutes. Properties used for religious, educational, charitable, benevolent, or other specified purposes may qualify for exemption if they meet statutory definitions and requirements. The detailed use and occupancy of the property, the nature of the services provided, and the relationship between the property use and the organization's mission are critical factors in determining eligibility. Owners must clearly articulate how their property's utilization fits within the statutory language granting exemption, providing evidence and detailed explanations as required by the form and supplemental documents. Properly assessing eligibility involves careful consideration of the property's specific use cases against the exemption criteria outlined by state law.

Filling out the Wisconsin PR-230 form, which is a property tax exemption request, requires attention to detail and a thorough understanding of the eligibility criteria as outlined by the State of Wisconsin. Mistakes in completing this form can lead to the denial of the exemption request. Here are six common mistakes:

To ensure a successful exemption application, it is essential to avoid these common pitfalls. Filling out the Wisconsin PR-230 form with accurate and detailed information, along with providing all necessary documentation, significantly increases the likelihood of approval for tax-exempt status. It's not just a formality but a critical step in receiving the benefits to which eligible properties are entitled.

When filing the Wisconsin PR-230 form, which is essential for property tax exemption requests, several other documents are usually required to support the application. These documents vary based on the specific exemptions being claimed and the type of property or organization applying. For clarity, a brief overview of each document typically utilized alongside the Wisconsin PR-230 form is provided below. This information aims to facilitate a smoother application process by ensuring all necessary paperwork is submitted efficiently and accurately.

Compiling and submitting the appropriate documentation is a crucial component of the property tax exemption process. Each of the documents listed plays a specific role in demonstrating eligibility for tax exemption under Wisconsin law. By carefully gathering and reviewing these items, organizations can significantly improve the likelihood of a favorable review by tax assessors, ensuring their valuable resources are focused on serving their mission rather than covering unnecessary tax liabilities.

The Wisconsin PR-230 form, used for property tax exemption requests, has aspects in common with other documents vital for managing and certifying the status of various entities and properties. One similar form is the IRS Form 1023, which organizations use to apply for recognition of exemption under Section 501(c)(3) of the Internal Revenue Code. Both forms require detailed information about the organization's purpose, activities, and financials, aiming to establish eligibility for tax-exempt status.

Equally, the Form 990, an annual return that tax-exempt organizations must file with the IRS, shares a resemblance. This document, like the Wisconsin PR-230, collects detailed financial data, operational information, and governance structure to maintain compliance with tax-exempt regulations. Both serve as transparency tools, providing the necessary oversight agencies and the public with insights into an organization's operations and financial status.

The Uniform Commercial Code (UCC-1) financing statement is another document with similarities. While its primary purpose is to secure interest in a debtor's personal property to ensure payment of a debt, it requires detailed information about the parties involved and the collateral, akin to how the PR-230 form identifies relationships and use of property in tax exemption contexts.

The Certificate of Zoning Compliance, often used in various municipalities across the United States, also parallels the Wisconsin PR-230 form. It confirms a property's compliance with local zoning ordinances, including its allowed uses, much like how the PR-230 form requires detailed explanations of property use to qualify for tax exemption.

Articles of Incorporation, filed by entities to legally establish a corporation, share commonalities with the PR-230 form. Both require comprehensive organization details, such as names and addresses of key individuals, organization purposes, and operational specifics to fulfill statutory requirements for recognition and benefits under the law.

The Grant Deed, a document that transfers ownership of real property, bears a resemblance to the PR-230 in that it must describe the property in detail, including its legal description and parcel number. Similarly, the PR-230 requires precise information about the property seeking tax exemption, ensuring clear identification and eligibility assessment.

The Application for Building Permit is another similar document. It necessitates a thorough description of property use, a legal description, and detailed plans for the intended development or use of the property. This mirrors the requirement on the PR-230 form to detail how the nonprofit organization uses the property in question.

A Certificate of Occupancy, issued by local government agencies to confirm a building's compliance with building codes and its suitability for occupancy, also aligns with the PR-230 form in its function. Both ensure that the use of a property adheres to specific standards and regulations before granting approval for its intended use.

The Environmental Impact Assessment (EIA) report also shares similarities. Though its primary focus is on assessing the environmental effects of proposed projects, it requires a comprehensive analysis of how a project uses land, which parallels the detailed property use information and justification needed for the PR-230 form.

Finally, the Declaration of Covenants, Conditions, and Restrictions (CC&Rs) in real estate developments resemble the PR-230 form. CC&Rs outline the rules and guidelines for properties within a community, including acceptable use of property. The PR-230 form similarly requires detailed descriptions of property use to establish eligibility for tax exemption based on those activities.

When filling out the Wisconsin PR-230 form, a Property Tax Exemption Request, there are several important dos and don'ts to consider for a successful submission. This guide highlights the key aspects to focus on and the pitfalls to avoid to ensure your request is processed efficiently.

Do:

Don't:

By carefully following these guidelines, you can improve the likelihood of a favorable review of your Property Tax Exemption Request in Wisconsin.

Understanding the complexities of property tax exemptions in Wisconsin, particularly through the lens of the PR-230 form, necessitates correcting prevalent misconceptions. Misinterpretations can lead to errors in filing, potentially causing eligible entities to miss out on exemptions. Here, eight commonly misunderstood aspects of the PR-230 form are addressed, fostering a clearer understanding of the process.

Through addressing these misconceptions, entities seeking exemption can more accurately navigate the process, ensuring that eligible properties are granted exemption status accordingly. Each point underscores the importance of meticulous compliance with statutory requirements and the detailed instructions provided by the Wisconsin Department of Revenue.

When seeking a property tax exemption in Wisconsin for the current assessment year, the completion and submission of the PR-230 form is mandated by state law. Owners must ensure that this form, alongside all necessary attachments, is submitted to the assessor of the taxation district where the property is located. The final date for filing to be eligible for exemption in the current assessment year is March 1. This deadline is critical for owners to meet to avoid the potential denial of their exemption request.

The PR-230 form requires comprehensive information regarding the applicant, the property for which the exemption is being sought, and the use of the property. Applicants must provide details about the organization seeking the exemption, including its non-profit status and the services it delivers, the beneficiaries of these services, and any fees charged. Furthermore, precise details about the property’s usage are necessary. If the form does not offer enough space for full answers, additional information can be provided in an "Additional Information" box on page 4 or through attached additional sheets.

Inclusion of supporting documents is vital for the PR-230 form’s acceptance and the subsequent approval of property tax exemption. These documents include proof of non-profit status, organizational documents such as partnership agreements or incorporation articles, financial reports, and any leases or occupancy agreements pertaining to the property. The careful compilation of these documents supports the validity of the exemption request and aids the determination of exempt status.

Affirmation of accuracy and truthfulness through an affidavit section is a required part of the PR-230 form submission process. This section must be completed and signed by an individual authorized by the applying organization, certifying that all information provided on the form and in accompanying documents is true and correct to the best of their knowledge. The affidavit must be sworn and notarized, underscoring the legal responsibility the applicant assumes in declaring the information’s accuracy.

Wisconsin Offer to Purchase Form - The form sets forth requirements for the delivery of documents and notices, ensuring effective communication between parties.

What Is a Rent Certificate - The process for handling rent certificates when a landlord refuses to sign is clearly outlined to assist renters in these situations.

Who Does Well Inspections - An assessment tool used by professionals to evaluate the potability and safety of well water.