Fill Your Wisconsin Wt 7 Tax Form

Fill Your Wisconsin Wt 7 Tax Form

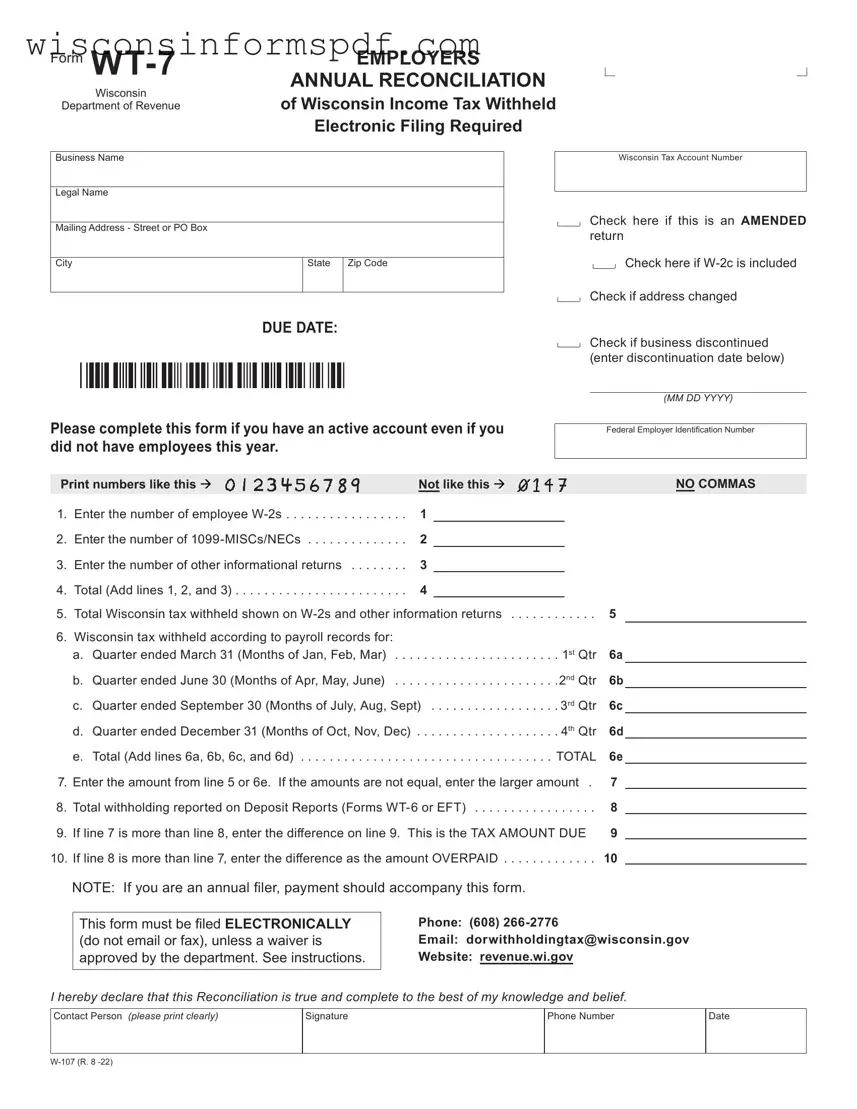

Navigating through the complexities of tax forms can often be challenging for employers, and understanding the specifics of the Wisconsin WT-7, an Employers Annual Reconciliation of Wisconsin Income Tax Withheld, is crucial for any business operating within the state. This form plays a pivotal role in reconciling the amounts withheld from employees' wages throughout the year with the totals reported and submitted to the Wisconsin Department of Revenue. It's designed for businesses to report the number of W-2s, 1099-MISCs/NECs, and other informational returns issued, along with the total Wisconsin tax withheld as shown on these documents. Not only does the form require a detailed breakdown of taxes withheld on a quarterly basis, but it also necessitates a comparison between the reported withholding amounts and those actually deposited through deposit reports or electronic funds transfer. The form carries implications for both annual filers and those who may have discontinued their business operations, offering spaces to indicate address changes, amended returns, and if a business has been discontinued. Importantly, the Wisconsin WT-7 Tax Form must be filed electronically, reinforcing the state's push towards streamlining tax administration and ensuring a more efficient processing framework for both the government and businesses alike. This necessitates that filers are attentive to the accuracy and completeness of the data submitted to avoid discrepancies and potential issues with the tax agency.

Form |

EMPLOYERS |

|

|

ANNUAL RECONCILIATION |

|

|

Wisconsin |

|

|

of Wisconsin Income Tax Withheld |

|

Department of Revenue |

||

Electronic Filing Required

Business Name

Legal Name

Mailing Address - Street or PO Box

City |

State |

Zip Code |

|

|

|

DUE DATE:

Wisconsin Tax Account Number

Check here if this is an AMENDED return

Check here if

Check if address changed

Check if business discontinued (enter discontinuation date below)

Please complete this form if you have an active account even if you did not have employees this year.

(MM DD YYYY)

Federal Employer Identification Number

Print numbers like this |

Not like this |

|

|

|

NO COMMAS |

||

1. |

Enter the number of employee |

1 |

|

|

|

|

|

2. |

Enter the number of |

2 |

|

|

|

|

|

3. |

Enter the number of other informational returns |

3 |

|

|

|

|

|

4. |

Total (Add lines 1, 2, and 3) |

4 |

|

|

|

|

|

5. |

Total Wisconsin tax withheld shown on |

. . . . . . |

5 |

|

|||

6. |

Wisconsin tax withheld according to payroll records for: |

|

|

|

|

|

|

|

a. Quarter ended March 31 (Months of Jan, Feb, Mar) . . . |

. . . . . . . . . . . . . . . . . . . |

. 1st Qtr |

6a |

|

||

|

b. Quarter ended June 30 (Months of Apr, May, June) . . . |

. . . . . . . . . . . . . . . . . . . |

.2nd Qtr |

6b |

|

||

|

c. Quarter ended September 30 (Months of July, Aug, Sept) |

6c |

|

||||

|

d. Quarter ended December 31 (Months of Oct, Nov, Dec) |

. . . . . . . . . . . . . . . . . . . |

. 4th Qtr |

6d |

|

||

|

e. Total (Add lines 6a, 6b, 6c, and 6d) |

. . . . . . . . . . . . . . . . . . . |

TOTAL |

6e |

|||

7. |

Enter the amount from line 5 or 6e. If the amounts are not equal, enter the larger amount . |

7 |

|

||||

8. |

. . . . . . . . . . .Total withholding reported on Deposit Reports (Forms |

. . . . . . |

8 |

|

|||

9. |

If line 7 is more than line 8, enter the difference on line 9. This is the TAX AMOUNT DUE |

9 |

|

||||

. . . . . . .10. If line 8 is more than line 7, enter the difference as the amount OVERPAID |

. . . . . . |

10 |

|

||||

NOTE: If you are an annual filer, payment should accompany this form.

This form must be filed ELECTRONICALLY

(do not email or fax), unless a waiver is approved by the department. See instructions.

Phone: (608)

Email: dorwithholdingtax@wisconsin.gov

Website: revenue.wi.gov

I hereby declare that this Reconciliation is true and complete to the best of my knowledge and belief.

Contact Person (please print clearly)

Signature

Phone Number

Date

| Fact Name | Description |

|---|---|

| Form Identification | Form WT-7 is known as the Employers' Annual Reconciliation of Wisconsin Income Tax Withheld. |

| Filing Requirement | It is mandatory for businesses with an active Wisconsin Tax Account Number to complete this form even if they did not have employees in the given year. |

| Electronic Filing | This form must be filed electronically, unless a waiver has been approved by the Wisconsin Department of Revenue. |

| Amendment Option | Employers have the option to check a box if the submission is an amended return or if W-2c forms are included. |

| Governing Law | The Form WT-7 is governed by Wisconsin state laws regarding the reconciliation and reporting of income tax withheld from employees' wages. |

Filing the Wisconsin Wt 7 Tax form, or the Employers’ Annual Reconciliation of Wisconsin Income Tax Withheld, is a crucial step for employers at the end of the fiscal year. This document plays a significant role in ensuring that the amount of income tax withheld from the employees' salaries throughout the year aligns with the total tax reported and deposited to the state. Whether it's your first time filling out this form or you’re just in need of a quick refresher, the process requires careful attention to detail to ensure accuracy and compliance with Wisconsin's Department of Revenue regulations. Let's walk through the necessary steps to accurately complete the form.

After completing these steps, it's important to remember that this form must be filed electronically with the Wisconsin Department of Revenue, unless you have been granted a specific waiver. The electronic filing requirement streamlines the processing and ensures quicker confirmation of your submission. If there are discrepancies or additional documents required, the Department of Revenue will contact you using the information provided. Successfully submitting the Form WT-7 not only keeps your business in good standing but also plays a part in the overall financial health and compliance with Wisconsin tax law.

What is the Form WT-7 and who needs to file it?

The Form WT-7, also known as the Employers Annual Reconciliation of Wisconsin Income Tax Withheld, is a required form for employers in Wisconsin. It serves to reconcile the amount of state income tax withheld from employees' paychecks throughout the year. Employers who have withheld income tax from employees' wages or have issued W-2s, 1099-MISCs, or 1099-NECs with Wisconsin tax withheld must file this form.

What is the due date for filing Form WT-7?

The due date for filing Form WT-7 is January 31st of the year following the tax year being reported. For example, for the tax year 2021, the form must be submitted by January 31, 2022. It's essential to meet this deadline to avoid any penalties or interest for late filing.

Is electronic filing of Form WT-7 mandatory?

Yes, the Form WT-7 must be filed electronically with the Wisconsin Department of Revenue unless the employer has received a specific waiver that permits them to file by paper. This electronic filing requirement helps streamline the process and ensure accurate and timely submission.

What happens if I need to amend a Form WT-7 already filed?

If you discover an error on a previously filed Form WT-7, you are required to submit an amended return. To do this, check the box on the form indicating that it is an amended return. You'll need to provide updated information and correct any errors from the original submission.

What if I did not have employees this year? Do I still need to file Form WT-7?

Yes, if you have an active account with the Wisconsin Department of Revenue, you are required to file Form WT-7, even if you did not have employees or withhold any income tax during the year. This helps the department maintain accurate records and ensures compliance.

How do I know if I need to include a W-2c with Form WT-7?

If you need to correct any information after W-2 forms have been submitted to the state, a W-2c form must be completed and included with your Form WT-7. This includes any corrections to employees' income, tax withheld, or personal information.

What should I do if my business address or legal name has changed?

If there have been changes to your business address or legal name, you must indicate this on Form WT-7 by checking the appropriate box. This ensures that your business information is updated and that all correspondence from the Wisconsin Department of Revenue is sent to the correct address.

Can I file Form WT-7 if my business has been discontinued?

Yes, if your business has been discontinued, you should still file Form WT-7 for any year in which you had an active withholding account. It is crucial to include the discontinuation date on the form, which notifies the Wisconsin Department of Revenue that no future filings will be necessary under that account.

Filling out the Wisconsin WT-7 Tax Form, the Employers' Annual Reconciliation of Wisconsin Income Tax Withheld, requires careful attention to detail. Unfortunately, mistakes can happen, which may lead to delays in processing or even penalties. Here are nine common errors that people often make:

It's easy for individuals and businesses to make these mistakes, particularly when dealing with the complexities of tax forms. Paying close attention to every detail on the form, double-checking all entries against payroll records, and ensuring to comply with the requirement for electronic filing can help avoid these common errors. Keeping accurate records throughout the year can also simplify the reconciliation process when it's time to file the WT-7 form.

Remember, inaccuracies and omissions on the Wisconsin WT-7 Tax Form can lead to unnecessary delays or financial penalties. Taking the time to review your form thoroughly before submission is crucial. When in doubt, consulting with a tax professional or reaching out to the Wisconsin Department of Revenue can provide additional clarity and help ensure that your reconciliation is complete and accurate.

When dealing with the Wisconsin WT-7 Tax Form, an Employer's Annual Reconciliation of Income Tax Withheld, one must often handle additional forms and documents to ensure comprehensive compliance and accurate reporting. These forms serve various purposes, from reporting specific types of income to amending previously submitted information. Understanding each document's role is crucial for businesses aiming to fulfill their tax obligations effectively.

Effectively managing these documents is fundamental to ensuring accuracy in tax reporting and compliance. Each form has a specific purpose and deadlines that must be adhered to. Proper understanding and timely submission of these forms, along with the Wisconsin WT-7, help employers maintain good standing with tax authorities and avoid potential penalties. Keeping abreast of the requirements for each of these documents can significantly streamline the tax reporting process.

The Form 940, also known as the Employer's Annual Federal Unemployment (FUTA) Tax Return, shares similarities with Wisconsin's WT-7 form in its primary function of reconciling taxes related to employment over the past year. Both forms require employers to report the total amount of taxes withheld or due based on employee wages. However, while the WT-7 focuses on state income tax withheld in Wisconsin, Form 940 focuses on federal unemployment tax, demonstrating the parallel structure in tax reporting duties at different government levels.

Form W-3, the Transmittal of Wage and Tax Statements, serves a similar role to the WT-7 by summarizing the information reported on individual W-2 forms for federal tax purposes. It consolidates the total earnings, Social Security wages, Medicare wages, and withholding for all employees of a business. This parallels the WT-7's role in reconciling the total state income tax withheld, as reported on W-2s, with the employer's payroll records for the state of Wisconsin. Both ensure accurate reporting and reconciliation of employee-related taxes.

The Form 941, Employer's Quarterly Federal Tax Return, is akin to the WT-7 in its objective to report taxes withheld from employees' paychecks; however, it does so on a quarterly basis instead of annually. It includes federal income tax, Social Security, and Medicare taxes that employers must withhold. This contrasts with WT-7's annual reconciliation but stresses the continuous requirement for employers to report and reconcile taxes withheld for government records.

The 1096 form, Annual Summary and Transmittal of U.S. Information Returns, is used to transmit paper copies of all 1099 forms sent to the IRS. Like the WT-7, it functions as a summary document that aids in the reconciliation process, in this case, for various forms of non-employee compensation. While 1096 encompasses a broader range of transactions beyond employee wage withholding, the essence of facilitating year-end reporting to the revenue authorities aligns it with the purposes of the WT-7 form.

The Form W-2, Wage and Tax Statement, directly relates to the WT-7 in the ecosystem of tax reporting documents. While individual W-2 forms report wages paid and taxes withheld for each employee, the WT-7 aggregates this information to reconcile total income taxes withheld as stated by employers in Wisconsin. The relationship between W-2 forms and the WT-7 is integral, as the accuracy of WT-7 submissions depends on the comprehensive reporting of each W-2.

State-specific counterparts to the WT-7 form, such as California's Form DE-9, the Annual Reconciliation Statement, serve a directly comparable role in other jurisdictions. These forms, while tailored to the unique tax codes and requirements of their respective states, share the WT-7's fundamental objective of reconciling the total amount of state income tax withheld from employees with the records maintained by employers. This similarity underlines a universal need within U.S. tax systems for annual employer reconciliations at the state level.

The Schedule H (Form 1040), Household Employment Taxes, while focused on domestic employment, shares an underlying principle with the WT-7 form by requiring the reconciliation of taxes (Social Security, Medicare, FUTA, and federal income tax) related to employment. Specifically, it applies to household employers who may not operate a formal business but are subject to tax withholding duties similar to those of business employers. The commonality lies in ensuring that employment taxes are properly accounted for and reported, regardless of the employment context.

When preparing and filing the Wisconsin WT-7 Tax Form, it's essential to proceed with care and attention to detail to ensure accuracy and compliance with state requirements. Below are key dos and don'ts that can guide you through the process:

By adhering to these guidelines, employers can fulfill their reporting obligations efficiently and minimize the risk of errors. It's always recommended to consult the complete instructions provided by the Wisconsin Department of Revenue or seek professional advice if there are uncertainties or complex issues.

Understanding the Wisconsin WT-7 Tax Form often leads to some common misconceptions. To clarify, below are some of the most frequent misunderstandings and their accurate explanations.

Electronic Filing Is Optional: Many believe filing this form electronically is a choice. However, the form clearly states that electronic filing is a requirement unless a waiver has been approved by the department. This mandate aims to streamline processing and ensure accuracy.

Only Employers with Current Employees Must File: A significant misconception is that the WT-7 is only for businesses with active employees within the year. Even if a business had no employees during the year, if it has an active Wisconsin Tax Account Number, it needs to complete this form.

Address Changes Are Automatically Updated: Some employers think that updating their address with the Wisconsin Department of Revenue for other forms automatically updates their information for the WT-7 form. However, employers must indicate an address change directly on the form to ensure accurate records.

Amendments Are Difficult to File: The process for amending a WT-7 form is often viewed as cumbersome. However, the form includes a specific checkbox to indicate an amendment, simplifying the process to correct previously submitted information.

W-2c Forms Are Unnecessary with WT-7 Filings: Another misunderstanding is the belief that corrected W-2 forms (W-2cs) are not to be included with the WT-7. Yet, the form specifically asks if W-2c is included, highlighting the importance of submitting these corrections as part of the reconciliation process.

All Payments Must Be Made with the WT-7 Form: While annual filers are required to make their payment with the submission of the WT-7, this misconception overlooks the detail that payments corresponding to the withholding reported can also be made through Deposit Reports (Forms WT-6 or EFT) before the annual reconciliation.

Decimal Points and Commas Are Required for Figures: The correct way to report figures on the WT-7 form is without using commas or decimal points. This common error can lead to confusion and processing delays. The form provides clear examples of the proper formatting.

Business Discontinuation Is Not Relevant: Contrary to this belief, the form includes a section specifically for indicating if a business has discontinued. This information is crucial for the Department of Revenue to maintain accurate and current records.

Form WT-6 and WT-7 Are Interchangeable: It's a common mistake to confuse the purpose of Forms WT-6 and WT-7. Form WT-6 is for quarterly or monthly deposit reporting, whereas WT-7 is an annual reconciliation. Each serves a distinct role in tax reporting and compliance.

Filing Without Payment When Amounts Differ: If the Total Wisconsin tax withheld shown on W-2s and other information returns differs from the amount according to payroll records, some believe it's acceptable to file the WT-7 without resolving the discrepancy. In reality, the form requires entering the larger amount and, if necessary, calculating either the tax amount due or the amount overpaid, clarifying the need to address and report differences accurately.

Understanding these nuances of the Wisconsin WT-7 Tax Form is crucial for employers to ensure compliance and avoid common pitfalls in tax reporting and reconciliation.

Filling out and using the Wisconsin WT-7 Tax Form, known as the Employers Annual Reconciliation of Wisconsin Income Tax Withheld, involves several key points that employers need to be aware of to ensure compliance and accuracy in their tax filings. Here are the takeaways that will help simplify this process:

By taking these points into consideration, employers can navigate their responsibilities more confidently, ensuring that they meet their obligations to the Wisconsin Department of Revenue while minimizing errors in their tax filings.

Buying a Home in Wisconsin - Explains the implications of a financing contingency and the buyer's obligations within such a clause.

Wisconsin Mv2449 - The Wisconsin MV2449 form is an application for a 72-Hour Charter School Bus Trip Permit by the Wisconsin Department of Transportation, allowing temporary intrastate travel.